Question: I'm getting a little lost here with ways to work with the risk free bond. I would need some guidance on how to work with

I'm getting a little lost here with ways to work with the risk free bond. I would need some guidance on how to work with this question.

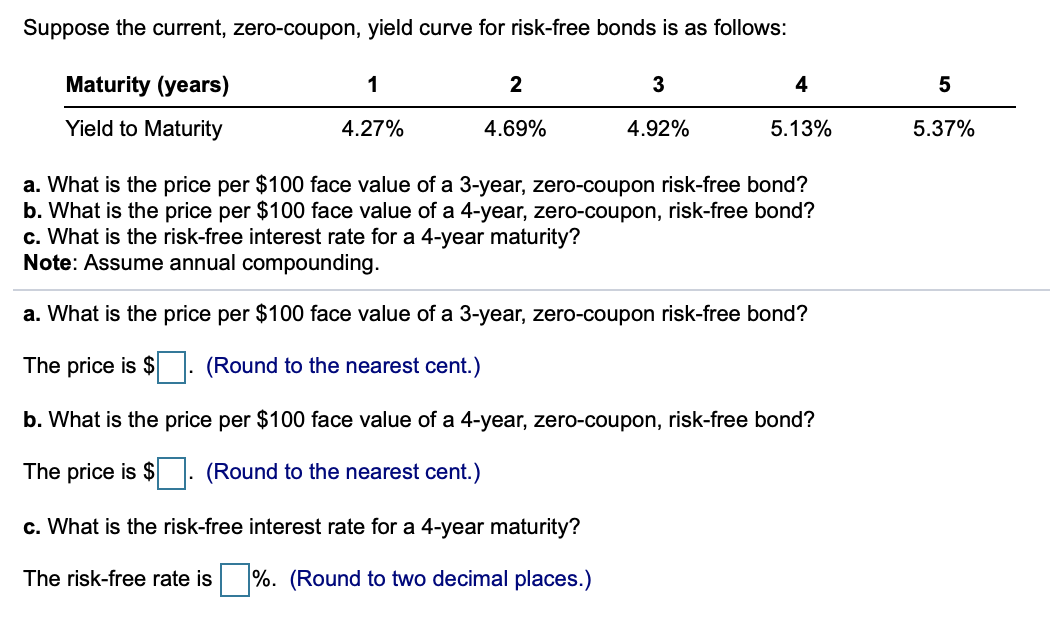

Suppose the current, zero-coupon, yield curve for risk-free bonds is as follows: Maturity (years) 2 3 4 5 Yield to Maturity 4.27% 4.69% 4.92% 5.13% 5.37% a. What is the price per $100 face value of a 3-year, zero-coupon risk-free bond? b. What is the price per $100 face value of a 4-year, zero-coupon, risk-free bond? c. What is the risk-free interest rate for a 4-year maturity? Note: Assume annual compounding. a. What is the price per $100 face value of a 3-year, zero-coupon risk-free bond? The price is $ (Round to the nearest cent.) b. What is the price per $100 face value of a 4-year, zero-coupon, risk-free bond? The price is $ . (Round to the nearest cent.) c. What is the risk-free interest rate for a 4-year maturity? The risk-free rate is %. (Round to two decimal places.)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts