Question: i need help writing reccommendations and investment plan for the family's finances. Case Study - Betty and Robert Burger You and Betty had attended the

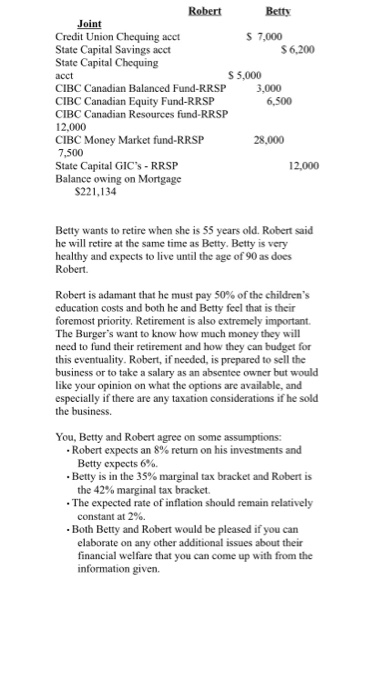

Case Study - Betty and Robert Burger You and Betty had attended the same high school many years ago and knew each other casually. You ran into her at a benefit dinner last week and she introduced you to her husband Robert, whom she married three years ago. She was impressed to find that you were now a financial planner with the firm of Princeton Financial Planners Inc. She had mentioned that she and Robert would like someone to look at their financial affairs and you offered to complete a comprehensive financial plan. She informed you that she is also having financial plans completed by competing firms so it is important that you provide a plan that is sufficient to win you their business. You met with Betty and Robert a few days later (week three of this course) to obtain the particulars about the state of their finances and told them you would provide a detailed financial plan within the next 8 weeks. Robert Burger is a 47 year old entrepreneur and the sole owner of Complete Brand Consulting Corporation", an extremely successful small Canadian qualified corporation He has operated the business successfully for the past 15 years and has a salary of $93,000 per annum (each year). He feels the business is worth $450,000 if it was sold today and has estimated that the net worth of the business will grow by an average of 6% a year. He would like any ideas you have regarding tax planning and the benefits he could receive if he sold the business at retirement. Robert has two children from his previous marriage: William who is 5 years old and Cathy who is 7. They live with their mother Marie, Robert's estranged first wife. Robert pays Marie $550 a month in alimony payments and a monthly total of $1,200 in child support payments. He will cover 50% of the children's 4 years of college/university education which currently costs $8,000 a year, and these costs are estimated to grow at 5% per year. Both children will be starting university college at age 18 (13 and 11 years respectively from now). He would like to know more about ways to fund these costs. He was also told by a friend that child support payments are no longer tax deductible and has asked you to review this for him and give him the correct answer. Betty is 35 and works at State Capital Bank as a Marketing Manager. She earns $70,000 a year and is a member of her company's defined benefit pension plan. She has been with the bank for five years and is quite comfortable in her position and feels it is quite secure. Betty and Robert want to start a family over the next couple of years and feel they will need to save S 6,000 a year for The Burger's purchased their home in in April 2012 for $325,000 and at that time obtained a fixed-rate mortgage of $240,000 at 6.75% (5 year term, monthly pay, 25 year amortization, renewal date: April 10, 2017). They pay $1,648 a month in principal and interest payments and when the mortgage renews at that time the principal owing will be at $220,000. The principal owing on their last statement was $221.134. They have talked to one bank and have been given the following choices for the renewal of their mortgage Monthly Term Type Amortization Rate Paymen year Fixed/closed 20 years 3.5% $1,285 year Fixed/closed 20 years 3.9% $1,330 year $1,37 Fixed/closed 4.25% 20 years Variable/open prime - $1,203 20 years 5 year 50%* The variable mortgage rate fluctuates with the bank prime rate so that it is always 50% (half a percent) less than the prime rate. The bank prime rate is currently 3.25%. All the above allow 20% of the original balance to be paid on each anniversary date (once a year). Note: For this paper use the rates listed, do not shop for other rates. A real estate salesperson has told them that their house is now worth $440,000 and should grow in value with the expected rate of inflation of 3%. Forty percent the home's value is considered due to the worth of the land and 60% is the replacement cost of the building structure. Robert and Betty want your opinion on which mortgage is best for them, why you suggest this is the best mortgage for them, and how this would affect their budget. Betty and Robert have unused RRSP contribution room of $30,000 and $70,000 respectively. Robert will continue to make the $20,000 contribution (as a lump sum in February) each year and Betty will continue her monthly contributions at the same rate as this year. Betty gets some great benefits from working at State Capital Bank such as no transaction fees on her bank accounts, lots of benefits (80% dental coverage, family plan included), life insurance equal to one times her salary, and disability insurance to 70% of her take home salary. Robert does not have any health benefits, life or disability Betty is a member of a non-contributory defined benetit pension plan that will pay her a pension at age 65 of 1.5% of the average of her last 5 years of salary, times the number of years she works with the bank. Betty plans on retiring at age 55. If she takes her retirement benefits earlier than age 65 she losses 5% per year. She expects her salary to keep pace with inflation estimated to be 2%. Betty contributes $5,400 each year to her self-directed RRSP and will continue to do so until she retires. She would be happy with a yearly return of 6%. Robert is a risk taker and feels long-term he would like to see a return of 8% on his investments. The Burger family lives well at the moment. Their current expenses are: Robert Betty Joint Clothing $ 2,000/year $2.400/year Fitness Club S 120 month Hair cuts/ grooming $ 30/month s 90/month Dining Out & lunches S 150/week S 30/week Property taxes 2,200/year Property Insurance 480/year Utilities 325/month Telephone 80/month Cable TV 110/month Groceries 500/month Cleaning service 90/month Home repairs 900/year Vacations 7,000/year Robert has a new Chrysler 300 (less than a year old) car purchased by his company for $55,000 and us e costs $800 Robert has a new Chrysler 300 (less than a year old) car purchased by his company for $55,000 and used mostly for business. The lease costs $800 a month, insurance is another $1,400 a year and gas cost $90 a week. It has a full bumper-to-bumper warranty so there are no repair charges. He feels its resale value is around $42.000 today. He has $200,000 in liability insurance, full collision and comprehensive insurance coverage. Betty has a low mileage 2000 Honda Civic that is in great condition and runs well. It is painted orange so has a low resale value of S1,100 but it is paid in full. She uses the car sparingly and spends S50 a month on gas. It costs $180 a year for repairs, S48 a year for licensing and another $500 a year for insurance (she has $1,000,000 liability, full collision and comprehensive with a deductible of $500). She really does not want to sell the car but has asked you if she should Betty has $350 outstanding on her VISA while Robert has $1,750 outstanding on his VISA (Robert's VISA is a company card). The monthly minimum payment on each card if not paid in full each month is 5% per of the outstanding balance. The Burger's tax returns for last year contained the following: Robert Betty Employment S 93,000 $70,000 CPP Premium 2,356 2,356 El Premiums 892 RRSP Contributions 20.000* 5.400 Charitable Donations SOO 400 Alimony 6,600 Taxes 26,480 19.250 *Note; He made his RRSP contribution as a lump sum payment in February of this year. The following most recent statements (from the previous month) were also provided. Robert Betty Joint Credit Union Chequing acet $ 7,000 State Capital Savings acct S 6,200 State Capital Chequing acet S5,000 CIBC Canadian Balanced Fund-RRSP 3,000 CIBC Canadian Equity Fund-RRSP 6,500 CIBC Canadian Resources fund-RRSP 12,000 CIBC Money Market fund-RRSP 28,000 7,500 State Capital GIC'S - RRSP 12,000 Balance owing on Mortgage Robert Betty Joint Credit Union Chequing acct $ 7,000 State Capital Savings acct $6.200 State Capital Chequing acct S 5,000 CIBC Canadian Balanced Fund-RRSP 3,000 CIBC Canadian Equity Fund-RRSP 6,500 CIBC Canadian Resources fund-RRSP 12.000 CIBC Money Market fund-RRSP 28.000 7,500 State Capital GIC'S - RRSP 12.000 Balance owing on Mortgage S221.134 Betty wants to retire when she is 55 years old. Robert said he will retire at the same time as Betty. Betty is very healthy and expects to live until the age of 90 as does Robert Robert is adamant that he must pay 50% of the children's education costs and both he and Betty feel that is their foremost priority. Retirement is also extremely important. The Burger's want to know how much money they will need to fund their retirement and how they can budget for this eventuality. Robert, if needed, is prepared to sell the business or to take a salary as an absentee owner but would like your opinion on what the options are available, and especially if there are any taxation considerations if he sold the business. You, Betty and Robert agree on some assumptions: . Robert expects an 8% return on his investments and Betty expects 6%. .Betty is in the 35% marginal tax bracket and Robert is the 42% marginal tax bracket. The expected rate of inflation should remain relatively constant at 2%. . Both Betty and Robert would be pleased if you can elaborate on any other additional issues about their financial welfare that you can come up with from the information given. Case Study - Betty and Robert Burger You and Betty had attended the same high school many years ago and knew each other casually. You ran into her at a benefit dinner last week and she introduced you to her husband Robert, whom she married three years ago. She was impressed to find that you were now a financial planner with the firm of Princeton Financial Planners Inc. She had mentioned that she and Robert would like someone to look at their financial affairs and you offered to complete a comprehensive financial plan. She informed you that she is also having financial plans completed by competing firms so it is important that you provide a plan that is sufficient to win you their business. You met with Betty and Robert a few days later (week three of this course) to obtain the particulars about the state of their finances and told them you would provide a detailed financial plan within the next 8 weeks. Robert Burger is a 47 year old entrepreneur and the sole owner of Complete Brand Consulting Corporation", an extremely successful small Canadian qualified corporation He has operated the business successfully for the past 15 years and has a salary of $93,000 per annum (each year). He feels the business is worth $450,000 if it was sold today and has estimated that the net worth of the business will grow by an average of 6% a year. He would like any ideas you have regarding tax planning and the benefits he could receive if he sold the business at retirement. Robert has two children from his previous marriage: William who is 5 years old and Cathy who is 7. They live with their mother Marie, Robert's estranged first wife. Robert pays Marie $550 a month in alimony payments and a monthly total of $1,200 in child support payments. He will cover 50% of the children's 4 years of college/university education which currently costs $8,000 a year, and these costs are estimated to grow at 5% per year. Both children will be starting university college at age 18 (13 and 11 years respectively from now). He would like to know more about ways to fund these costs. He was also told by a friend that child support payments are no longer tax deductible and has asked you to review this for him and give him the correct answer. Betty is 35 and works at State Capital Bank as a Marketing Manager. She earns $70,000 a year and is a member of her company's defined benefit pension plan. She has been with the bank for five years and is quite comfortable in her position and feels it is quite secure. Betty and Robert want to start a family over the next couple of years and feel they will need to save S 6,000 a year for The Burger's purchased their home in in April 2012 for $325,000 and at that time obtained a fixed-rate mortgage of $240,000 at 6.75% (5 year term, monthly pay, 25 year amortization, renewal date: April 10, 2017). They pay $1,648 a month in principal and interest payments and when the mortgage renews at that time the principal owing will be at $220,000. The principal owing on their last statement was $221.134. They have talked to one bank and have been given the following choices for the renewal of their mortgage Monthly Term Type Amortization Rate Paymen year Fixed/closed 20 years 3.5% $1,285 year Fixed/closed 20 years 3.9% $1,330 year $1,37 Fixed/closed 4.25% 20 years Variable/open prime - $1,203 20 years 5 year 50%* The variable mortgage rate fluctuates with the bank prime rate so that it is always 50% (half a percent) less than the prime rate. The bank prime rate is currently 3.25%. All the above allow 20% of the original balance to be paid on each anniversary date (once a year). Note: For this paper use the rates listed, do not shop for other rates. A real estate salesperson has told them that their house is now worth $440,000 and should grow in value with the expected rate of inflation of 3%. Forty percent the home's value is considered due to the worth of the land and 60% is the replacement cost of the building structure. Robert and Betty want your opinion on which mortgage is best for them, why you suggest this is the best mortgage for them, and how this would affect their budget. Betty and Robert have unused RRSP contribution room of $30,000 and $70,000 respectively. Robert will continue to make the $20,000 contribution (as a lump sum in February) each year and Betty will continue her monthly contributions at the same rate as this year. Betty gets some great benefits from working at State Capital Bank such as no transaction fees on her bank accounts, lots of benefits (80% dental coverage, family plan included), life insurance equal to one times her salary, and disability insurance to 70% of her take home salary. Robert does not have any health benefits, life or disability Betty is a member of a non-contributory defined benetit pension plan that will pay her a pension at age 65 of 1.5% of the average of her last 5 years of salary, times the number of years she works with the bank. Betty plans on retiring at age 55. If she takes her retirement benefits earlier than age 65 she losses 5% per year. She expects her salary to keep pace with inflation estimated to be 2%. Betty contributes $5,400 each year to her self-directed RRSP and will continue to do so until she retires. She would be happy with a yearly return of 6%. Robert is a risk taker and feels long-term he would like to see a return of 8% on his investments. The Burger family lives well at the moment. Their current expenses are: Robert Betty Joint Clothing $ 2,000/year $2.400/year Fitness Club S 120 month Hair cuts/ grooming $ 30/month s 90/month Dining Out & lunches S 150/week S 30/week Property taxes 2,200/year Property Insurance 480/year Utilities 325/month Telephone 80/month Cable TV 110/month Groceries 500/month Cleaning service 90/month Home repairs 900/year Vacations 7,000/year Robert has a new Chrysler 300 (less than a year old) car purchased by his company for $55,000 and us e costs $800 Robert has a new Chrysler 300 (less than a year old) car purchased by his company for $55,000 and used mostly for business. The lease costs $800 a month, insurance is another $1,400 a year and gas cost $90 a week. It has a full bumper-to-bumper warranty so there are no repair charges. He feels its resale value is around $42.000 today. He has $200,000 in liability insurance, full collision and comprehensive insurance coverage. Betty has a low mileage 2000 Honda Civic that is in great condition and runs well. It is painted orange so has a low resale value of S1,100 but it is paid in full. She uses the car sparingly and spends S50 a month on gas. It costs $180 a year for repairs, S48 a year for licensing and another $500 a year for insurance (she has $1,000,000 liability, full collision and comprehensive with a deductible of $500). She really does not want to sell the car but has asked you if she should Betty has $350 outstanding on her VISA while Robert has $1,750 outstanding on his VISA (Robert's VISA is a company card). The monthly minimum payment on each card if not paid in full each month is 5% per of the outstanding balance. The Burger's tax returns for last year contained the following: Robert Betty Employment S 93,000 $70,000 CPP Premium 2,356 2,356 El Premiums 892 RRSP Contributions 20.000* 5.400 Charitable Donations SOO 400 Alimony 6,600 Taxes 26,480 19.250 *Note; He made his RRSP contribution as a lump sum payment in February of this year. The following most recent statements (from the previous month) were also provided. Robert Betty Joint Credit Union Chequing acet $ 7,000 State Capital Savings acct S 6,200 State Capital Chequing acet S5,000 CIBC Canadian Balanced Fund-RRSP 3,000 CIBC Canadian Equity Fund-RRSP 6,500 CIBC Canadian Resources fund-RRSP 12,000 CIBC Money Market fund-RRSP 28,000 7,500 State Capital GIC'S - RRSP 12,000 Balance owing on Mortgage Robert Betty Joint Credit Union Chequing acct $ 7,000 State Capital Savings acct $6.200 State Capital Chequing acct S 5,000 CIBC Canadian Balanced Fund-RRSP 3,000 CIBC Canadian Equity Fund-RRSP 6,500 CIBC Canadian Resources fund-RRSP 12.000 CIBC Money Market fund-RRSP 28.000 7,500 State Capital GIC'S - RRSP 12.000 Balance owing on Mortgage S221.134 Betty wants to retire when she is 55 years old. Robert said he will retire at the same time as Betty. Betty is very healthy and expects to live until the age of 90 as does Robert Robert is adamant that he must pay 50% of the children's education costs and both he and Betty feel that is their foremost priority. Retirement is also extremely important. The Burger's want to know how much money they will need to fund their retirement and how they can budget for this eventuality. Robert, if needed, is prepared to sell the business or to take a salary as an absentee owner but would like your opinion on what the options are available, and especially if there are any taxation considerations if he sold the business. You, Betty and Robert agree on some assumptions: . Robert expects an 8% return on his investments and Betty expects 6%. .Betty is in the 35% marginal tax bracket and Robert is the 42% marginal tax bracket. The expected rate of inflation should remain relatively constant at 2%. . Both Betty and Robert would be pleased if you can elaborate on any other additional issues about their financial welfare that you can come up with from the information given

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts