Question: In this problem, you are asked to simulate the payoffs of a covered call over 52 weeks, with weekly updating of the positions. Start by

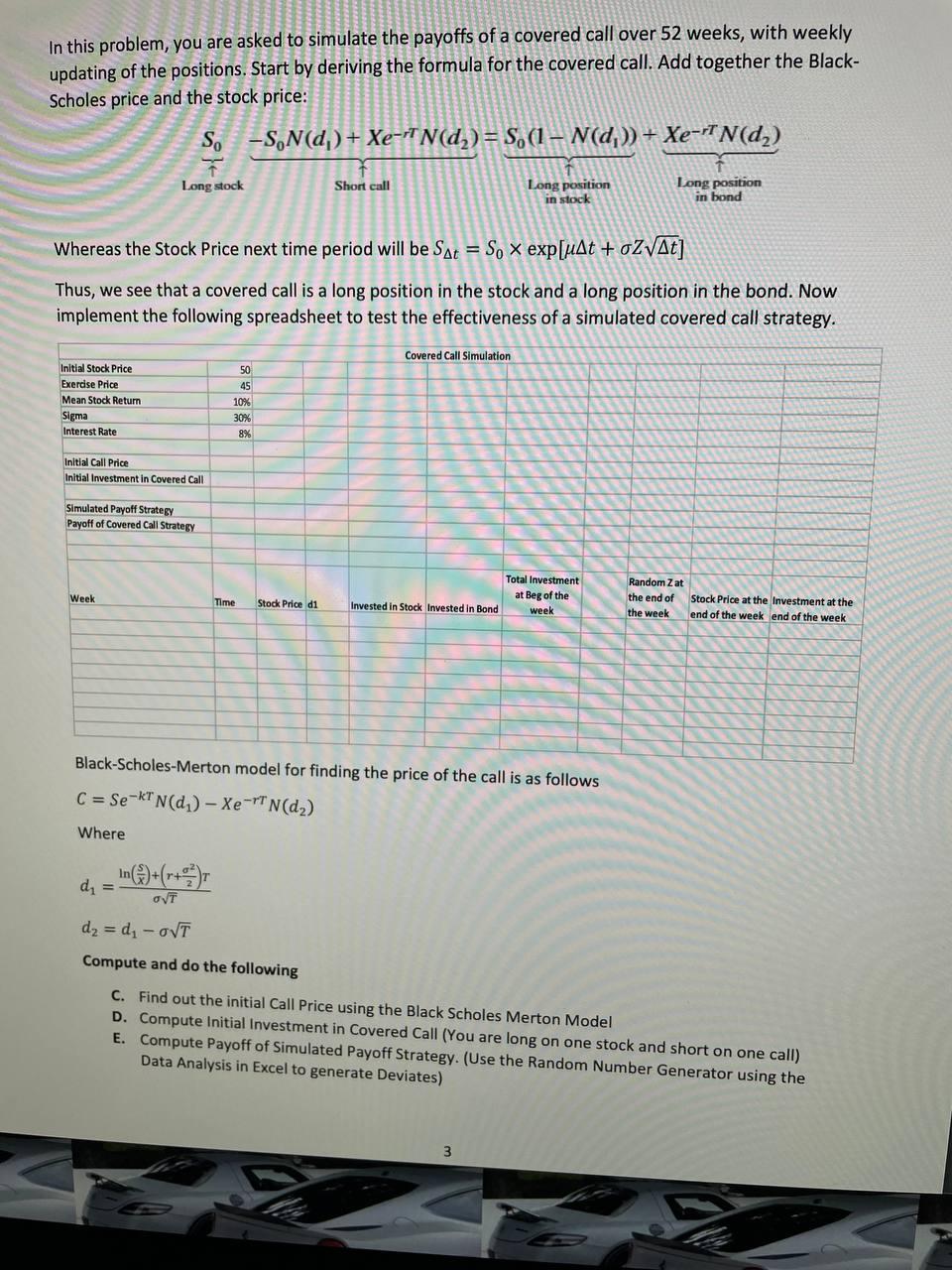

In this problem, you are asked to simulate the payoffs of a covered call over 52 weeks, with weekly updating of the positions. Start by deriving the formula for the covered call. Add together the BlackScholes price and the stock price: Whereas the Stock Price next time period will be St=S0exp[t+Zt] Thus, we see that a covered call is a long position in the stock and a long position in the bond. Now implement the following spreadsheet to test the effectiveness of a simulated covered call strategy. oratn-scnoies-Iverton model for finding the price of the call is as follows C=SekTN(d1)XerTN(d2) Where d1=Tln(xS)+(r+22)Td2=d1T Compute and do the following C. Find out the initial Call Price using the Black Scholes Merton Model D. Compute Initial Investment in Covered Call (You are long on one stock and short on one call) E. Compute Payoff of Simulated Payoff Strategy. (Use the Random Number Generator using the Data Analysis in Excel to generate Deviates) F. Fill in the above table for 52 weeks. ( t= 2501 for daily time change, use this information to compute t for week) In this problem, you are asked to simulate the payoffs of a covered call over 52 weeks, with weekly updating of the positions. Start by deriving the formula for the covered call. Add together the BlackScholes price and the stock price: Whereas the Stock Price next time period will be St=S0exp[t+Zt] Thus, we see that a covered call is a long position in the stock and a long position in the bond. Now implement the following spreadsheet to test the effectiveness of a simulated covered call strategy. oratn-scnoies-Iverton model for finding the price of the call is as follows C=SekTN(d1)XerTN(d2) Where d1=Tln(xS)+(r+22)Td2=d1T Compute and do the following C. Find out the initial Call Price using the Black Scholes Merton Model D. Compute Initial Investment in Covered Call (You are long on one stock and short on one call) E. Compute Payoff of Simulated Payoff Strategy. (Use the Random Number Generator using the Data Analysis in Excel to generate Deviates) F. Fill in the above table for 52 weeks. ( t= 2501 for daily time change, use this information to compute t for week)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts