Question: ignore the current answered(0.5%) please provide a simple answer Question (Interest rate swap, 1 of 4) Company A wants to finance a $100,000,000 project at

ignore the current answered(0.5%) please provide a simple answer

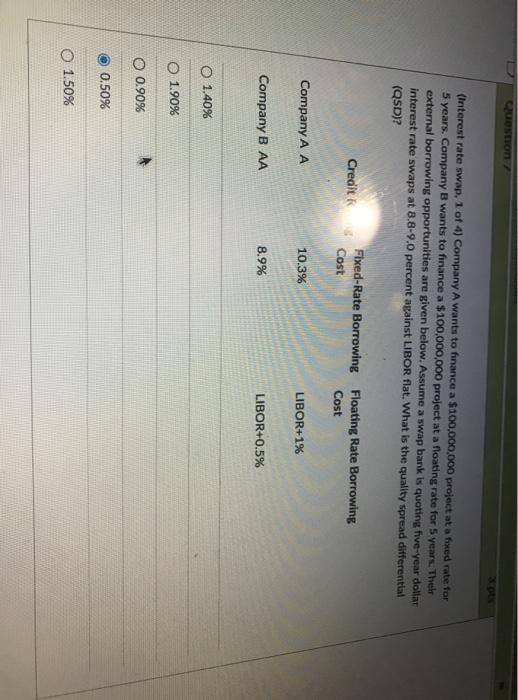

Question (Interest rate swap, 1 of 4) Company A wants to finance a $100,000,000 project at a fixed rate for 5 years. Company B wants to finance a $100,000,000 project at a floating rate for 5 years. Their external borrowing opportunities are given below. Assume a swap bank is quoting five-year dollar interest rate swaps at 8.8-9.0 percent against LIBOR flat. What is the quality spread differential (QSD)? Credit Fixed-Rate Borrowing Floating Rate Borrowing Cost Cost Company A A 10.3% LIBOR+19 Company B AA 8.9% LIBOR+0.5% O 1.40% O 1.90% O 0.90% 0.50% O 1.50%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock