Question: initial 4% rate, so it contracts with the bank to swap its variable-interest-rate obligation for a fixed- interest-rate obligation. The swap fixes the firm's annual

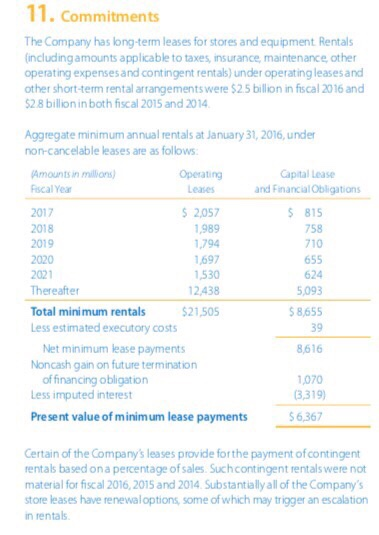

initial 4% rate, so it contracts with the bank to swap its variable-interest-rate obligation for a fixed- interest-rate obligation. The swap fixes the firm's annual interest expense and cash expenditure to 4% of the $500,000 note. FD designates the swap contract as a cash flow hedge. INTEGRATIVE CASE 7.1 Walmart It is common practice for retail outlets to lease their store locations and distribution centers. Walmart is no exception. Note 11 to Walmart's consolidated financial statements for the fiscal year ending January 31, 2016 (found online at the text website or available for download in the investor relations section of Walmart's website), provides information on future operating lease commitments. REQUIRED a. Effectively capitalize the operating lease obligations. You must first choose and justify an interest rate. Assume that all cash flows occur at the end of each year. b. Recompute the long-term debt to long-term capital ratio (see Chapter 5) using your capi- talized operating leases. Comment on the results. CASE 7.2 IT. Commitments The Company has long-term leases for stores and equipment Rentals (includingamounts applicable to taxes, insurance, maintenance other operating expenses and contingent rentals) under operating leases and other short-term rental arrangementswere $2.5 billion in fiscal 2016 and 52 8 billion in both fiscal 2015 and 2014 Aggregate minimum annual rentals at January 31, 2016,under non-cancelable leases are as follows Operating Leases Capital Lease and Financial Obligations Amounts in millions) Fscal Year 2017 2018 2019 2020 2021 Thereafter Total minimum rentals Less estimated executory costs 2057 1,989 1,794 697 1,530 12,438 $21,505 815 758 710 655 624 5,093 58,655 39 Net minimum lease payments Noncash gain on future termination 8,616 of financing obligation Less imputed interest 1070 3,319) 6,367 Pre sent value of minimum lease payments Certain of the Company's leases provide forthe payment of contingent rentals based on a percentage of sales. Suchcontingent rentals were not material for fiscal 2016, 2015 and 2014 Substantially all of the Company's store leases have renewal options, some of which may trigger an escalation n rentals CHAPTER Risk Analysis LEARNING OBJECTIVES LO 5-1 Understand required disclosures about a firm's risk exposures and risk LO 5-2 Define financial flexibility and decompose the return on common equity to LO 5-3 Apply analytical tools to assess working capital management and short-term LO 5-4 Explain the benefits and risks of financial leverage and apply analytical tools to LO 5-5 Use risk analysis tools to assess credit risk LO 5-6 Apply predictive statistical models to assess bankruptcy risk management activities. assess financial flexibility liquidity risk assess long-term solvency risk LO 5- Recognize the distinction between firm-specific risks, indicated by various financial statement ratios, and systematic risk, estimated with market equity beta. Chapter Overview he concept of risk means different things to different people because the poten tial consequences of risk differ across different contexts and stakeholders. As a result, there are numerous definitions of risk. A general definition is that risk involves exposure to a specified type of loss. The more specific definition of risk depends on the loss of interest. For example, equity investors make investment deci- sions based on the expected return from equity investments relative to the risks that such investments will fail to generate the expected level of returns, or, worse, lose money. Similarly, lenders make lending decisions based on the expected return in the form of interest revenue relative to the risks of the borrower defaulting on repay ments. The analysis of risk is central to any decision to commit economic resources to a project or an investment. initial 4% rate, so it contracts with the bank to swap its variable-interest-rate obligation for a fixed- interest-rate obligation. The swap fixes the firm's annual interest expense and cash expenditure to 4% of the $500,000 note. FD designates the swap contract as a cash flow hedge. INTEGRATIVE CASE 7.1 Walmart It is common practice for retail outlets to lease their store locations and distribution centers. Walmart is no exception. Note 11 to Walmart's consolidated financial statements for the fiscal year ending January 31, 2016 (found online at the text website or available for download in the investor relations section of Walmart's website), provides information on future operating lease commitments. REQUIRED a. Effectively capitalize the operating lease obligations. You must first choose and justify an interest rate. Assume that all cash flows occur at the end of each year. b. Recompute the long-term debt to long-term capital ratio (see Chapter 5) using your capi- talized operating leases. Comment on the results. CASE 7.2 IT. Commitments The Company has long-term leases for stores and equipment Rentals (includingamounts applicable to taxes, insurance, maintenance other operating expenses and contingent rentals) under operating leases and other short-term rental arrangementswere $2.5 billion in fiscal 2016 and 52 8 billion in both fiscal 2015 and 2014 Aggregate minimum annual rentals at January 31, 2016,under non-cancelable leases are as follows Operating Leases Capital Lease and Financial Obligations Amounts in millions) Fscal Year 2017 2018 2019 2020 2021 Thereafter Total minimum rentals Less estimated executory costs 2057 1,989 1,794 697 1,530 12,438 $21,505 815 758 710 655 624 5,093 58,655 39 Net minimum lease payments Noncash gain on future termination 8,616 of financing obligation Less imputed interest 1070 3,319) 6,367 Pre sent value of minimum lease payments Certain of the Company's leases provide forthe payment of contingent rentals based on a percentage of sales. Suchcontingent rentals were not material for fiscal 2016, 2015 and 2014 Substantially all of the Company's store leases have renewal options, some of which may trigger an escalation n rentals CHAPTER Risk Analysis LEARNING OBJECTIVES LO 5-1 Understand required disclosures about a firm's risk exposures and risk LO 5-2 Define financial flexibility and decompose the return on common equity to LO 5-3 Apply analytical tools to assess working capital management and short-term LO 5-4 Explain the benefits and risks of financial leverage and apply analytical tools to LO 5-5 Use risk analysis tools to assess credit risk LO 5-6 Apply predictive statistical models to assess bankruptcy risk management activities. assess financial flexibility liquidity risk assess long-term solvency risk LO 5- Recognize the distinction between firm-specific risks, indicated by various financial statement ratios, and systematic risk, estimated with market equity beta. Chapter Overview he concept of risk means different things to different people because the poten tial consequences of risk differ across different contexts and stakeholders. As a result, there are numerous definitions of risk. A general definition is that risk involves exposure to a specified type of loss. The more specific definition of risk depends on the loss of interest. For example, equity investors make investment deci- sions based on the expected return from equity investments relative to the risks that such investments will fail to generate the expected level of returns, or, worse, lose money. Similarly, lenders make lending decisions based on the expected return in the form of interest revenue relative to the risks of the borrower defaulting on repay ments. The analysis of risk is central to any decision to commit economic resources to a project or an investment

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts