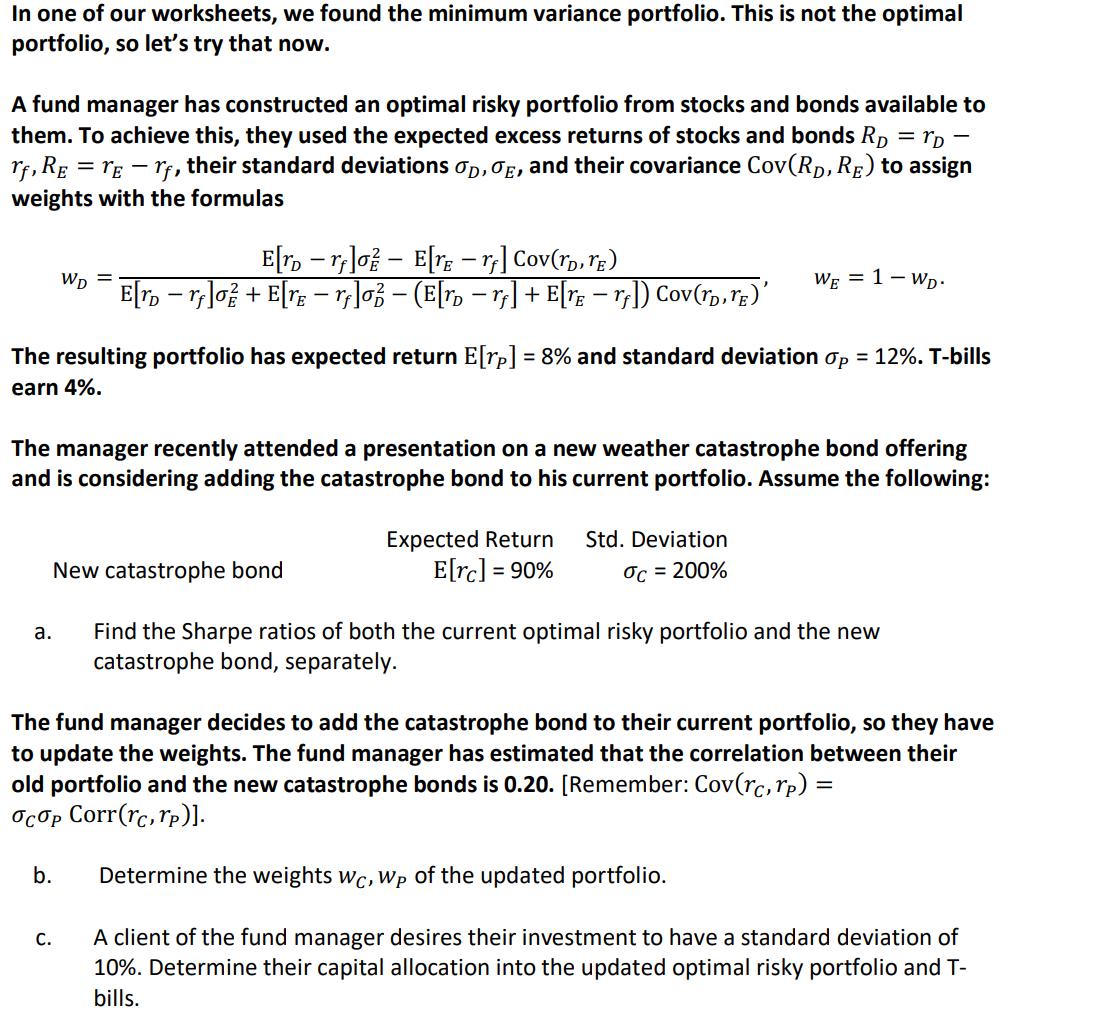

In one of our worksheets, we found the minimum variance portfolio. This is not the optimal...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a The Sharpe ratio is calculated as the excess return of an assetportfolio divided by its standard d... View the full answer

Related Book For

Posted Date: