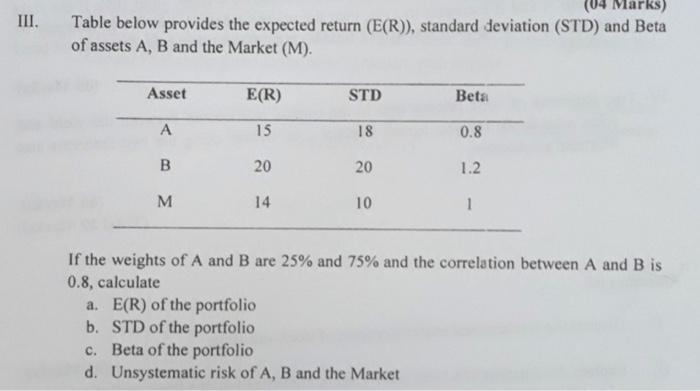

Question: III. (04 Marks) Table below provides the expected return (E(R)), standard deviation (STD) and Beta of assets A, B and the Market (M). Asset E(R)

III. (04 Marks) Table below provides the expected return (E(R)), standard deviation (STD) and Beta of assets A, B and the Market (M). Asset E(R) STD Beta 15 18 0.8 B 20 20 1.2 M 14 10 1 If the weights of A and B are 25% and 75% and the correlation between A and B is 0.8, calculate a. E(R) of the portfolio b. STD of the portfolio c. Beta of the portfolio d. Unsystematic risk of A, B and the Market

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock