Question: I posted this question earlier but only a & b were answered. I still need help with c through e. 1. A pension fund manager

I posted this question earlier but only a & b were answered. I still need help with c through e.

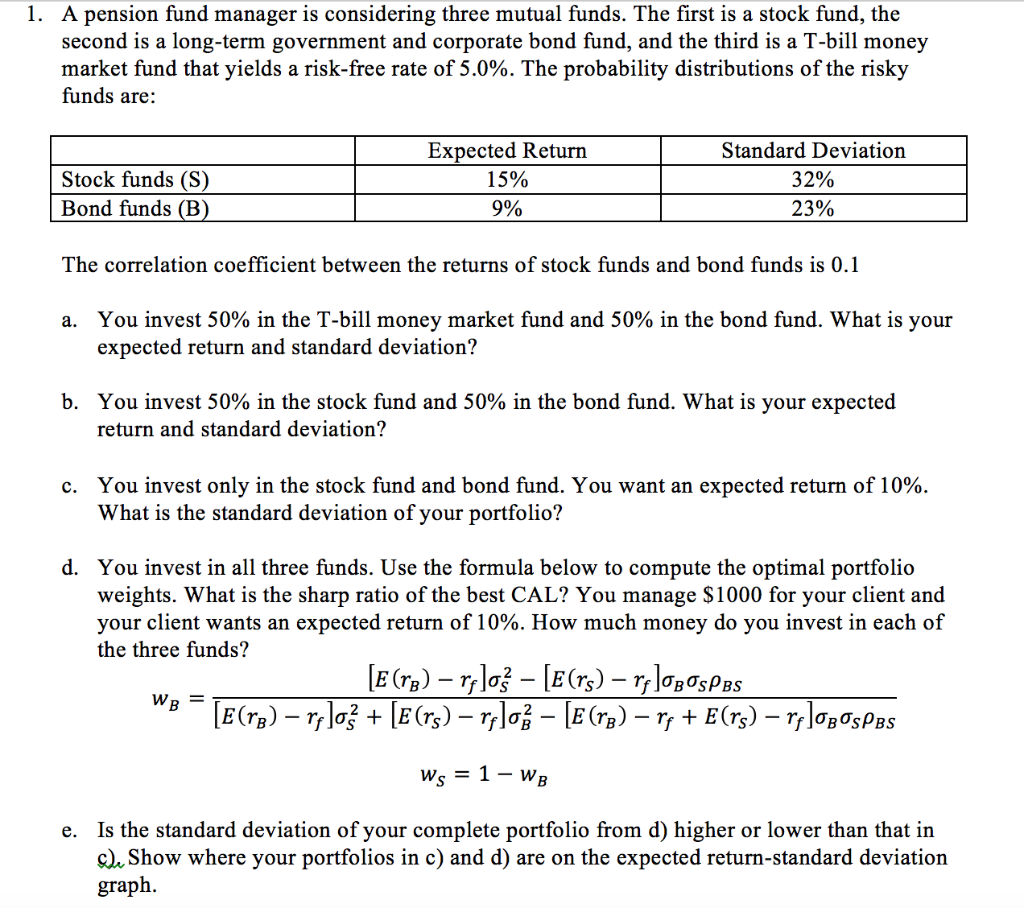

1. A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a risk-free rate of 5.0%. The probability distributions of the risky funds are: Expected Return 15% 9% Standard Deviation 32% 23% Stock funds (S) Bond funds (B The correlation coefficient between the returns of stock funds and bond funds is 0.1 a. You invest 50% in the T-bill money market fund and 50% in the bond fund. What is your expected return and standard deviation'? b. You invest 50% in the stock fund and 50% in the bond fund. What is your expected return and standard deviation? You invest only in the stock fund and bond fund. You want an expected return of 10%. What is the standard deviation of your portfolio! c. d. You invest in all three funds. Use the formula below to compute the optimal portfolio weights. What is the sharp ratio of the best CAL? You manage $1000 for your client and your client wants an expected return of 10%. How much money do you invest in each of the three funds? Is the standard deviation of your complete portfolio from d) higher or lower than that in ), Show where your portfolios in c) and d) are on the expected return-standard deviatiorn graph. e

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts