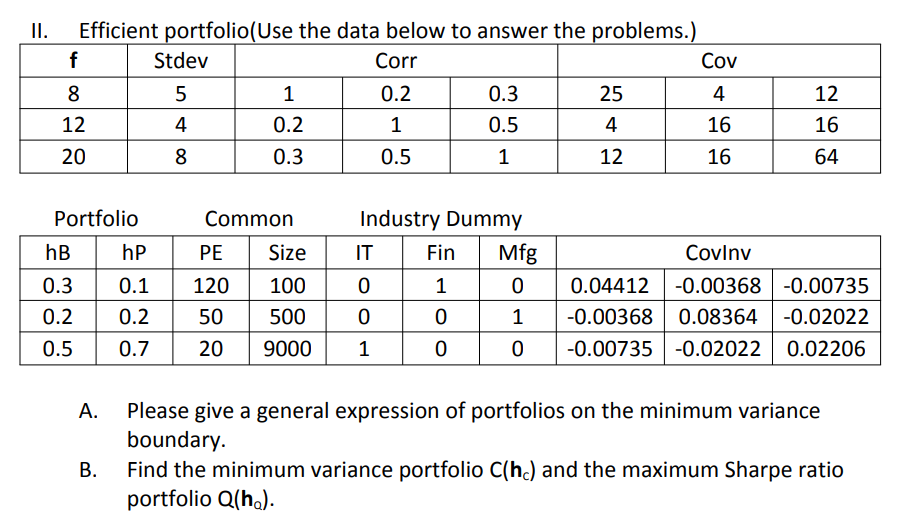

Question: II. Efficient portfolio(Use the data below to answer the problems.) Stdev Corr Cov 8 5 1 0.2 0.3 25 4 12 12 4 0.2 1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock