Question: I would like to know how to write the correct process for the two small questions in this question. Thank you! Exercise 4. Let (0,)

I would like to know how to write the correct process for the two small questions in this question. Thank you!

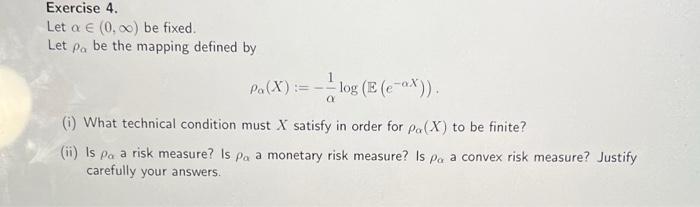

Exercise 4. Let (0,) be fixed. Let a be the mapping defined by (X):=1log(E(eX)) (i) What technical condition must X satisfy in order for (X) to be finite? (ii) Is a risk measure? Is a monetary risk measure? Is a convex risk measure? Justify carefully your answers

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock