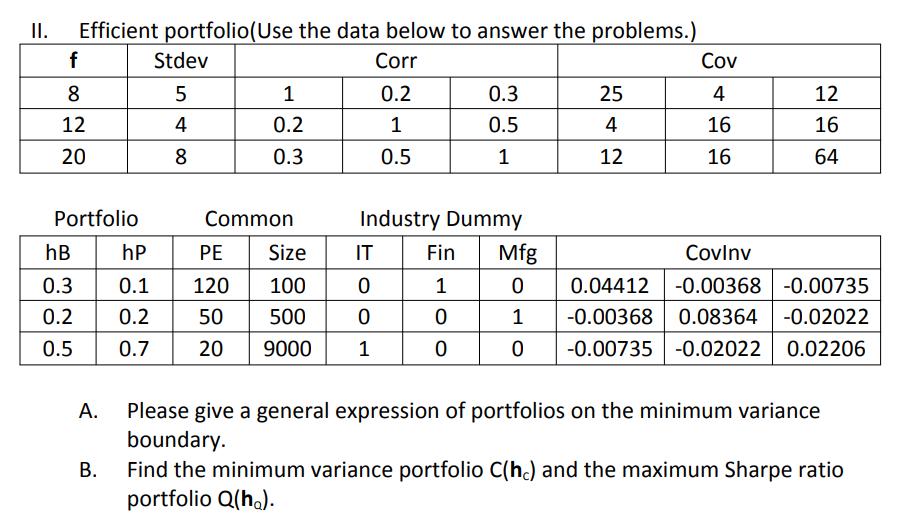

Question: II. Efficient portfolio(Use the data below to answer the problems.) Corr f 8 12 20 Portfolio hB 0.3 0.2 0.5 A. B. Stdev 5

II. Efficient portfolio(Use the data below to answer the problems.) Corr f 8 12 20 Portfolio hB 0.3 0.2 0.5 A. B. Stdev 5 4 8 1 0.2 0.3 Common hP 0.1 120 0.2 50 0.7 20 0.2 1 0.5 0.3 0.5 1 Fin 1 0 0 25 4 12 Industry Dummy PE Size IT Mfg Covlnv 100 0 0 0.04412 -0.00368 -0.00735 0.08364 -0.02022 500 0 1 -0.00368 9000 1 0 -0.00735 -0.02022 -0.02022 0.02206 Cov 4 16 16 12 16 64 Please give a general expression of portfolios on the minimum variance boundary. Find the minimum variance portfolio C(hc) and the maximum Sharpe ratio portfolio Q(ho).

Step by Step Solution

★★★★★

3.53 Rating (146 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock