Question: i need the formulas for the blanks please Consider the following information. Your portfolio is invested 30 percent each in A and C, and 40

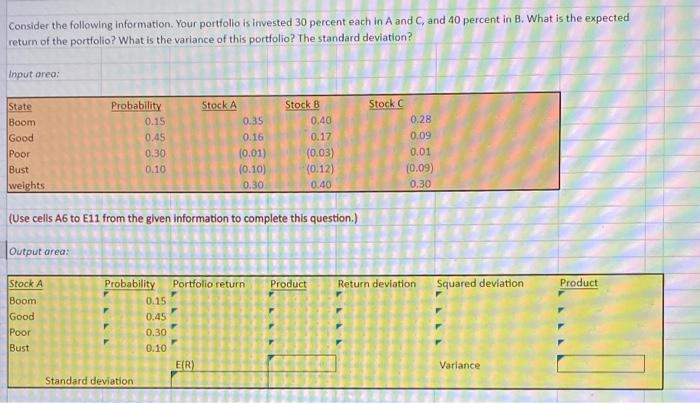

Consider the following information. Your portfolio is invested 30 percent each in A and C, and 40 percent in B. What is the expected return of the portfolio? What is the variance of this portfolio? The standard deviation? Input oreo: State Boom Good Poor Bust weights Probability 0.15 0,45 0.30 0.10 Stock A 0.35 0.16 (0.01) (0.10 0.30 Stock B 0.40 0.17 (0.03) (0.12) 0.40 Stock 0.28 0.09 0.01 (0.09) 0.30 (Use cells A6 to E11 from the given information to complete this question) Output area: Portfolio return Product Return deviation Squared deviation Product Stock A Boom Good Poor Bust Probability 0.15 0.45 0.30 0.10 . ER Variance Standard deviation

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts