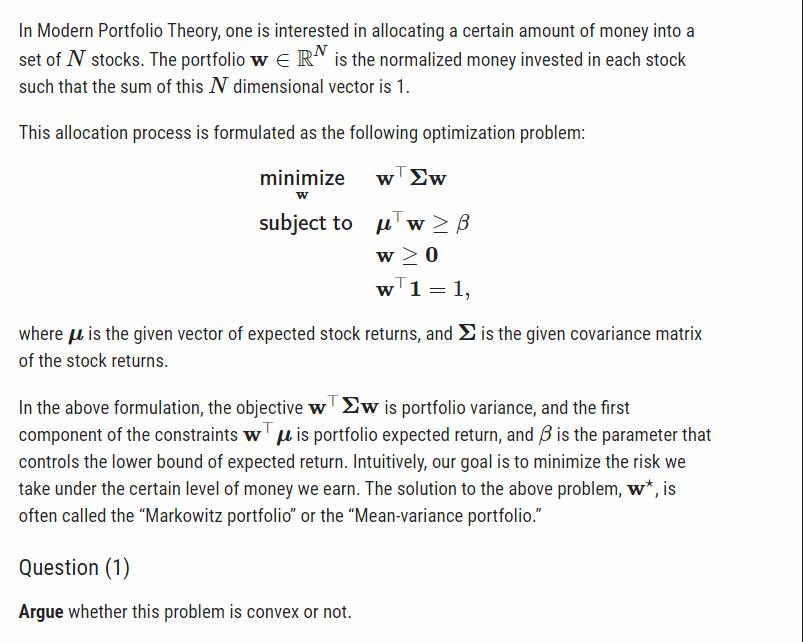

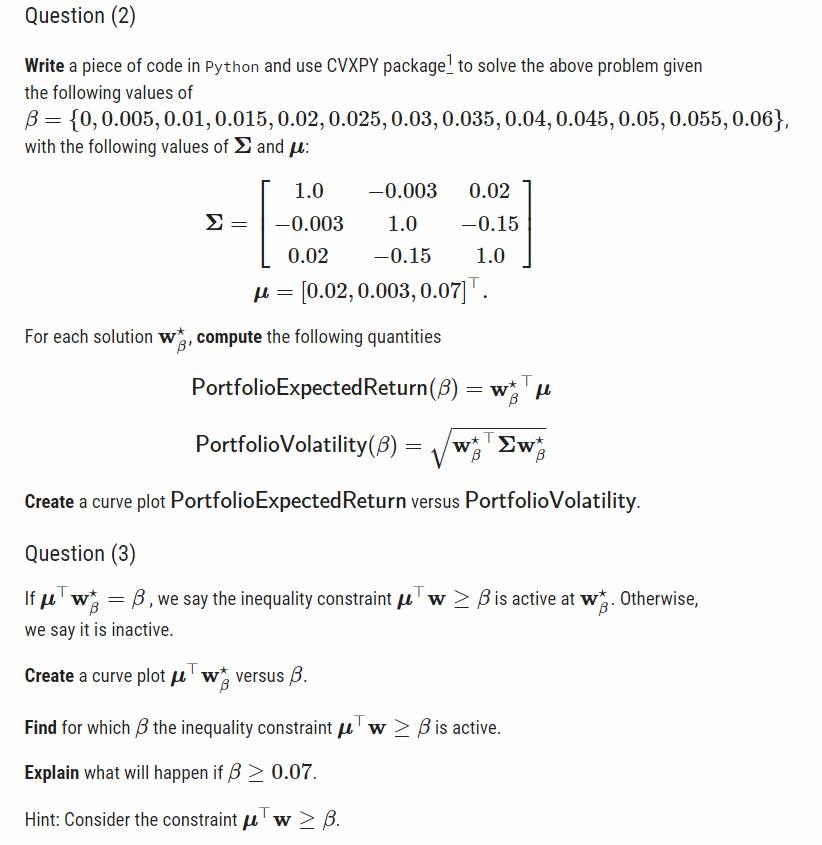

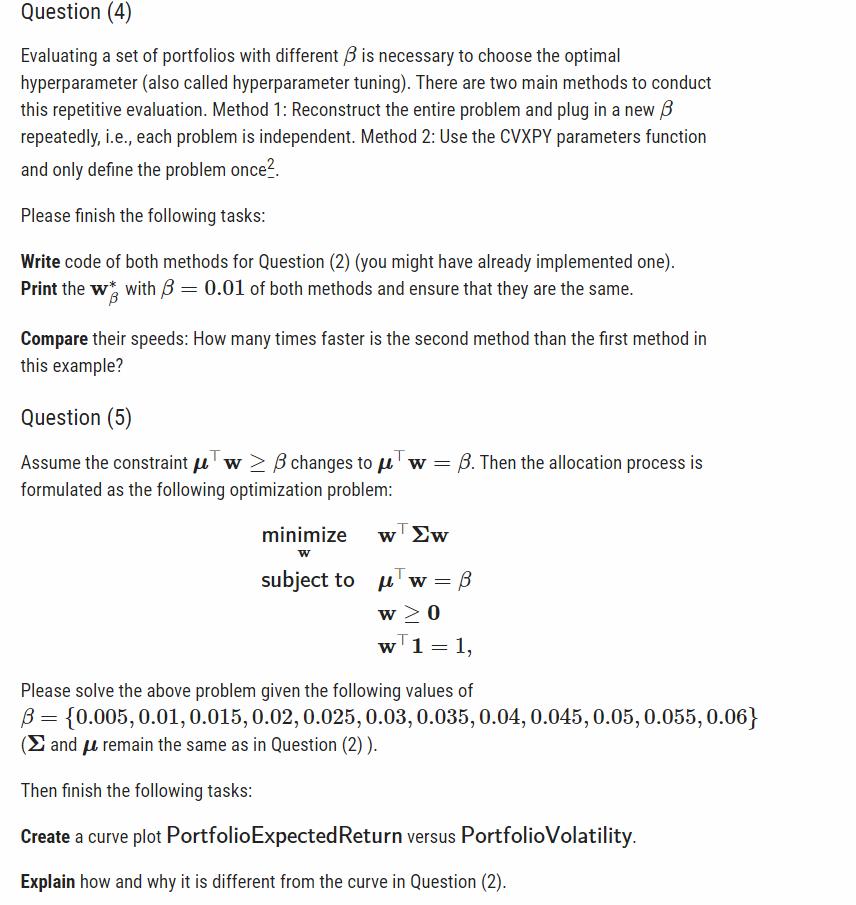

In Modern Portfolio Theory, one is interested in allocating a certain amount of money into a...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Question 1 The given optimization problem is a convex problem To show this we need to prove that the objective function and the constraints satisfy the conditions for convexity Objective Function The ... View the full answer

Related Book For

Posted Date: