Question: In performing the audit, an auditor basically, considers what would make the financial statements materially misstated. Materially is defined as the magnitude or omission or

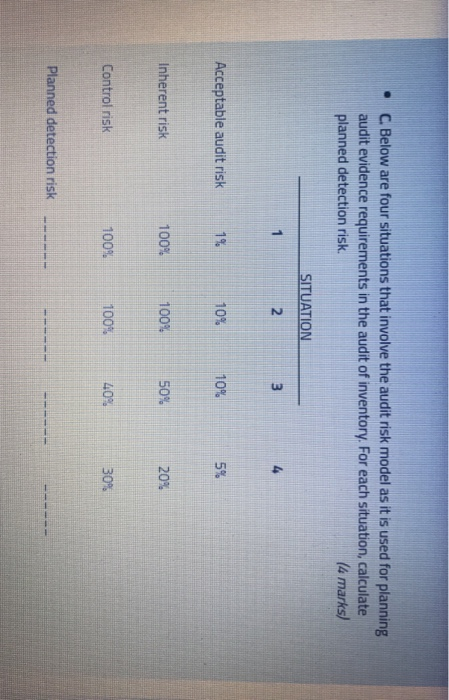

In performing the audit, an auditor basically, considers what would make the financial statements materially misstated. Materially is defined as the magnitude or omission or misstatement of accounting information that, in the judgment of a reasonable person relying on the information, would have been changed or influenced by the omission or misstatement. The auditor's assessment of materiality, related to specific account balances and classes of transactions, helps the auditor decide such questions as what items to examine and whether to use sampling and analytical procedures. This enables the auditor to select audit procedures that, in combination, can be expected to reduce audit risk to an acceptably low level. There is an inverse relationship between materiality and the level of audit risk, that is, the higher the materiality level, the lower the audit risk and vice versa. The auditor takes the inverse relationship between materiality and audit risk into account when determining the nature, timing, and extent of audit procedures. Required: a Briefly explain with relevant example any TWO factors affecting auditor's judgment on materiality (2 marks) (4 marks/ b. Briefly explain with relevant example the following risks: Inherent risk Control risk Detection risk . C. Below are four situations that involve the audit risk model as it is used for planning audit evidence requirements in the audit of inventory. For each situation, calculate planned detection risk. (4 marks) SITUATION 1 2 3 Acceptable audit risk 1% 10% 10% 5% Inherent risk 100% 100% 50% 20% Control risk 100%. 100% 40% 30% Planned detection risk

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts