Question: (iii) Write down the payment matrix, Q, and corresponding price vector, pS, derived from the following elemental payment combinations: B0: Buy a Bond at period

(iii) Write down the payment matrix, Q, and corresponding price vector, pS, derived from the following elemental payment combinations:

B0: Buy a Bond at period 0, sell it at the end of the next period;

S0: Buy a Stock at period 0, sell it at the end of the next period;

Bb: At period 1, if the state is b, buy a Bond, sell it at the end of the next period;

Sb: At period 1, if the state is b, buy a Stock, sell it at the end of the next period.

B02: Buy a Bond at period 0, sell it at the end of period 2;

S02: Buy a Stock at period 0, sell it at the end of period 2;

can you please give me an specific solution to show how to work out this ?

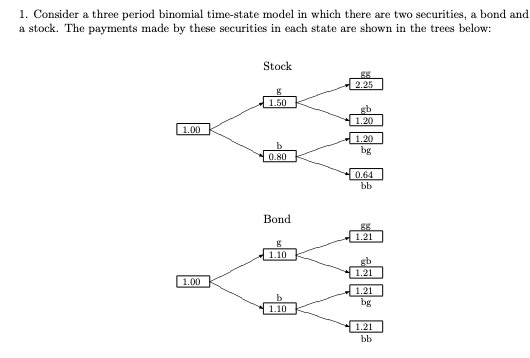

1. Consider a three period binomial time-state model in which there are two securities, a bond and a stock. The payments made by these securities in each state are shown in the trees below: Stock 55 2.25 8 1.50 gb 1.20 1.00 b 0.80 1.20 bg 0.64 bb Bond 55 1.21 8 1.10 gb 1.21 1.00 b 1.10 1.21 bg 1.21 bb

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts