Question: If the bond face value is not given, assume that it is $100. Find the swap rate of a 1.5-year plain vanilla swap 3 months

- If the bond face value is not given, assume that it is $100.

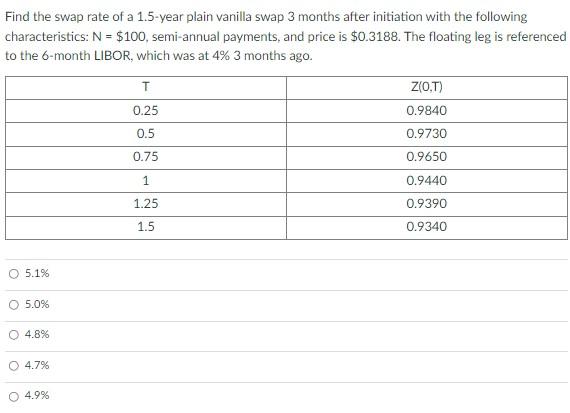

Find the swap rate of a 1.5-year plain vanilla swap 3 months after initiation with the following characteristics: N = $100, semi-annual payments, and price is $0.3188. The floating leg is referenced to the 6-month LIBOR, which was at 4% 3 months ago. T Z(O,T) 0.25 0.9840 0.5 0.9730 0.75 0.9650 1 0.9440 1.25 0.9390 1.5 0.9340 O 5.1% O 5.0% 4.8% 4.7% 4.9% Find the swap rate of a 1.5-year plain vanilla swap 3 months after initiation with the following characteristics: N = $100, semi-annual payments, and price is $0.3188. The floating leg is referenced to the 6-month LIBOR, which was at 4% 3 months ago. T Z(O,T) 0.25 0.9840 0.5 0.9730 0.75 0.9650 1 0.9440 1.25 0.9390 1.5 0.9340 O 5.1% O 5.0% 4.8% 4.7% 4.9%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts