Question: I only need the solution to part b. If you need more information I will add it. The following exercises use the random stock price

I only need the solution to part b. If you need more information I will add it.

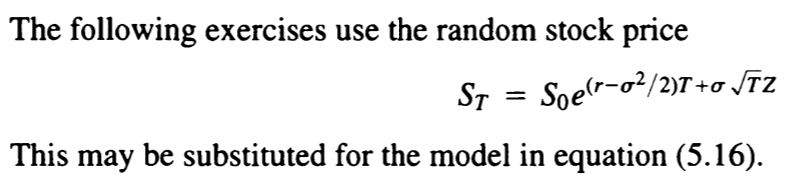

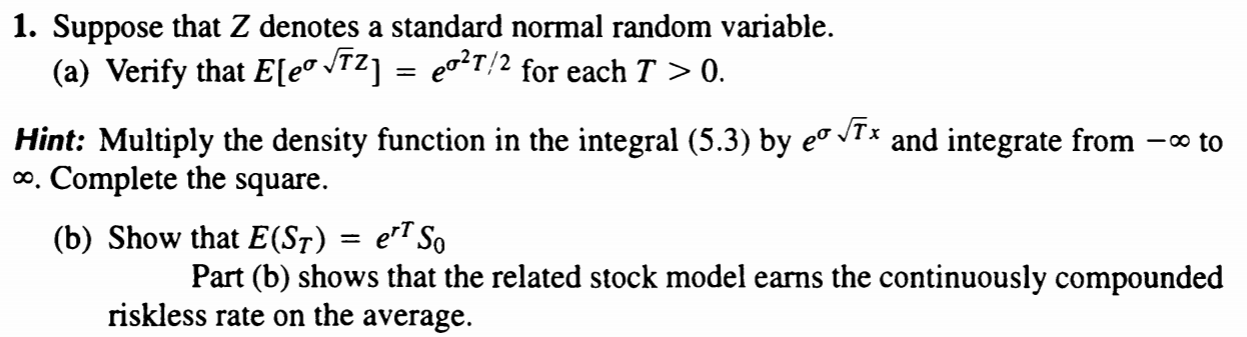

The following exercises use the random stock price Sy = Soerr-92/2)T +0 VIZ This may be substituted for the model in equation (5.16). -o to 1. Suppose that Z denotes a standard normal random variable. (a) Verify that E[e0 VT2] = {0-1/2 for each T >0. Hint: Multiply the density function in the integral (5.3) by eo vix and integrate from 00. Complete the square. (b) Show that E(ST) = et So Part (b) shows that the related stock model earns the continuously compounded riskless rate on the average. The following exercises use the random stock price Sy = Soerr-92/2)T +0 VIZ This may be substituted for the model in equation (5.16). -o to 1. Suppose that Z denotes a standard normal random variable. (a) Verify that E[e0 VT2] = {0-1/2 for each T >0. Hint: Multiply the density function in the integral (5.3) by eo vix and integrate from 00. Complete the square. (b) Show that E(ST) = et So Part (b) shows that the related stock model earns the continuously compounded riskless rate on the average

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts