Question: I only need answer for question 4, plesse/thanks. I only need answer for this question, #4. Question 1 1 pts Questions 1-8 are based on

I only need answer for question 4, plesse/thanks.

I only need answer for this question, #4.

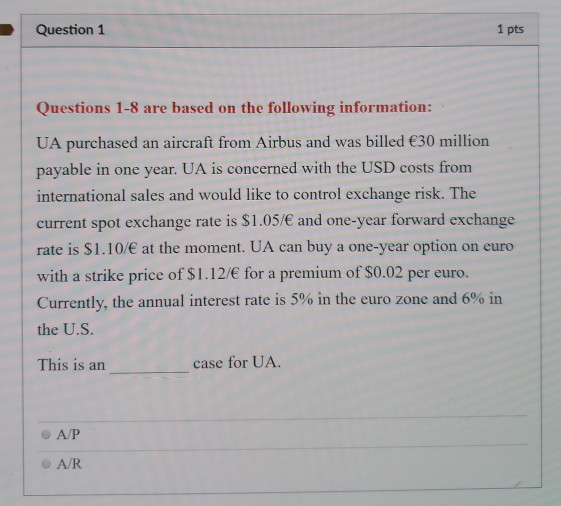

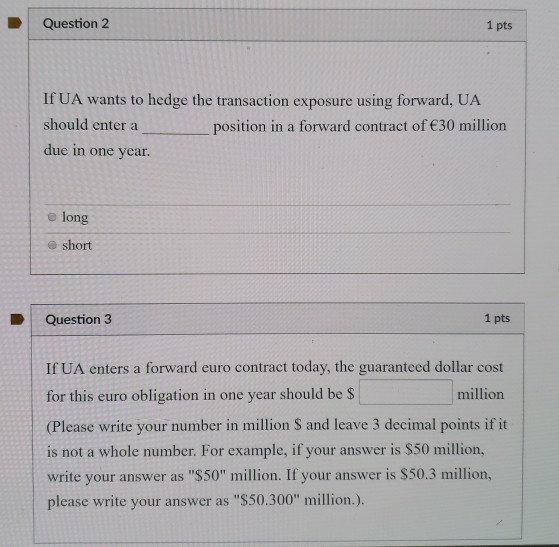

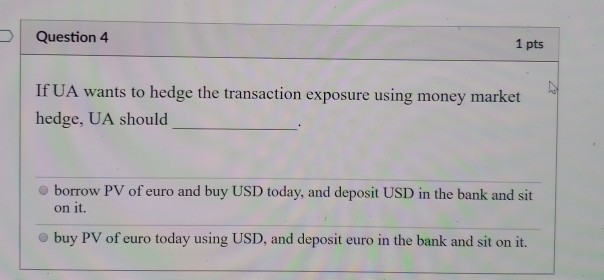

Question 1 1 pts Questions 1-8 are based on the followving information: UA purchased an aircraft from Airbus and was billed 30 million payable in one year. UA is concerned with the USD costs from international sales and would like to control exchange risk. The current spot exchange rate is $1.05/ and one-year forward exchange rate is $1.10/ at the moment. UA can buy a one-year option on euro with a strike price of S1.12/ for a premium of $0.02 per euro. Currently, the annual interest rate is 5% in the euro zone and 6% in the U.S. This is an case for UA e A/P o A/R Question 2 1 pts If UA wants to hedge the transaction exposure using forward, UA should enter a position in a forward contract of 30 million due in one year. e long e short Question 3 1 pts If UA enters a forward euro contract today, the guaranteed dollar cost for this euro obligation in one year should be $ (Please write your number in million S and leave 3 decimal points if it million is not a whole number. For example, if your answer is $50 million, write your answer as "$50" million. If your answer is $50.3 million, please write your answer as "$50.300" million.). Question 4 1 pts If UA wants to hedge the transaction exposure using money market hedge, UA should o borrow PV of euro and buy USD today, and deposit USD in the bank and sit on it. o buy PV of euro today using USD, and deposit euro in the bank and sit on it

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts