In early 1986, Roy Tyson purchased Professional Building Maintenance, Inc. (PBM), a building maintenance and cleaning...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

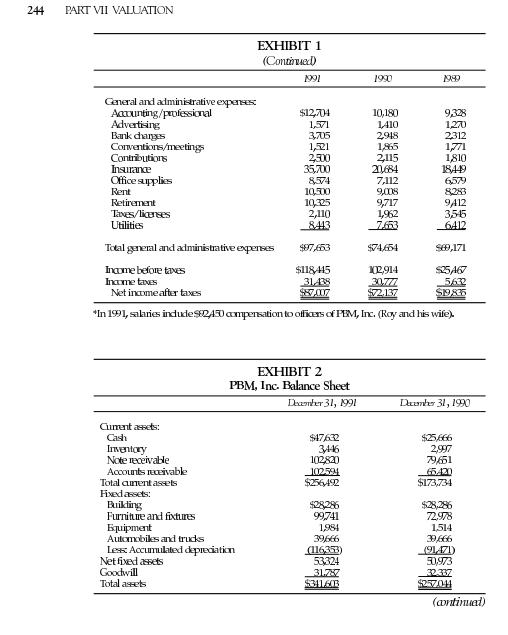

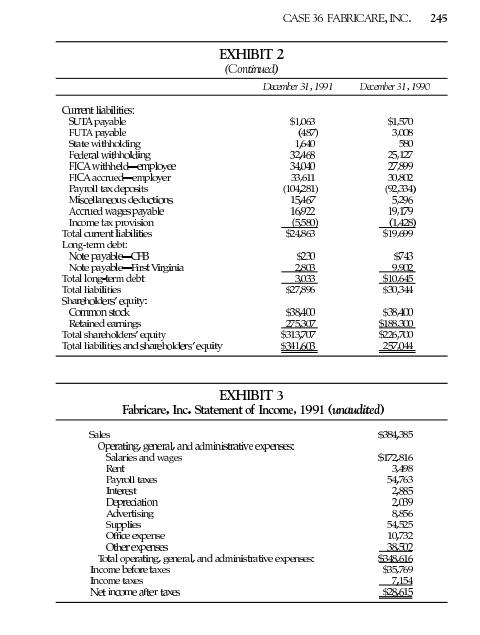

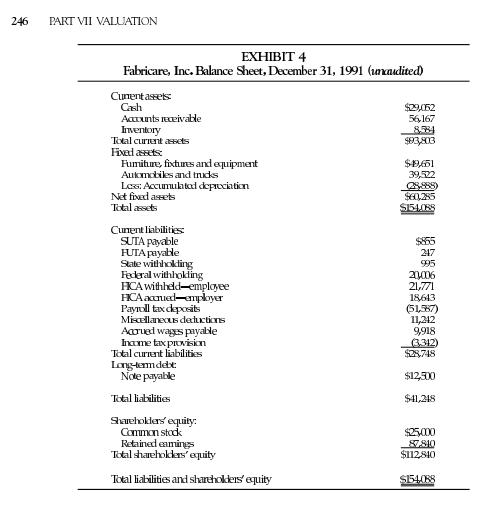

In early 1986, Roy Tyson purchased Professional Building Maintenance, Inc. (PBM), a building maintenance and cleaning firm located and operating in the Danville, Virginia area. The firm specialized in providing cleaning services in commercial and professional offices, such as banks, law offices, and medical practices. Over the next 5 years, revenues increased more than 400 percent, from $212,100 to $851,430 in 1991 (see Exhibit 1 and 2). The revenue growth rate slowed in 1991 as PBM's market share (currently 40 percent) in the area expanded and the potential new prospect pool declined. Roy was confident that the expertise he had gained while operating PBM could be applied successfully to similar firms in other geographical markets that possessed greater growth potential than Danville. In 1992, he learned that a building maintenance firm, Fabricare, Inc., located in Lynchburg, Virginia, was for sale. Fabricare's most recent (year- end 1991) revenues were less than one-half of those of PBM, but Roy believed the growth potential to be much greater because Fabricare had only a small share (approximately 10 percent) of the Lynchburg market. As he looked over the 1991 income statement and balance sheet for Fabricare, Roy was try- ing to decide (1) if he should purchase the company and (2) if so, at what price. Fabricare, like PBM, was in the building maintenance business, but approxi- mately one-half of its revenues came from commercial establishment carpet cleaning. The owner of Fabricare was approaching retirement age and no prepa- ration had been made for management succession in the small firm. On investigation, Roy learned that Fabricare had about $384,000 in revenues in 1991, a figure that had grown only modestly over the previous three years (Exhibit 3 is a 1991 income statement, derived from Fabricare's 1991 tax return. Exhibit 4 is an unaudited 1991 balance sheet for Fabricare). Fabricare's current owners were not much on keeping careful records. Past income records were not reliable in Roy's judgment. Hence, the decision regarding acquisition of Fabricare had to be based primarily on Roy's own projections of cash flows from Fabricare and on an appraisal of the quality of the assets that would be acquired. In assessing Fabricare's market position, Roy visited the competitors' prem- ises noting, in particular, the number of service vehicles that each business had available. Although a relatively crude method of measuring the business activ- ity level of each firm and relative market shares, he had found this to be a fairly accurate indicator in the Danville area. From these observations, Roy believed that Fabricare had only a 10 percent share of the building maintenance business in Lynchburg, In addition, Roy learned from some of the local firms that made use of building maintenance services in Lynchburg that the bidding techniques and performance standards were similar to those he had experienced from his competitors in Danville. Lynchburg had a larger business and professional community than Danville and offered greater immediate growth potential than existed in the saturated Danville market. Upon a closer examination of Fabricare, Roy saw a firm whose business could be expanded from its current customer base into a more success- ful, full-service building maintenance firm like PBM. Roy felt strongly that he could capture about the same market share (40 percent) in Lynchburg as he had in Danville. Beyond that level, Roy found additional market share difficult to obtain from customers who often were more concerned about cost considera- tions than quality of performance. Roy also considered a startup operation, but he concluded that the pur- chase of an existing firm would give him quicker access to the market. In addition to the current customer base, he would also obtain employees who were familiar with the business and the area. Based on an estimate of the cur- rent and future total market for building maintenance services in Lynchburg and a projection of Fabricare's market penetration that matched the historical performance of PBM, Roy estimated that sales revenues under his manage- ment could be: 1993: $400,000 1994: $600,000 1995: $900,000 1996: $1,200,000 1997: $1,500,000 1998 and beyond: $1,600,000 To develop pro forma statements that could assist in the valuation of the firm, Roy made the following assumptions, based on his experience at PBM: 1. Pretax operating profit equals 13.5 percent of sales. 2. Taxes computed using 30 percent combined (state and federal) tax rate. 3. Additional net working capital investment equal to $8,450 in 1993 and there- after 16.9 percent of incremental sales. 242 PART VII VALUATION 4. Capital investment requirements equal to $25,000 in 1993, $30,000 in 1994, $40,000 in 1995, $60,000 both in 1996 and 1997, and $70,000 per year there- after. These capital outlays are needed to replace and recondition vehicles, sweepers, carpet cleaning equipment, and equipment and furnishings used in the main company office. 5. Annual depreciation was expected to total $5,000 in 1993, $11,000 in 1994, $20,000 in 1995, $45,000 in 1996, and $70,000 per year thereafter. 6. If the acquisition is completed, the effective date will be January 1, 1993. Under its present management, sales and profit growth was expected to be sub- stantially less than under Roy's management and ownership. Based on what he knew about the past performance of Fabricare, Roy felt that the current managers would be lucky if they could grow their 1991 yearly after-tax cash flows of $30,654 ($28,615 net income after tax plus depreciation of $2,039) by 5 percent per year. As a starting point in estimating a required return on equity, Roy used data from publicly held building maintenance and cleaning firms. This analysis led Roy to conclude that a 15 percent return on equity was suitable for firms in that industry. However, because PBM and Fabricare were privately held and suf- fered from a lack of liquidity for their owners, because of the increased risk associated with locationally nondiversified firms, and because the owners were not well-diversified with respect to their own portfolio of assets, Roy concluded that a 20 percent return on equity was appropriate for valuing both PBM and any potential acquisition in the industry. A similar analysis of publicly held firms and data from Robert Morris Associates for smaller firms in the industry indicated that a 20 percent return requirement was reasonable and achievable. This analysis also led Roy to con- clude that a capital structure containing up to 30 percent debt was typical. However, Roy did not wish to assume any liabilities associated with the Fabricare operation, because he was unsure of the business reputation of the current owners and did not want to have to deal with any outstanding claims against the current owners. Hence, he planned only to acquire the assets of Fabricare and to negotiate a "noncompete" agreement with the current owners. The assets to be acquired included fixed assets (trucks and equipment), leased property improvements, and working capital, including cash, inventories, and accounts receivable. These assets had a current book value of $154,088, but Roy felt a more reasonable liquidation value was $140,000. Roy and the Fabricare owners agreed that if an agreement to purchase was completed, the final sales price would be adjusted to reflect changes in the working capital accounts, from the amounts outstanding at year-end 1991, as shown in Exhibit 4. Roy's first problem was a valuation of Fabricare. If he sought to acquire the firm, he did not want to overpay. Fabricare did have some good contracts on which Roy felt his firm could build. These contracts, although not long-term, were with customers who had used Fabricare for several years and were thought to be loyal customers. The owners of Fabricare were asking a price of $275,000, Roy's intuition told him that this asking price was too high, given the performance of CASE 36 FABRICARE, INC. 243 Fabricare and Roy's own experience at PBM. Publidy traded building mainte- nance service firms were currently selling at a multiple of 65 percent of sales, and 8 times curent eamings. Roy had recently leamed about the concept of free cash flows and wanted to apply this valuation technique as well. Roy knew that he wanted to purchase Fabricare as an entry into the Lynchburg market. The basic questions were (1) to determine a valuation for Fabricare; (2) to determine a valuation for the combined firms; and (3) to decide how to finance the purchase of Fabricare. After these questions were answered, Roy still had to negotiate a price with the current owners of Fabricare. With these thoughts in mind, Roy got out his calculator and began his analysis. QUESTIONS 1. I Roy Tyson were to acquire Fabricare, what is the maximum amount that he court pay for the firm, assuming that the appensition is effective at the beginning of 19032 2. In the valuation of Fabricare, is trying to decide the price he is willing to pay for the firm. In a proper valuaties of Fabricare, what role should (1) the book value of the assets to be acquired from Fabricare, (2) price-to-earnings ratios for publicly traded building maintenance firms, (3) market value as a percentage of sales analysis for publicly traded firms, and (4) an estimate of the value of Fabricare under current management play in the analysis? Are there any factors that might lead you to recommend that Tyson pay less for Fabricare than the amount computed in question 1? 3. What value would you recommend as a starting point for negotiation Sales Operating expenses Salaries* Payroll taxes Supplies Subcontractor fees Repairs/maintenance Uniform expense Vehicle expense Travel Depreciation Total operating expenses Gross margin on sales EXHIBIT 1 PBM, Inc. Statement of Income 1991 1990 $851,430 497674 35,579 42371 13,008 6,643 2,721 7,529 4,925 21,882 $636,382 $216,098 $748,880 453/72 32,673 34,024 11,814 5,862 1,924 7,289 4,612 20042 $571,312 $177,568 1989 $550,140 341,543 27,577 28,716 10,181 5,322 1,297 11,180 4,585 25.101 $4.535.302 $94,638 (continued) 244 PART VII VALUATION General and administrative expenses: Accounting/professional Advertising Bank charges Conventions/meetings Contributions Insurance Office supplies Rent Retirement Taxes/licenses Utilities Current assets: Cash Inventory Note receivable Accounts receivable Total curent assets Fixed assets: Building Furniture and fixtures EXHIBIT 1 (Continued) Equipment Automobiles and trucks 1991 Less: Accumulated depreciation Net fixed assets Goodwill Total asets $12,704 1,571 3,705 1,521 2,500 35,700 8,574 10,500 10,325 7,112 9,008 9,717 1,962 7.653 Total general and administrative expenses $74,654 Income before taxes $118,445 102,914 Income taxus 31,438 30,777 Net income after taxes $87,007 $72.137 *In 1991, salaries indude $2,450 compensation to officers of PEM, Inc. (Roy and his wife). 2,110 8443 $87,653 EXHIBIT 2 PBM, Inc. Balance Sheet December 31, 1991 $47,632 3446 102,820) 102.594 $256492 $28,2986 99,741 1,984 39666 1990 (116353) 53,324 31.787 $311.603 10,180 1410 2918 1,865 2,115 20684 1989 9,328 1,270 2312 1,771 1,810 18,449 6,579 8,283 9412 3,545 6412 $69,171 $25,A67 5,632 $19,835 Damber 31, 1990 $25,666 2,997 79651 65420 $173,734 $28,286 72,978 1,514 39,666 (91471) 50,973 32.337 $2570441 (continued) Current liabilities: SUTA payable FUTA payable State withholding Federal withholding FICA withheld employee FICA accrued employer Payroll tax deposits Miscellaneous deductions Accrued wages payable Income tax provision Total cunent liabilities Long-term debt: Note payable CHB Note payable-First Virginia Total long-term debt Total liabilities Shareholders' equity: Common stock Retained eamings Total shareholders' equity Total liabilities and shareholders' equity Payroll taxes Interest CASE 36 FABRICARE, INC. 245 EXHIBIT 2 (Continued) Depreciation Advertising Supplies Office expense Other expenses December 31, 1991 $1,063 (487) 1,640 32468 34040 33,611 (104,281) 15467 16,922 (5,580) $24,863 Sales Operating, general, and administrative expenses: Salaries and wages Rent $230 280083 3033 $27,896 $38400 275307 $313,707 $341,603 December 31, 1990 EXHIBIT 3 Fabricare, Inc. Statement of Income, 1991 (unaudited) Total operating, general, and administrative expenses Income before taxes Income taxes Net income after taxes $1,570 3,008 580 25,127 27,899 30,802 (92,334) 5,296 19,179 (1428) $19,099 $743 9.902 $10,645 $30,344 $38400 $188.3000 $226,7000 257044 $384,385 $172,816 3498 54,763 2,885 20139 8,856 54,525 10,732 38.702 $348.616 $35,769 7.154 $28,615 246 PART VII VALUATION EXHIBIT 4 Fabricare, Inc. Balance Sheet, December 31, 1991 (unaudited) Cunent assets: Cash Accounts receivable Inventory Total current assets Fixed assets: Furniture, fixtures and equipment Automobiles and trucks Less: Accumulated depreciation Net fixed assets Total assets Cunent liabilities: SUTA payable FUTA payable State withholding Federal withholding HCA withheld-employee HCA acued employer Payroll tax deposits Miscellaneous deductions Accrued wages payable Income tax provision Total current liabilities Long-term debe Note payable Total liabilities Shareholders' equity: Common stock Retained eamings Total shareholders' equity Total liabilities and shareholders' equity $29,052 56,167 884 $93,803 $19,651 39,522 $60,285 $154,088 $855 247 995 20006 21,771 18,643 (51,587) 11,212 9,918 (3.312) $28,748 $12,500 $41,248 $25,000 87,840 $112,840 $154,088 In early 1986, Roy Tyson purchased Professional Building Maintenance, Inc. (PBM), a building maintenance and cleaning firm located and operating in the Danville, Virginia area. The firm specialized in providing cleaning services in commercial and professional offices, such as banks, law offices, and medical practices. Over the next 5 years, revenues increased more than 400 percent, from $212,100 to $851,430 in 1991 (see Exhibit 1 and 2). The revenue growth rate slowed in 1991 as PBM's market share (currently 40 percent) in the area expanded and the potential new prospect pool declined. Roy was confident that the expertise he had gained while operating PBM could be applied successfully to similar firms in other geographical markets that possessed greater growth potential than Danville. In 1992, he learned that a building maintenance firm, Fabricare, Inc., located in Lynchburg, Virginia, was for sale. Fabricare's most recent (year- end 1991) revenues were less than one-half of those of PBM, but Roy believed the growth potential to be much greater because Fabricare had only a small share (approximately 10 percent) of the Lynchburg market. As he looked over the 1991 income statement and balance sheet for Fabricare, Roy was try- ing to decide (1) if he should purchase the company and (2) if so, at what price. Fabricare, like PBM, was in the building maintenance business, but approxi- mately one-half of its revenues came from commercial establishment carpet cleaning. The owner of Fabricare was approaching retirement age and no prepa- ration had been made for management succession in the small firm. On investigation, Roy learned that Fabricare had about $384,000 in revenues in 1991, a figure that had grown only modestly over the previous three years (Exhibit 3 is a 1991 income statement, derived from Fabricare's 1991 tax return. Exhibit 4 is an unaudited 1991 balance sheet for Fabricare). Fabricare's current owners were not much on keeping careful records. Past income records were not reliable in Roy's judgment. Hence, the decision regarding acquisition of Fabricare had to be based primarily on Roy's own projections of cash flows from Fabricare and on an appraisal of the quality of the assets that would be acquired. In assessing Fabricare's market position, Roy visited the competitors' prem- ises noting, in particular, the number of service vehicles that each business had available. Although a relatively crude method of measuring the business activ- ity level of each firm and relative market shares, he had found this to be a fairly accurate indicator in the Danville area. From these observations, Roy believed that Fabricare had only a 10 percent share of the building maintenance business in Lynchburg, In addition, Roy learned from some of the local firms that made use of building maintenance services in Lynchburg that the bidding techniques and performance standards were similar to those he had experienced from his competitors in Danville. Lynchburg had a larger business and professional community than Danville and offered greater immediate growth potential than existed in the saturated Danville market. Upon a closer examination of Fabricare, Roy saw a firm whose business could be expanded from its current customer base into a more success- ful, full-service building maintenance firm like PBM. Roy felt strongly that he could capture about the same market share (40 percent) in Lynchburg as he had in Danville. Beyond that level, Roy found additional market share difficult to obtain from customers who often were more concerned about cost considera- tions than quality of performance. Roy also considered a startup operation, but he concluded that the pur- chase of an existing firm would give him quicker access to the market. In addition to the current customer base, he would also obtain employees who were familiar with the business and the area. Based on an estimate of the cur- rent and future total market for building maintenance services in Lynchburg and a projection of Fabricare's market penetration that matched the historical performance of PBM, Roy estimated that sales revenues under his manage- ment could be: 1993: $400,000 1994: $600,000 1995: $900,000 1996: $1,200,000 1997: $1,500,000 1998 and beyond: $1,600,000 To develop pro forma statements that could assist in the valuation of the firm, Roy made the following assumptions, based on his experience at PBM: 1. Pretax operating profit equals 13.5 percent of sales. 2. Taxes computed using 30 percent combined (state and federal) tax rate. 3. Additional net working capital investment equal to $8,450 in 1993 and there- after 16.9 percent of incremental sales. 242 PART VII VALUATION 4. Capital investment requirements equal to $25,000 in 1993, $30,000 in 1994, $40,000 in 1995, $60,000 both in 1996 and 1997, and $70,000 per year there- after. These capital outlays are needed to replace and recondition vehicles, sweepers, carpet cleaning equipment, and equipment and furnishings used in the main company office. 5. Annual depreciation was expected to total $5,000 in 1993, $11,000 in 1994, $20,000 in 1995, $45,000 in 1996, and $70,000 per year thereafter. 6. If the acquisition is completed, the effective date will be January 1, 1993. Under its present management, sales and profit growth was expected to be sub- stantially less than under Roy's management and ownership. Based on what he knew about the past performance of Fabricare, Roy felt that the current managers would be lucky if they could grow their 1991 yearly after-tax cash flows of $30,654 ($28,615 net income after tax plus depreciation of $2,039) by 5 percent per year. As a starting point in estimating a required return on equity, Roy used data from publicly held building maintenance and cleaning firms. This analysis led Roy to conclude that a 15 percent return on equity was suitable for firms in that industry. However, because PBM and Fabricare were privately held and suf- fered from a lack of liquidity for their owners, because of the increased risk associated with locationally nondiversified firms, and because the owners were not well-diversified with respect to their own portfolio of assets, Roy concluded that a 20 percent return on equity was appropriate for valuing both PBM and any potential acquisition in the industry. A similar analysis of publicly held firms and data from Robert Morris Associates for smaller firms in the industry indicated that a 20 percent return requirement was reasonable and achievable. This analysis also led Roy to con- clude that a capital structure containing up to 30 percent debt was typical. However, Roy did not wish to assume any liabilities associated with the Fabricare operation, because he was unsure of the business reputation of the current owners and did not want to have to deal with any outstanding claims against the current owners. Hence, he planned only to acquire the assets of Fabricare and to negotiate a "noncompete" agreement with the current owners. The assets to be acquired included fixed assets (trucks and equipment), leased property improvements, and working capital, including cash, inventories, and accounts receivable. These assets had a current book value of $154,088, but Roy felt a more reasonable liquidation value was $140,000. Roy and the Fabricare owners agreed that if an agreement to purchase was completed, the final sales price would be adjusted to reflect changes in the working capital accounts, from the amounts outstanding at year-end 1991, as shown in Exhibit 4. Roy's first problem was a valuation of Fabricare. If he sought to acquire the firm, he did not want to overpay. Fabricare did have some good contracts on which Roy felt his firm could build. These contracts, although not long-term, were with customers who had used Fabricare for several years and were thought to be loyal customers. The owners of Fabricare were asking a price of $275,000, Roy's intuition told him that this asking price was too high, given the performance of CASE 36 FABRICARE, INC. 243 Fabricare and Roy's own experience at PBM. Publidy traded building mainte- nance service firms were currently selling at a multiple of 65 percent of sales, and 8 times curent eamings. Roy had recently leamed about the concept of free cash flows and wanted to apply this valuation technique as well. Roy knew that he wanted to purchase Fabricare as an entry into the Lynchburg market. The basic questions were (1) to determine a valuation for Fabricare; (2) to determine a valuation for the combined firms; and (3) to decide how to finance the purchase of Fabricare. After these questions were answered, Roy still had to negotiate a price with the current owners of Fabricare. With these thoughts in mind, Roy got out his calculator and began his analysis. QUESTIONS 1. I Roy Tyson were to acquire Fabricare, what is the maximum amount that he court pay for the firm, assuming that the appensition is effective at the beginning of 19032 2. In the valuation of Fabricare, is trying to decide the price he is willing to pay for the firm. In a proper valuaties of Fabricare, what role should (1) the book value of the assets to be acquired from Fabricare, (2) price-to-earnings ratios for publicly traded building maintenance firms, (3) market value as a percentage of sales analysis for publicly traded firms, and (4) an estimate of the value of Fabricare under current management play in the analysis? Are there any factors that might lead you to recommend that Tyson pay less for Fabricare than the amount computed in question 1? 3. What value would you recommend as a starting point for negotiation Sales Operating expenses Salaries* Payroll taxes Supplies Subcontractor fees Repairs/maintenance Uniform expense Vehicle expense Travel Depreciation Total operating expenses Gross margin on sales EXHIBIT 1 PBM, Inc. Statement of Income 1991 1990 $851,430 497674 35,579 42371 13,008 6,643 2,721 7,529 4,925 21,882 $636,382 $216,098 $748,880 453/72 32,673 34,024 11,814 5,862 1,924 7,289 4,612 20042 $571,312 $177,568 1989 $550,140 341,543 27,577 28,716 10,181 5,322 1,297 11,180 4,585 25.101 $4.535.302 $94,638 (continued) 244 PART VII VALUATION General and administrative expenses: Accounting/professional Advertising Bank charges Conventions/meetings Contributions Insurance Office supplies Rent Retirement Taxes/licenses Utilities Current assets: Cash Inventory Note receivable Accounts receivable Total curent assets Fixed assets: Building Furniture and fixtures EXHIBIT 1 (Continued) Equipment Automobiles and trucks 1991 Less: Accumulated depreciation Net fixed assets Goodwill Total asets $12,704 1,571 3,705 1,521 2,500 35,700 8,574 10,500 10,325 7,112 9,008 9,717 1,962 7.653 Total general and administrative expenses $74,654 Income before taxes $118,445 102,914 Income taxus 31,438 30,777 Net income after taxes $87,007 $72.137 *In 1991, salaries indude $2,450 compensation to officers of PEM, Inc. (Roy and his wife). 2,110 8443 $87,653 EXHIBIT 2 PBM, Inc. Balance Sheet December 31, 1991 $47,632 3446 102,820) 102.594 $256492 $28,2986 99,741 1,984 39666 1990 (116353) 53,324 31.787 $311.603 10,180 1410 2918 1,865 2,115 20684 1989 9,328 1,270 2312 1,771 1,810 18,449 6,579 8,283 9412 3,545 6412 $69,171 $25,A67 5,632 $19,835 Damber 31, 1990 $25,666 2,997 79651 65420 $173,734 $28,286 72,978 1,514 39,666 (91471) 50,973 32.337 $2570441 (continued) Current liabilities: SUTA payable FUTA payable State withholding Federal withholding FICA withheld employee FICA accrued employer Payroll tax deposits Miscellaneous deductions Accrued wages payable Income tax provision Total cunent liabilities Long-term debt: Note payable CHB Note payable-First Virginia Total long-term debt Total liabilities Shareholders' equity: Common stock Retained eamings Total shareholders' equity Total liabilities and shareholders' equity Payroll taxes Interest CASE 36 FABRICARE, INC. 245 EXHIBIT 2 (Continued) Depreciation Advertising Supplies Office expense Other expenses December 31, 1991 $1,063 (487) 1,640 32468 34040 33,611 (104,281) 15467 16,922 (5,580) $24,863 Sales Operating, general, and administrative expenses: Salaries and wages Rent $230 280083 3033 $27,896 $38400 275307 $313,707 $341,603 December 31, 1990 EXHIBIT 3 Fabricare, Inc. Statement of Income, 1991 (unaudited) Total operating, general, and administrative expenses Income before taxes Income taxes Net income after taxes $1,570 3,008 580 25,127 27,899 30,802 (92,334) 5,296 19,179 (1428) $19,099 $743 9.902 $10,645 $30,344 $38400 $188.3000 $226,7000 257044 $384,385 $172,816 3498 54,763 2,885 20139 8,856 54,525 10,732 38.702 $348.616 $35,769 7.154 $28,615 246 PART VII VALUATION EXHIBIT 4 Fabricare, Inc. Balance Sheet, December 31, 1991 (unaudited) Cunent assets: Cash Accounts receivable Inventory Total current assets Fixed assets: Furniture, fixtures and equipment Automobiles and trucks Less: Accumulated depreciation Net fixed assets Total assets Cunent liabilities: SUTA payable FUTA payable State withholding Federal withholding HCA withheld-employee HCA acued employer Payroll tax deposits Miscellaneous deductions Accrued wages payable Income tax provision Total current liabilities Long-term debe Note payable Total liabilities Shareholders' equity: Common stock Retained eamings Total shareholders' equity Total liabilities and shareholders' equity $29,052 56,167 884 $93,803 $19,651 39,522 $60,285 $154,088 $855 247 995 20006 21,771 18,643 (51,587) 11,212 9,918 (3.312) $28,748 $12,500 $41,248 $25,000 87,840 $112,840 $154,088

Expert Answer:

Related Book For

Posted Date:

Students also viewed these accounting questions

-

While securities markets are generally believed to be efficient, there appear to be some exceptions. For these exceptions (i.e., the anomalies) to be important for the individual investor, what must...

-

Firm S plans to sell an office building via an English auction. The firm expects two buyers to bid, each with a value uniformly distributed between $300,000 and $360,000. In addition, firm S knows it...

-

Banks hold more liquid assets than do most businesses. Explain why.

-

The specifications for the water supply system of the Sears Tower in Chicago require that 100 gpm of water be pumped to a reservoir at the top of the tower, which is 340 m above street level. The...

-

What is a key and what is it used for?

-

In Exercises 1 and 2, use the figure, which shows two lines whose equations are y1 = m1x + b1 and y2 = m2x + b2. Assume that both lines have positive slopes. Derive a formula for the angle between...

-

How to amend a pleading once it is filed with the court?

-

The Fanta Company presents you with the following account balances taken from its December 31, 2007 adjusted trial balance: Inventory, January 1, 2007 ............. $ 43,000 Selling expenses...

-

Lem E Tweakit Inc. is considering the purchase of a new magic marker machine. This machine will reduce manufacturing costs by $6,000 annually. The new machine will be in CCA class 8 (d = 20%). The...

-

Arthur, CPA, is auditing The Home Improvement Store as of December 31, 2021. As with all audit engagements, Arthur's initial procedures are to analyze the entity's financial data by reviewing trends...

-

Suzuki Supply reports the following amounts at the end of 2018 (before adjustment) Credit Sales for 2018....$260,000 Accounts Receivable, December 31, 201855,000 Allowance for Uncollectible Accounts,...

-

A poll is being conducted on a college campus to obtain a sample of the population of an entire country. What is the frame for this type of sampling? Who would be excluded from the survey and how...

-

Favorite movie Determine the level of measurement of each variable.

-

A web page design firm has two designs for an online hardware store. To determine the more effective design, the firm uses one page with only teenage visitors and a second page with only adult...

-

For a poll of voters regarding a referendum calling for a national value-added tax, design a sampling method to obtain the individuals in the sample. Be sure to support your choice. Which sampling...

-

Suppose a surveyor wants to conduct a phone survey about a new car. She plans to take a simple random sample. However, some people do not want to participate. Do you believe this can affect the...

-

For the system shown below, determine the following: A) Draw the free-body-diagram. B) Find the two equations of motion. C) Write the equations of motion in matrix form. D) Find the steady-state...

-

5. How much would you need to deposit in an account now in order to have $5,000 in the account in 5 years? Assume the account earns 2% interest compounded monthly. 10. You deposit $300 each month...

-

Oshawa Motors is a car dealership that has two types of operations: car sales and service. The two divisions operate independently and, in fact, the showroom for car sales is entirely separate from...

-

Tymens financial statements as at December 31, 2019, appear below (PPE denotes property, plant, and equipment): Tymen Ltd. Income Statement For the Year Ended December 31, 2019 Sales...

-

The CPA Canada Handbook is available to most post-secondary students through their institutions subscription. Visit http://edu.knotia.ca to complete this exercise. (You may need to complete this...

-

What forms of business organization are permitted under Rule 505-Form of Practice and Firm Name?

-

There currently are thirteen Rules of Conduct. Listed below are circumstances pertaining to some of these rules: 1. A member shall exercise due professional care in the performance of an engagement....

-

a. What aspects of a company's financial statements are covered in the first three reporting standards? b. What is the objective of the fourth standard of reporting?

Study smarter with the SolutionInn App