Question: I was able to get parts a and b. Cannot figure out part c. Please advise (This is all the information given in the problem,

I was able to get parts a and b. Cannot figure out part c. Please advise (This is all the information given in the problem, the last chegg helper said there wasnt enough info, but there is)

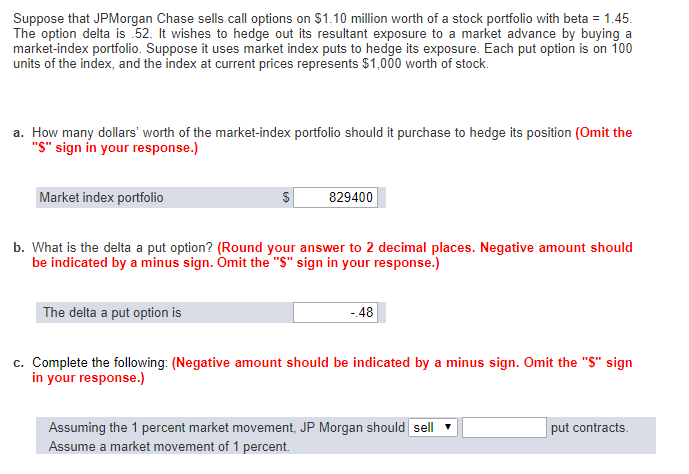

Suppose that JPMorgan Chase sells call options on $1.10 million worth of a stock portfolio with beta = 1.45. The option delta is .52. It wishes to hedge out its resultant exposure to a market advance by buying a market-index portfolio. Suppose it uses market index puts to hedge its exposure. Each put option is on 100 units of the index, and the index at current prices represents $1,000 worth of stock. a. How many dollars' worth of the market-index portfolio should it purchase to hedge its position (Omit the "S" sign in your response.) Market index portfolio 829400 b. What is the delta a put option (Round your answer to 2 decimal places. Negative amount should be indicated by a minus sign. Omit the "S" sign in your response.) The delta a put option is -48 c. Complete the following: (Negative amount should be indicated by a minus sign. Omit the "$" sign in your response.) Assuming the 1 percent market movement. JP Morgan should sell Assume a market movement of 1 percent

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts