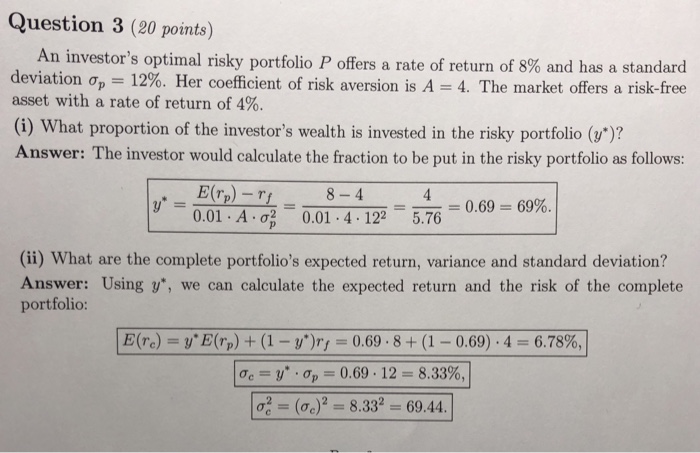

Question: In (i), what does the .01 stand for? (where did it come from?). Question 3 (20 points) An investor's optimal risky portfolio P offers a

Question 3 (20 points) An investor's optimal risky portfolio P offers a rate of return of 8% and has a standard deviation p-12%. Her coefficient of risk aversion is A-4. The market offers a risk-free asset with a rate of return of 4%. (i) What proportion of the investor's wealth is invested in the risky portfolio (u)? Answer: The investor would calculate the fraction to be put in the risky portfolio as follows: E(rn)- 0.01 : A . 2-0.01-4-122 4 5.76 = 0.09-b9% (ii) What are the complete portfolio's expected return, variance and standard deviation? Answer: Using y, we can calculate the expected return and the risk of the complete portfolio: E(re) = y*E(rp) + (1-y*)ry = 0.69 . 8 + (1-0.69) . 4 = 6.78%, 0c = y* Op = 0.69 , 12 = 8.33%. -(%)2 = 8.332 = 69.44

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts