Question: Instructions: At various points in this assignment, you will need to include Mathematica code. Include this code and output as it is used in each

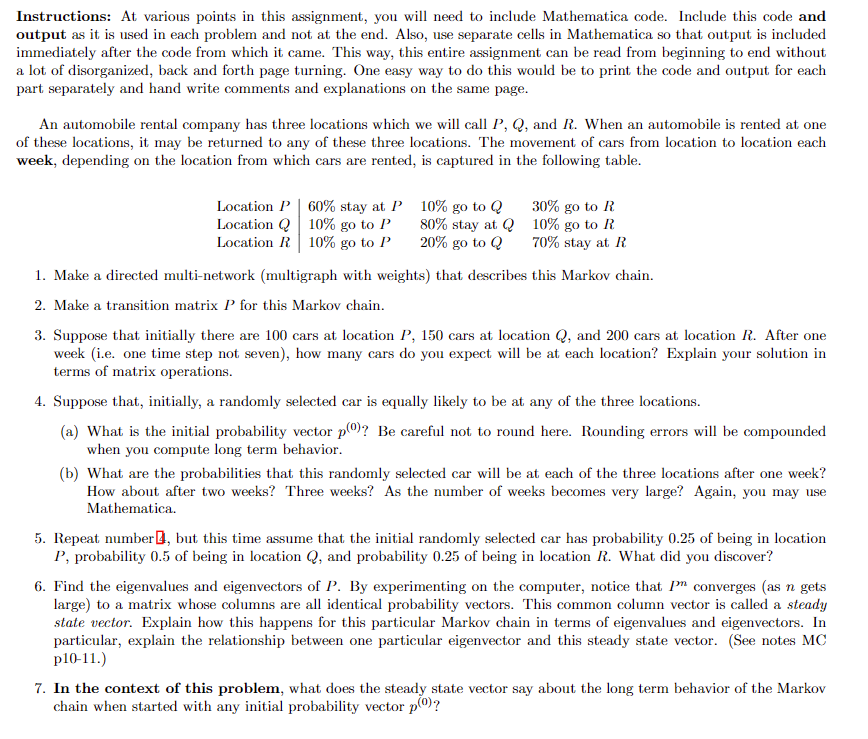

Instructions: At various points in this assignment, you will need to include Mathematica code. Include this code and output as it is used in each problem and not at the end. Also, use separate cells in Mathematica so that output is included immediately after the code from which it came. This way, this entire assignment can be read from beginning to end without a lot of disorganized, back and forth page turning. One easy way to do this would be to print the code and output for each part separately and hand write comments and explanations on the same page An automobile rental company has three locations which we will call P, Q, and R. When an automobile is rented at one of these locations, it may be returned to any of these three locations. The movement of cars from location to location each week, depending on the location from which cars are rented, is captured in the following table Location P | 60% stay at 1, Location Q | 10% go to P Location 11 | 10% go to P 10% go to Q 30% go to 11 80% stay at Q10% go to 11 20% go to Q 70% stay at 11 1. Make a directed multi-network (multigraph with weights) that describes this Markov chain. 2. Make a transition matrix P for this Markov chain 3. Suppose that initially there are 100 cars at location P, 150 cars at location Q, and 200 cars at location R. After one week (i.e. one time step not seven), how many cars do you expect will be at each location? Explain your solution in terms of matrix operations. 4. Suppose that, initially, a randomly selected car is equally likely to be at any of the three locations. (a) What is the initial probability vector po? Be careful not to round here. Rounding errors will be compounded when you compute long term behavior (b) What are the probabilities that this randomly selected car will be at each of the three locations after one week? How about after two weeks? Three weeks? As the number of weeks becomes very large? Again, you may use Mathematica 5. Repeat number, but this time assume that the initial randomly selected car has probability 0.25 of being in location P, probability 0.5 of being in location Q, and probability 0.25 of being in location R. What did you discover? 6. Find the eigenvalues and eigenvectors of P. By experimenting on the computer, notice that In converges (as n gets large) to a matrix whose columns are all identical probability vectors. This common column vector is called a steady state vector. Explain how this happens for this particular Markov chain in terms of eigenvalues and eigenvectors. In particular, explain the relationship between one particular eigenvector and this steady state vector. (See notes MC p10-11.) 7. In the context of this problem, what does the steady state vector say about the long term behavior of the Markov chain when started with any initial probability vector p? Instructions: At various points in this assignment, you will need to include Mathematica code. Include this code and output as it is used in each problem and not at the end. Also, use separate cells in Mathematica so that output is included immediately after the code from which it came. This way, this entire assignment can be read from beginning to end without a lot of disorganized, back and forth page turning. One easy way to do this would be to print the code and output for each part separately and hand write comments and explanations on the same page An automobile rental company has three locations which we will call P, Q, and R. When an automobile is rented at one of these locations, it may be returned to any of these three locations. The movement of cars from location to location each week, depending on the location from which cars are rented, is captured in the following table Location P | 60% stay at 1, Location Q | 10% go to P Location 11 | 10% go to P 10% go to Q 30% go to 11 80% stay at Q10% go to 11 20% go to Q 70% stay at 11 1. Make a directed multi-network (multigraph with weights) that describes this Markov chain. 2. Make a transition matrix P for this Markov chain 3. Suppose that initially there are 100 cars at location P, 150 cars at location Q, and 200 cars at location R. After one week (i.e. one time step not seven), how many cars do you expect will be at each location? Explain your solution in terms of matrix operations. 4. Suppose that, initially, a randomly selected car is equally likely to be at any of the three locations. (a) What is the initial probability vector po? Be careful not to round here. Rounding errors will be compounded when you compute long term behavior (b) What are the probabilities that this randomly selected car will be at each of the three locations after one week? How about after two weeks? Three weeks? As the number of weeks becomes very large? Again, you may use Mathematica 5. Repeat number, but this time assume that the initial randomly selected car has probability 0.25 of being in location P, probability 0.5 of being in location Q, and probability 0.25 of being in location R. What did you discover? 6. Find the eigenvalues and eigenvectors of P. By experimenting on the computer, notice that In converges (as n gets large) to a matrix whose columns are all identical probability vectors. This common column vector is called a steady state vector. Explain how this happens for this particular Markov chain in terms of eigenvalues and eigenvectors. In particular, explain the relationship between one particular eigenvector and this steady state vector. (See notes MC p10-11.) 7. In the context of this problem, what does the steady state vector say about the long term behavior of the Markov chain when started with any initial probability vector p

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts