Question: I need the portfolio variance for part B. Plus the formula to know what cell to reference. If you know the equation to solve the

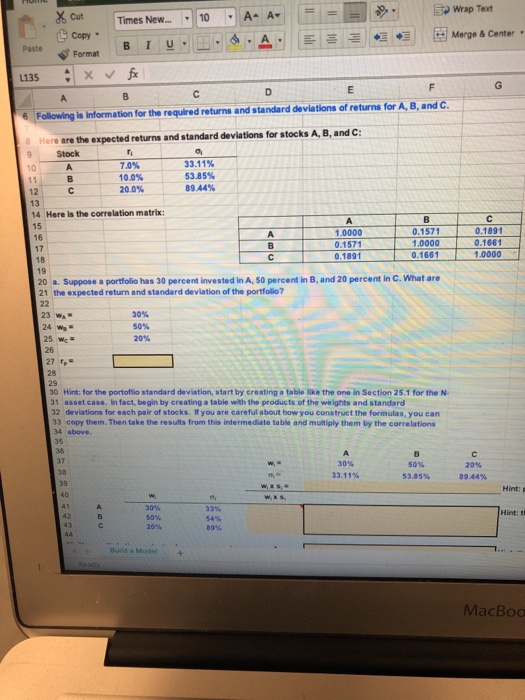

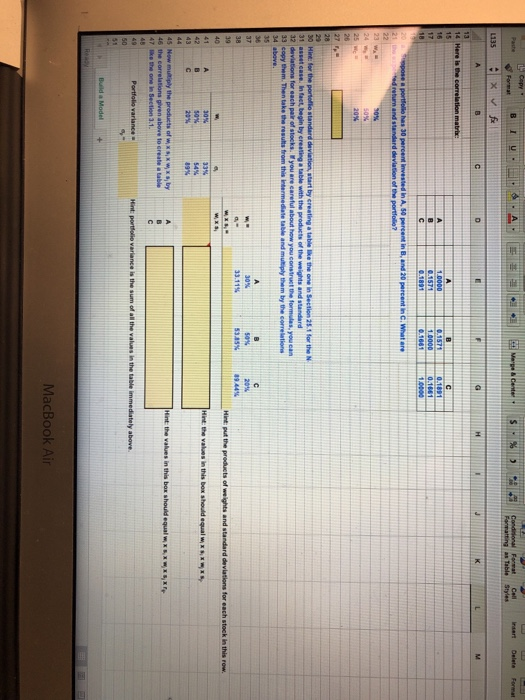

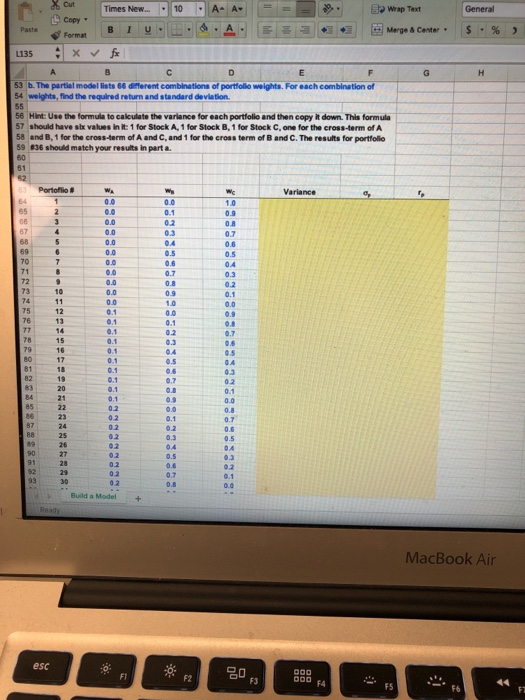

Wrap Text cut Times New." 10A AFE Copy Following is Information for the required returns and standard deviations of returns for A, B, and C Here are the expected returns and standard deviations for stocks A, B, and C: 9 Stock 10 10.0% 20.0% 33.11% 53.85% 89.44% 12 14 Here is the correlation matrix: 15 1.0000 0.1571 0.1891 1570.1891 0.15710 4661 1.0000 16 17 18 19 20 a. Suppose a portfolio has 30 percent invested in A, 50 percent in B, and 20 percent in C. What are 21 the expected return and standard deviation of the portfolio? 0.1661 1.0000 30% 50% 20% 23 WA 25 we 27 f, 30 Hint: for the portoflio standard deviation, start by creating a table like the one in Section 25.1 for the N 31 asset case. In fact, begin by creating a table with the products of the weights and standard 32 deviations for each pair of stocks. f you are careful about how you construet the formulas, you can 33 copy them. Then take the results from this intermediate table and multiply them by the correlations 34 above. 37 30% 33.11% 50% 53.85% 20% 39.44% 33% 54% Hint: t Buid a Model+ MacBod 135 of the weights and standard 20% 53.85% Times New.10 A A- Copy Format 135 3 bThe partial model lists 66 different combinations of portfollo weights. For each combination of 54 weights, find the required return and standard deviation 56 Hint: Use the formula to cakculate the variance for each portfolio and then copy it down. This formula 57 should have six values in it 1 for Stock A, 1 for Stock B, 1 for Stock C, one for the cross-term of A 58 and B, 1 for the cross-term of A and C, and 1 for the croas term of B and C. The results for portfolio #36 should match your results in part a. 61 Portofio # Variance 1.0 0.0 0.1 0.3 0.7 0.6 69 70 0.0 0.0 72 73 0.2 0.1 0.0 0.9 o.8 0.7 10 09 1.0 75 0.1 0.1 13 0.1 78 15 16 17 0.1 0.1 0.1 0.1 0.1 0.1 04 0.5 0.7 0.8 0.9 02 0.1 23 0.1 0.2 0.3 04 0.7 0.6 0.4 0.2 02 0.2 02 0.4 0.7 0.1 Build a Model+ MacBook Air esc F1 O0D FA F6 F5 Wrap Text cut Times New." 10A AFE Copy Following is Information for the required returns and standard deviations of returns for A, B, and C Here are the expected returns and standard deviations for stocks A, B, and C: 9 Stock 10 10.0% 20.0% 33.11% 53.85% 89.44% 12 14 Here is the correlation matrix: 15 1.0000 0.1571 0.1891 1570.1891 0.15710 4661 1.0000 16 17 18 19 20 a. Suppose a portfolio has 30 percent invested in A, 50 percent in B, and 20 percent in C. What are 21 the expected return and standard deviation of the portfolio? 0.1661 1.0000 30% 50% 20% 23 WA 25 we 27 f, 30 Hint: for the portoflio standard deviation, start by creating a table like the one in Section 25.1 for the N 31 asset case. In fact, begin by creating a table with the products of the weights and standard 32 deviations for each pair of stocks. f you are careful about how you construet the formulas, you can 33 copy them. Then take the results from this intermediate table and multiply them by the correlations 34 above. 37 30% 33.11% 50% 53.85% 20% 39.44% 33% 54% Hint: t Buid a Model+ MacBod 135 of the weights and standard 20% 53.85% Times New.10 A A- Copy Format 135 3 bThe partial model lists 66 different combinations of portfollo weights. For each combination of 54 weights, find the required return and standard deviation 56 Hint: Use the formula to cakculate the variance for each portfolio and then copy it down. This formula 57 should have six values in it 1 for Stock A, 1 for Stock B, 1 for Stock C, one for the cross-term of A 58 and B, 1 for the cross-term of A and C, and 1 for the croas term of B and C. The results for portfolio #36 should match your results in part a. 61 Portofio # Variance 1.0 0.0 0.1 0.3 0.7 0.6 69 70 0.0 0.0 72 73 0.2 0.1 0.0 0.9 o.8 0.7 10 09 1.0 75 0.1 0.1 13 0.1 78 15 16 17 0.1 0.1 0.1 0.1 0.1 0.1 04 0.5 0.7 0.8 0.9 02 0.1 23 0.1 0.2 0.3 04 0.7 0.6 0.4 0.2 02 0.2 02 0.4 0.7 0.1 Build a Model+ MacBook Air esc F1 O0D FA F6 F5

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts