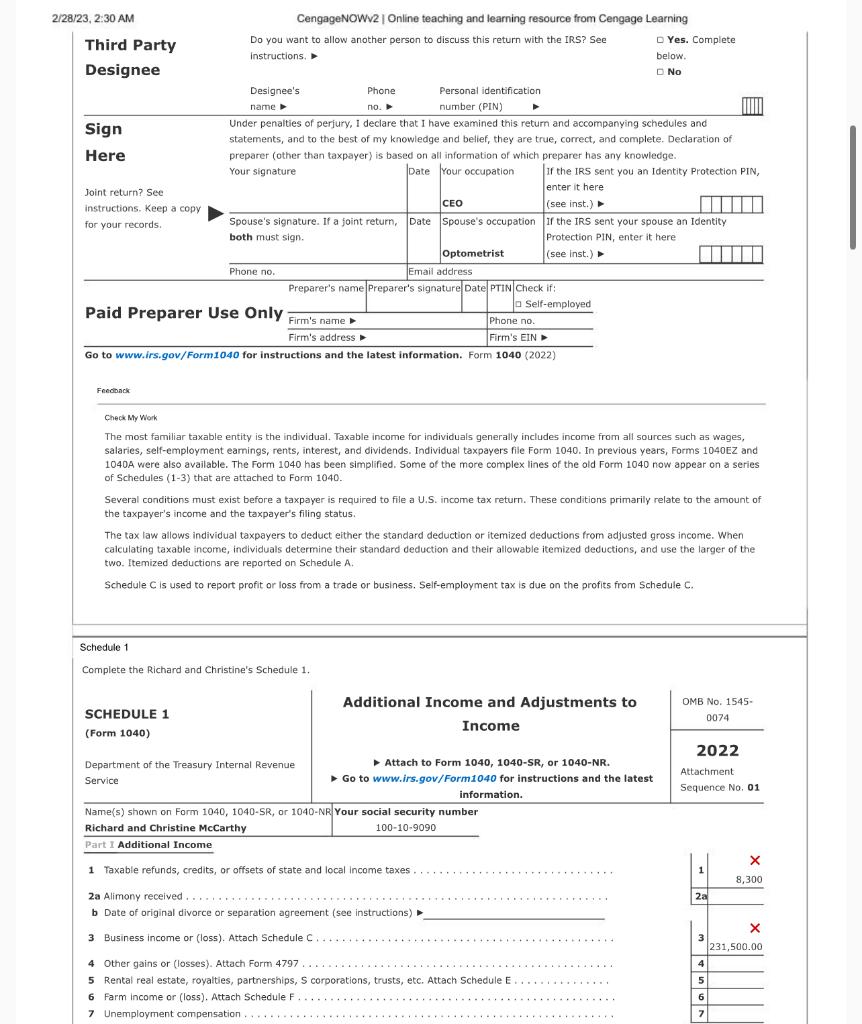

Question: Instructions Comprehensive Problem 6-1A Richard McCarthy (born 2/14/1968; Social Security number 100-10-9090) and Christine McCarthy (born 6/1/1970; Social Security number 101-213434) have a 19-year-old son

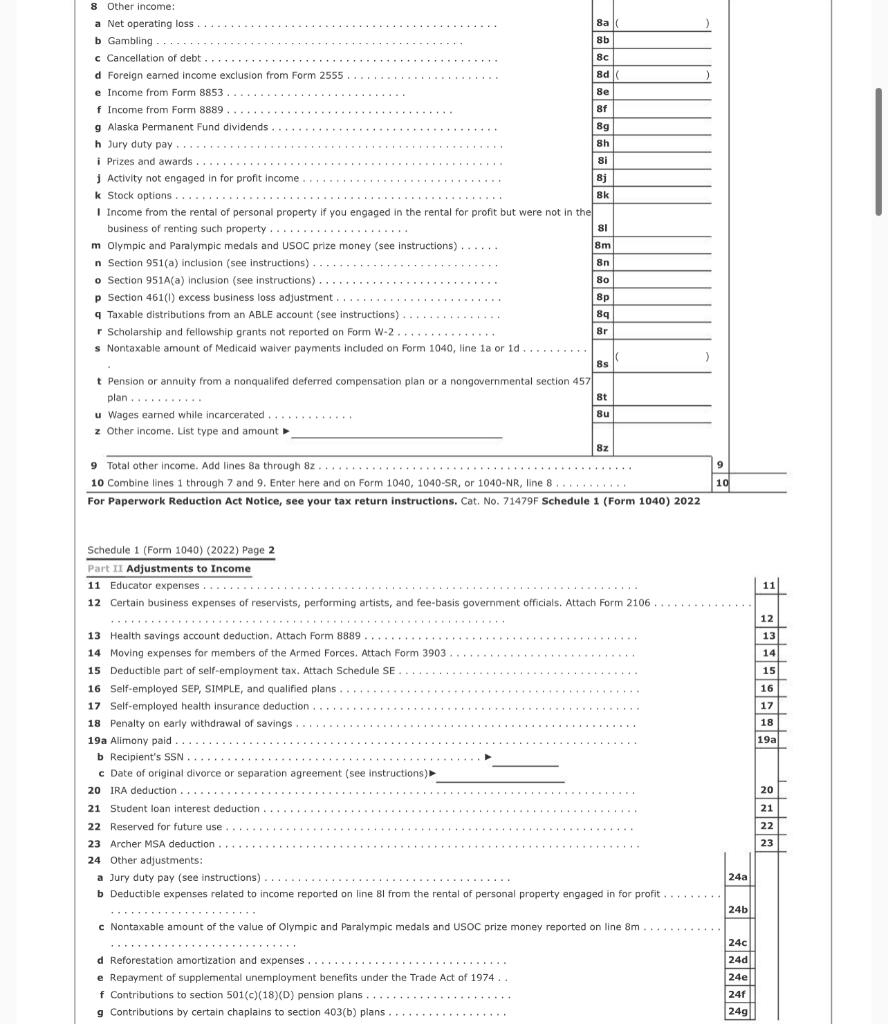

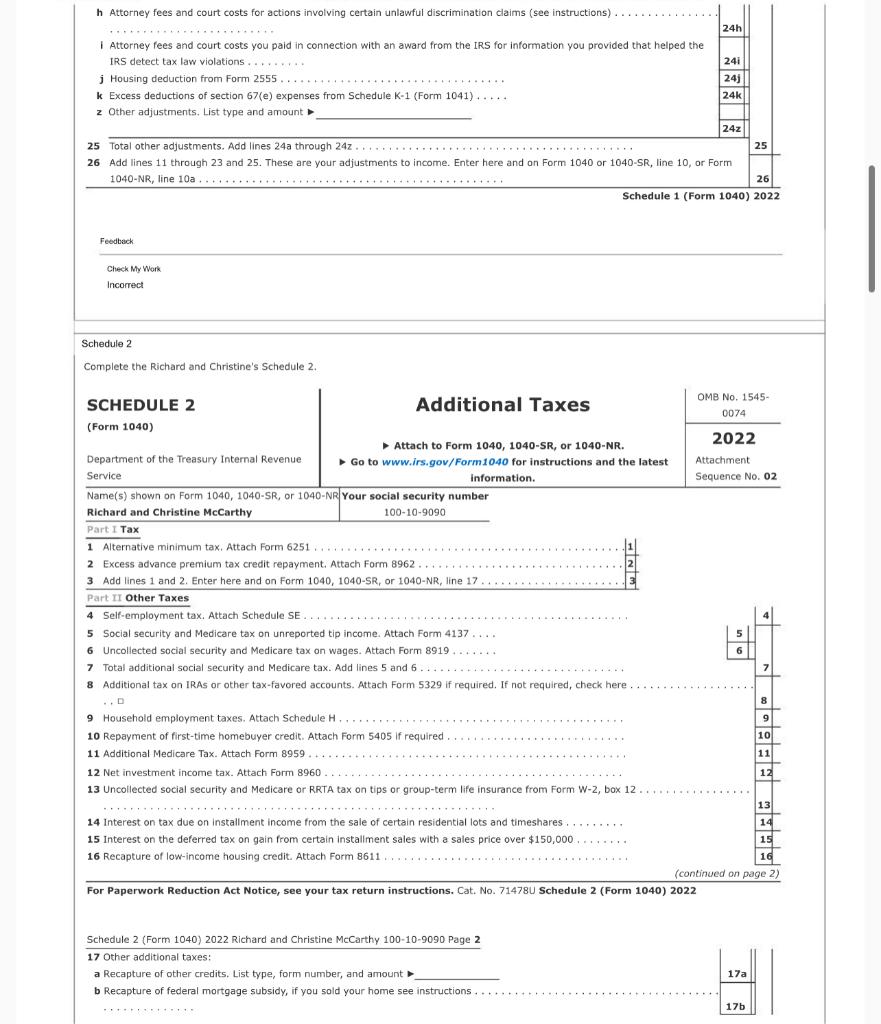

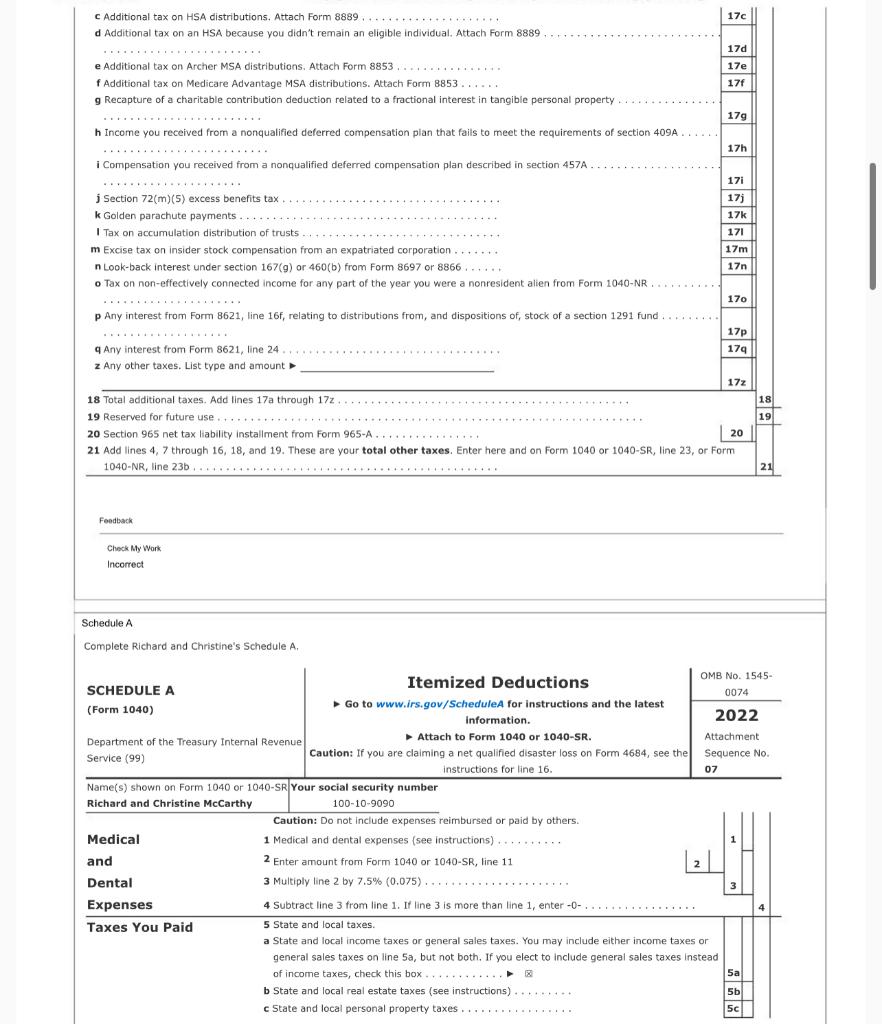

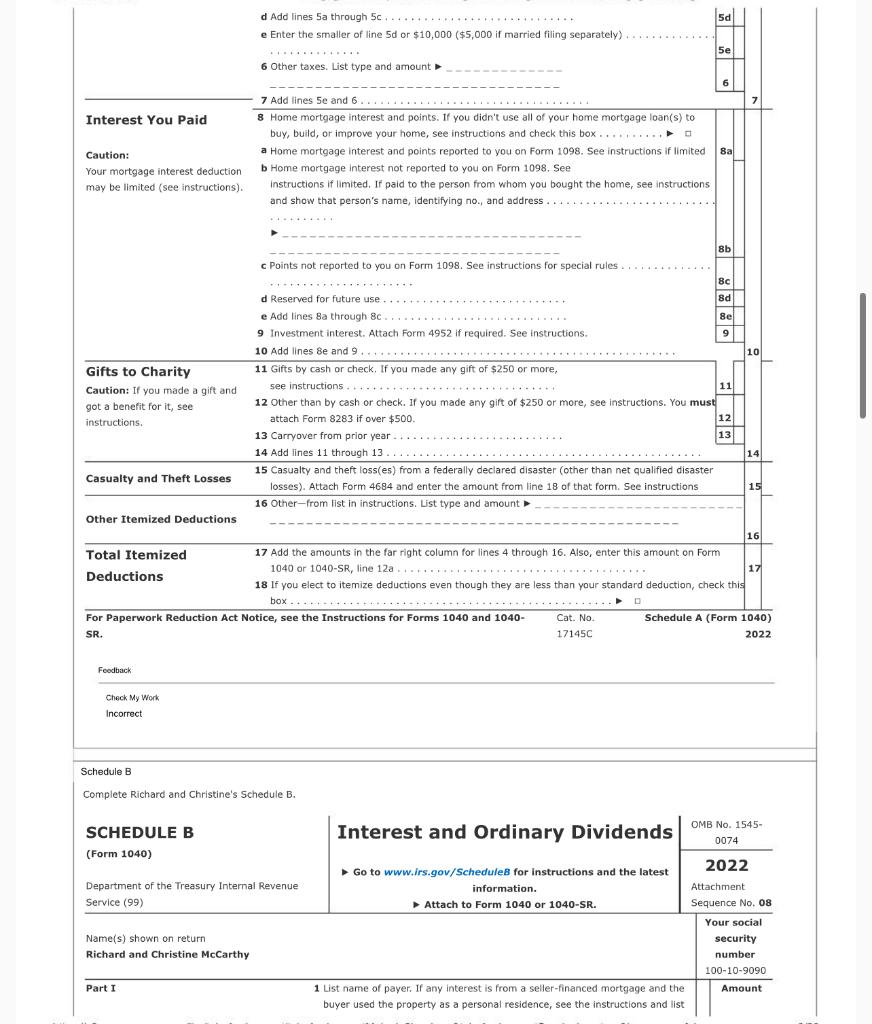

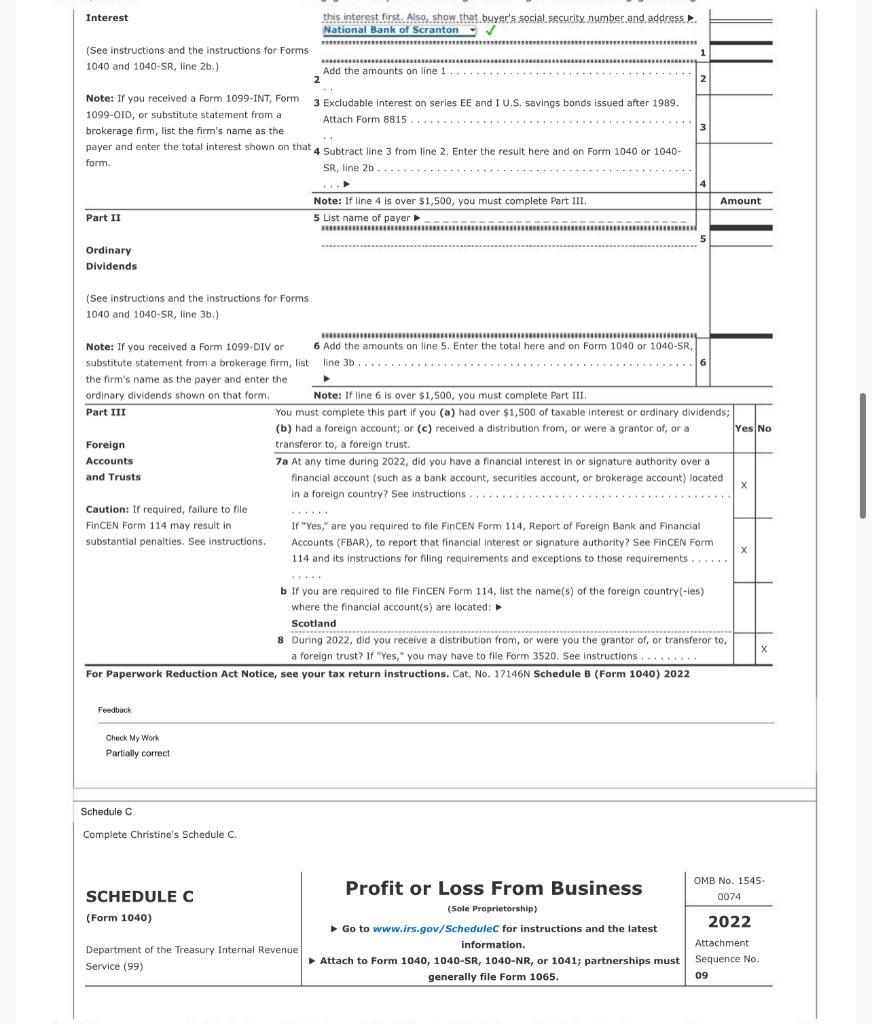

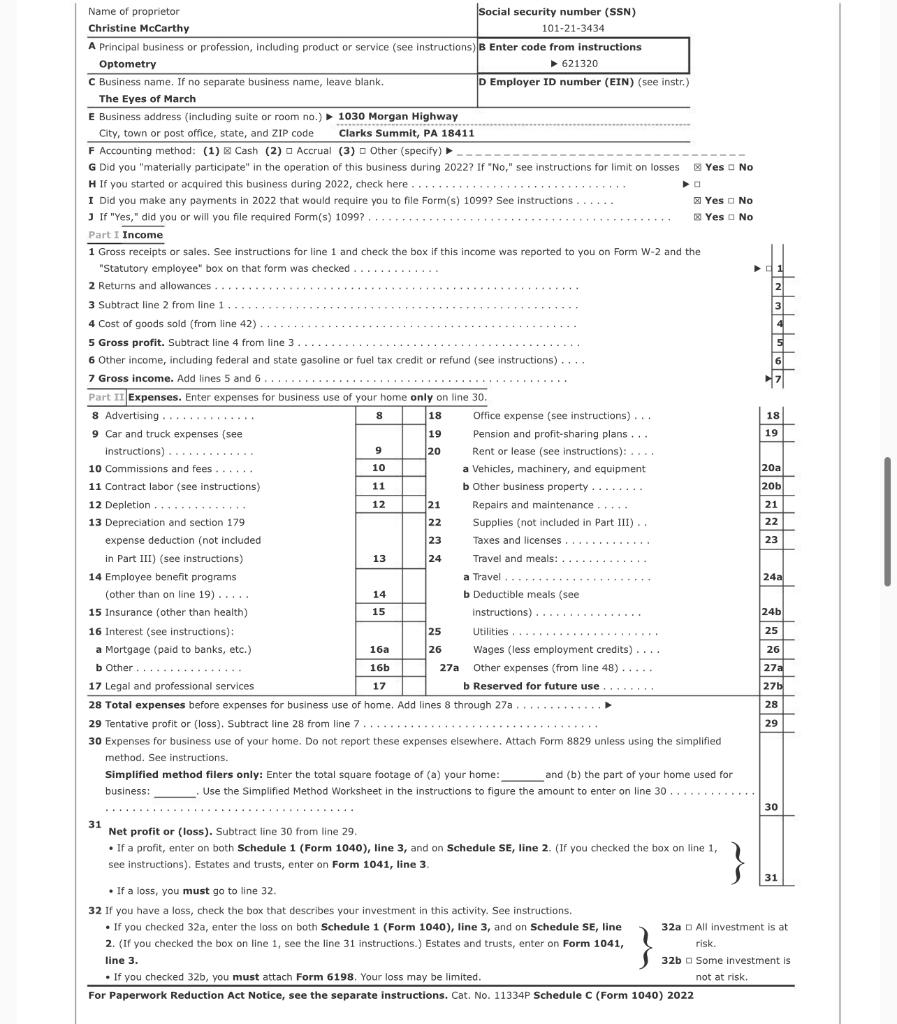

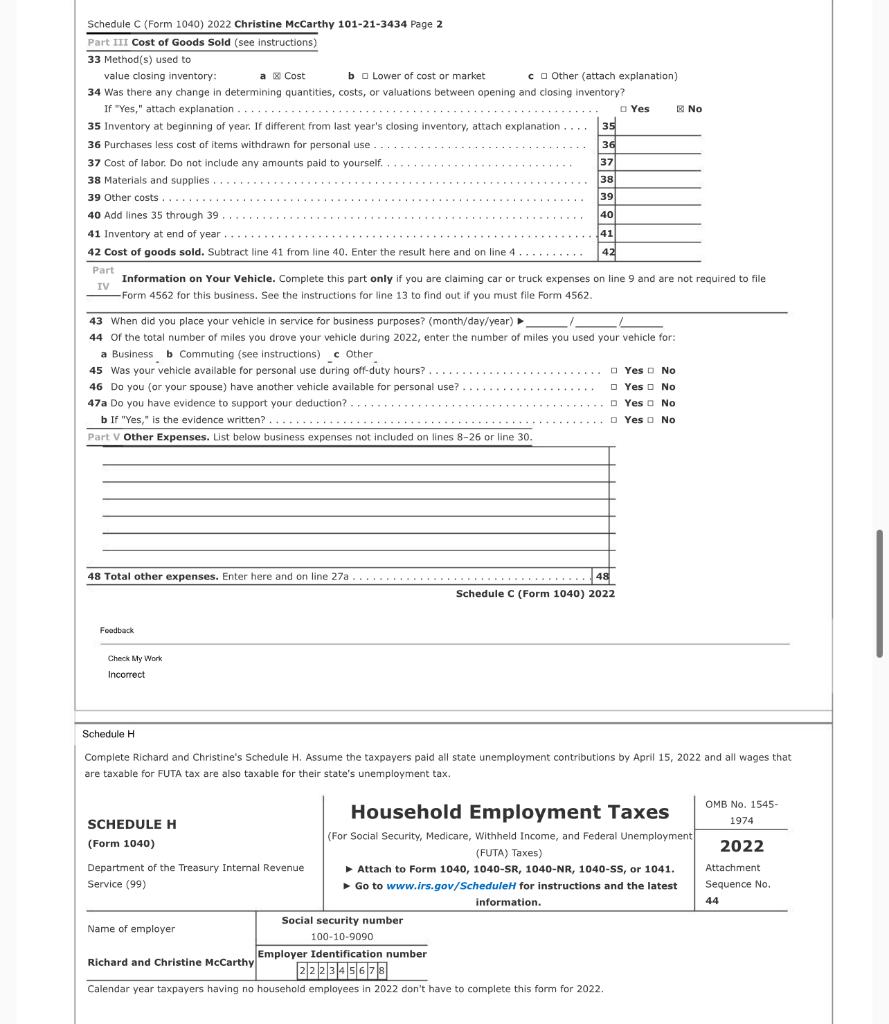

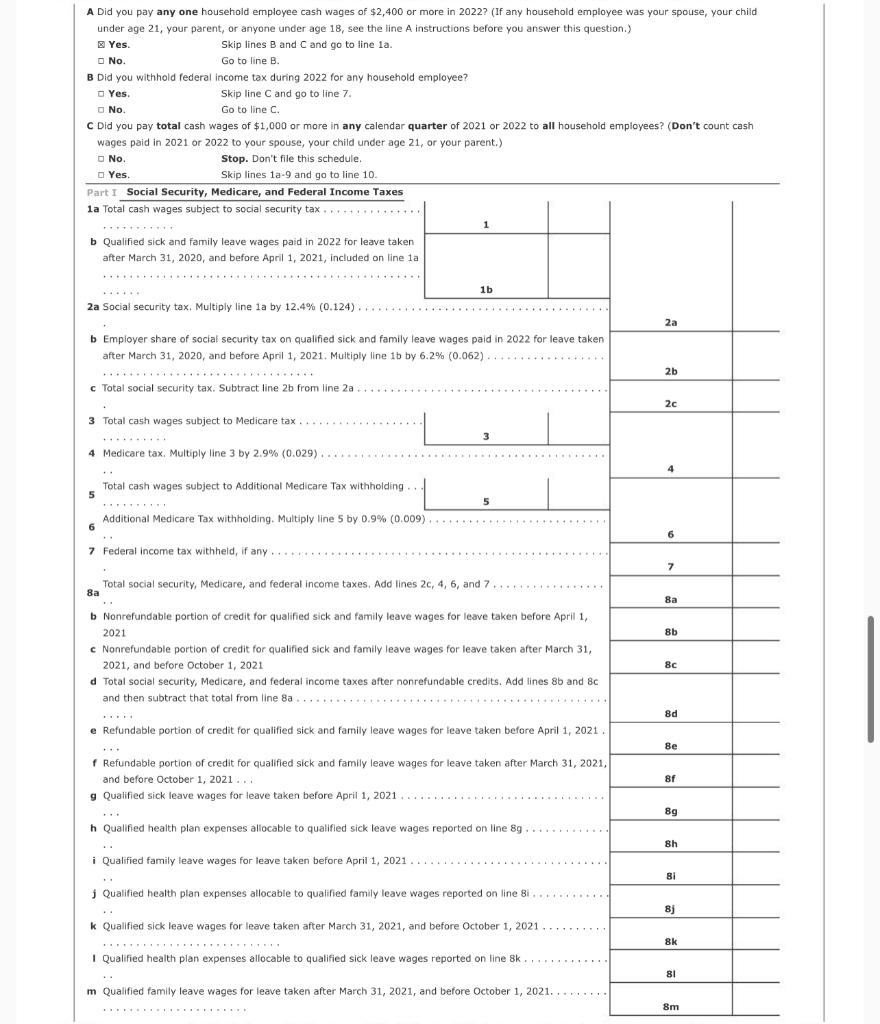

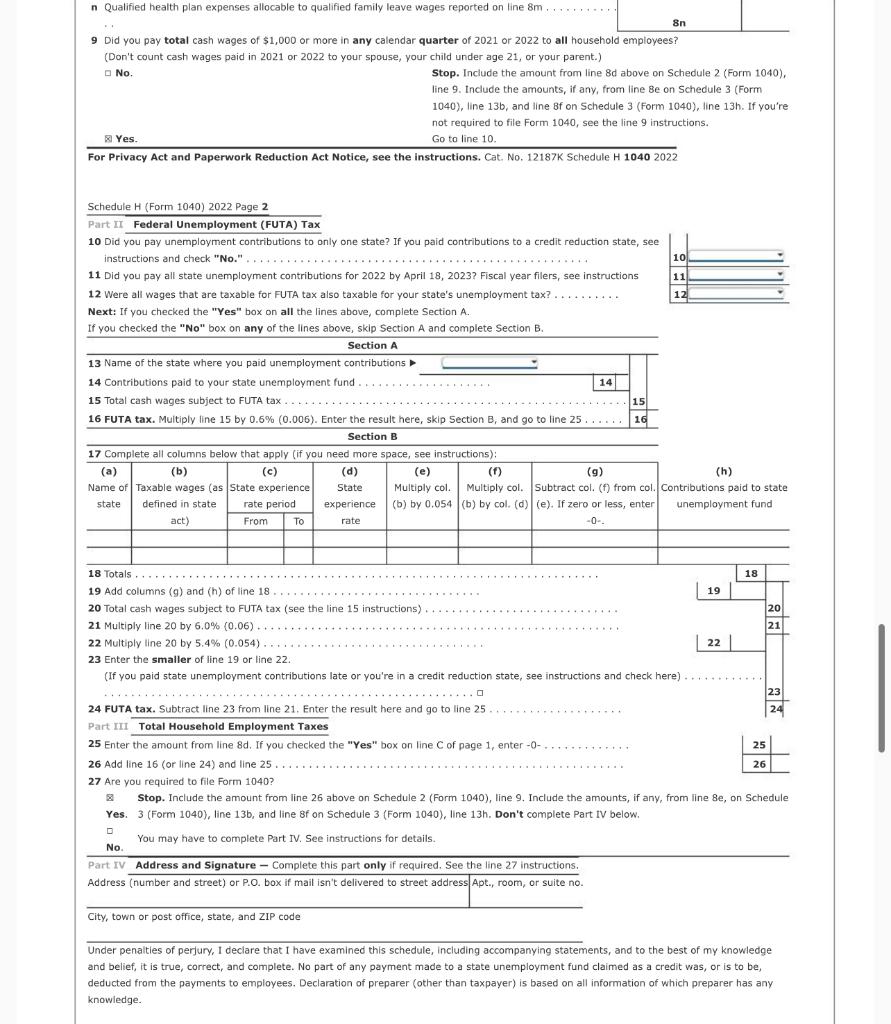

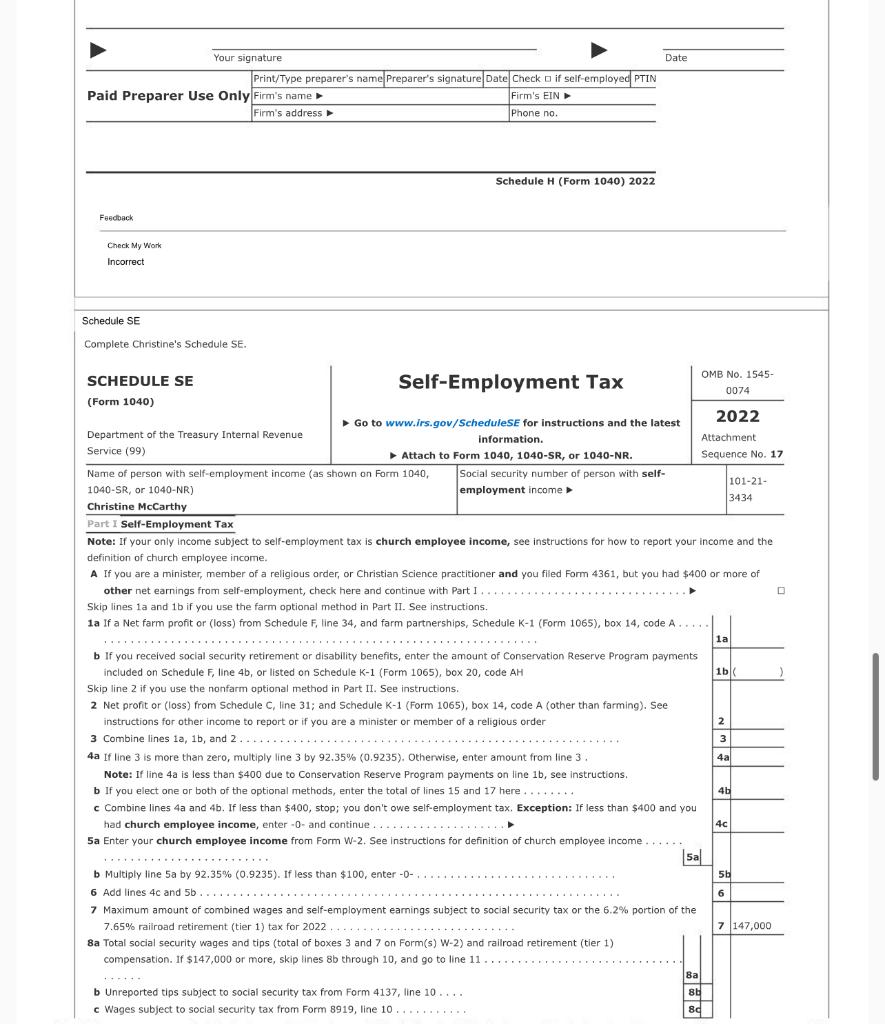

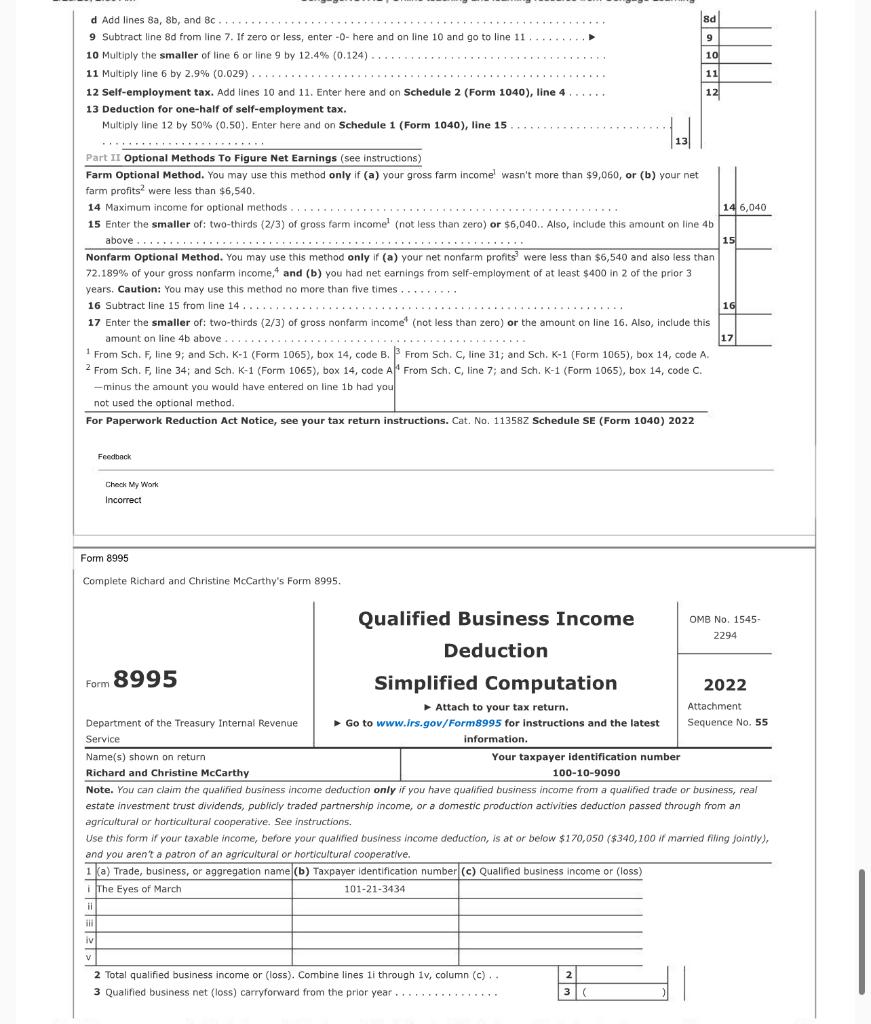

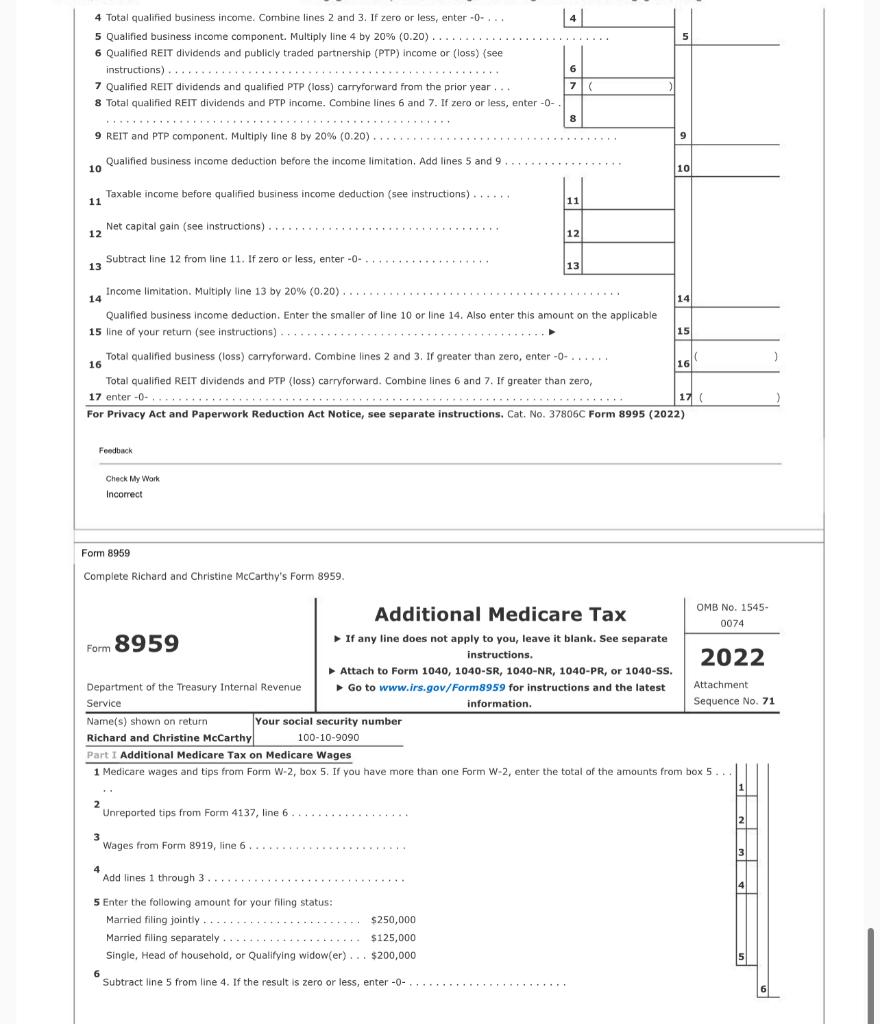

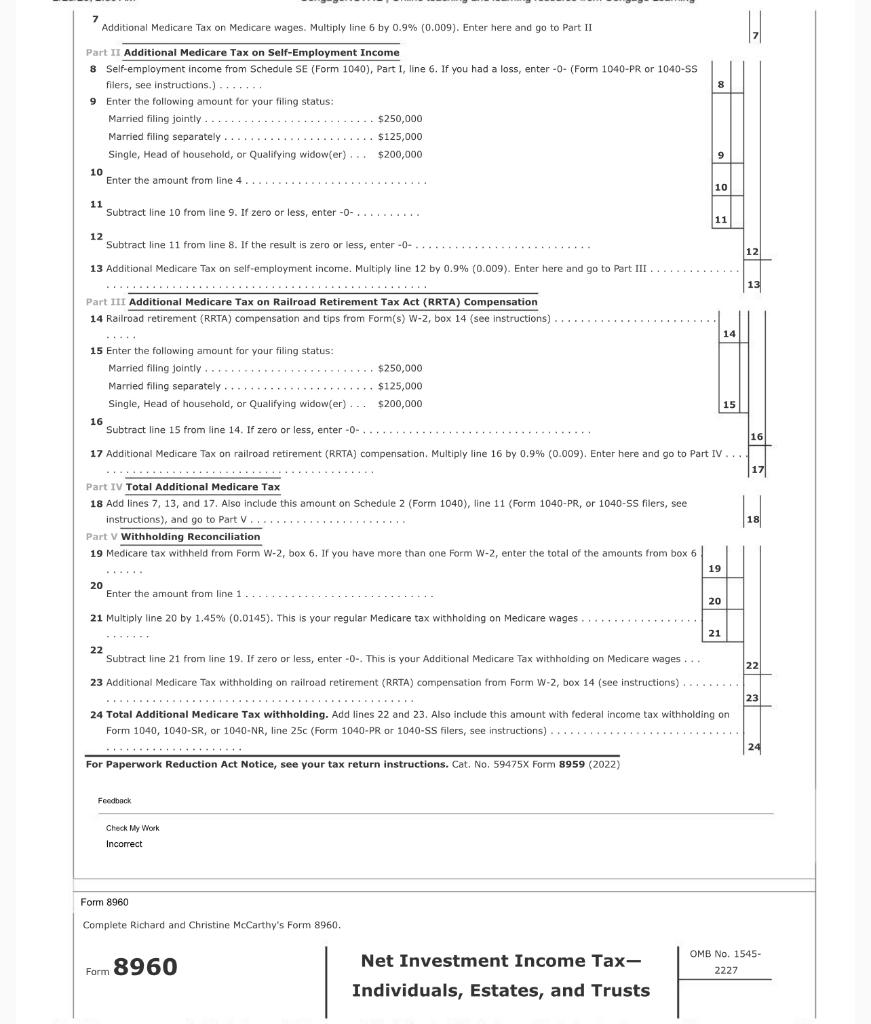

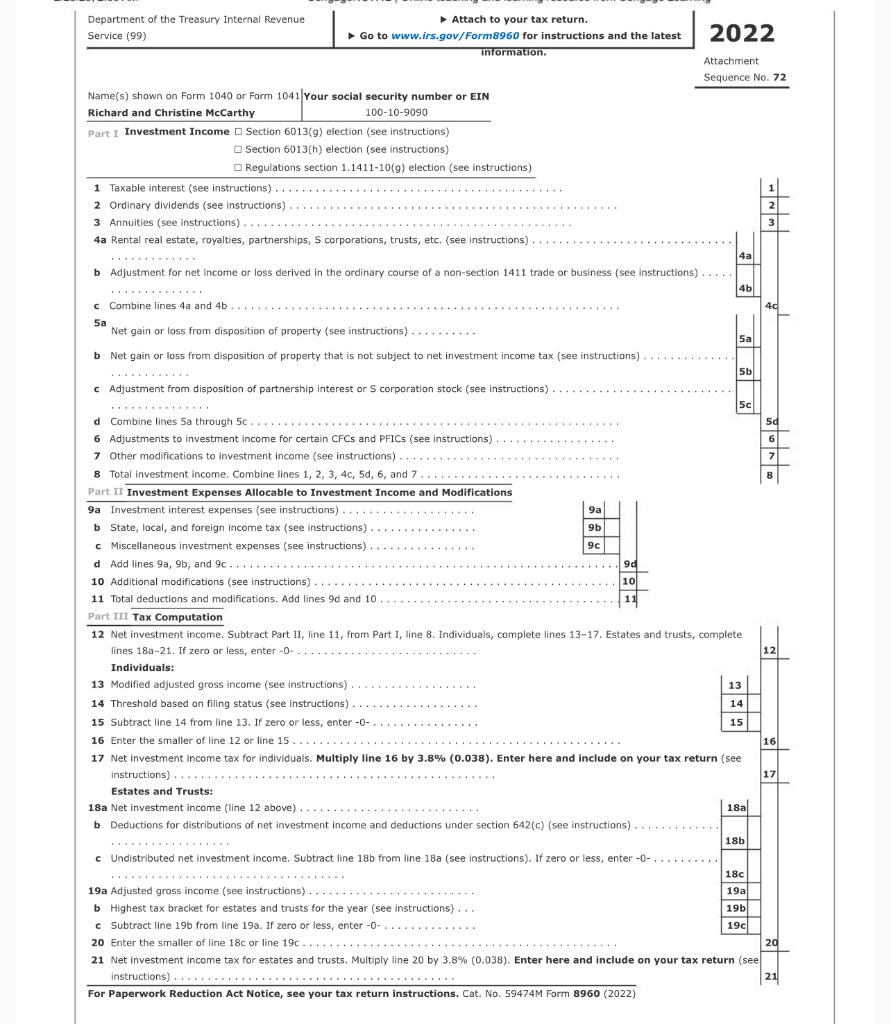

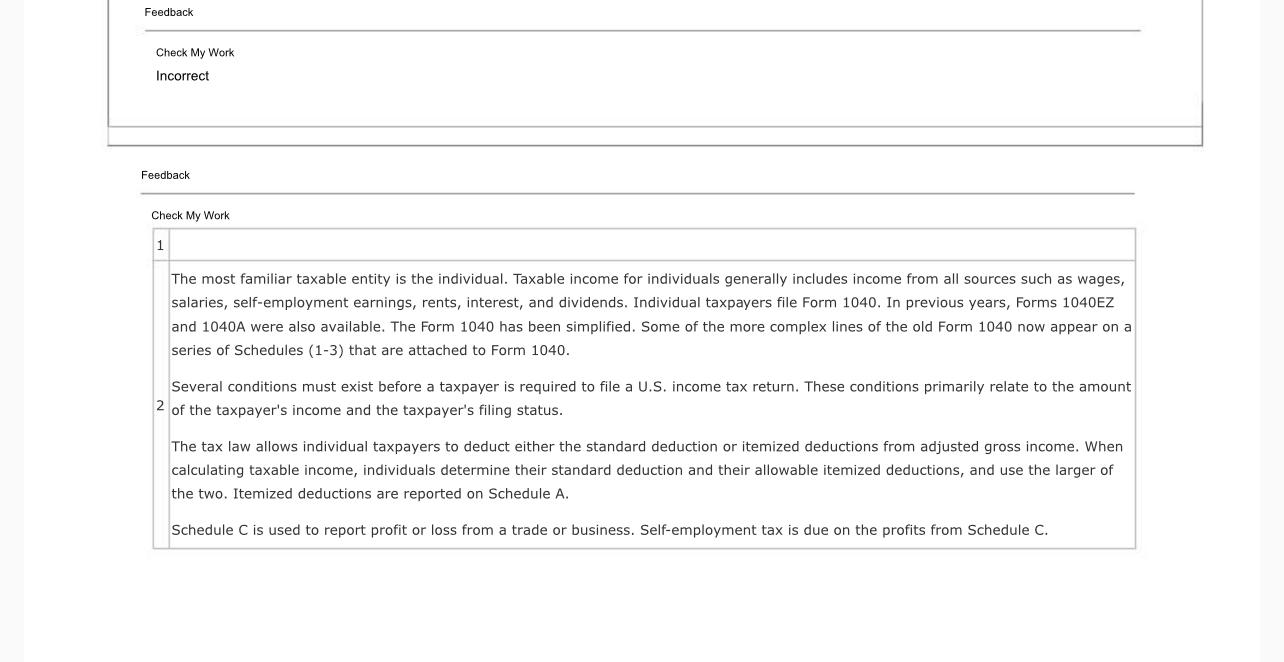

Instructions Comprehensive Problem 6-1A Richard McCarthy (born 2/14/1968; Social Security number 100-10-9090) and Christine McCarthy (born 6/1/1970; Social Security number 101-213434) have a 19-year-old son Jack, (born 10/2/2003; Social Security number 555-55-1212), who is a full-time student at the University of Key West. The McCarthys also have a 12-year-old daughter Justine, (born 12/09/2010; Social Security number 444-23-1212), who lives with them. The McCarthys can claim a $2,000 child tax credit for Justine and a $500 other dependent credit for Jack. Richard is the CEO at a paper company. His 2022 Form W-2 (see separate tab) Christine is an optometrist and operates her own practice ("The Eyes of March") in town as a sole proprietor. The shop address is 1030 Morgan Highway, Clarks Summit, PA 18411 and the business code is 621320 . Christine keeps her books on the cash basis and her bookkeeper provided the following information: Christine paid her rent in 2022 month-to-month, but paid $24,000 in December 2022 for a 12 -month lease on her office for all of 2023 . One of Christine's customers is a large state prison that purchases special eye glasses for the the inmates that meet prison safety standards. Because the order is large, Christine was paid a $20,000 advance payment in December 2022 for glasses she delivered in January 2023 . The rent and advance payment are included in her financial figures above. The McCarthys have a nanny/housekeeper whom they paid $13,000 during 2022. They did not withhold income or FICA taxes. The McCarthys paid Pennsylvania state unemployment tax of $380 in 2022. Christine received a 2022 Form 1099-INT from the National Bank of Scranton that listed interest income of $23,500. Note that McCarthys reasonably allocate $751 to state income tax expense for purposes of the net investment income tax. Christine's uncle that lives in Scotiand dies in 2022 and left her a checking account at the Royal Bank of Glasgow with a balance of 18,000 or about US\$20,000, The account did not earn any interest. Christine reported the account on the FinCEN website. The McCarthys received a Form 1099-G from Pennsylvania that reported a $477 state income tax refund from 2021 . The McCarthys filed a Schedule A in 2021 and had $14,223 of state income tax expense that was limited to a $10,000 deduction. The McCarthys paid the following in 2022: Required: Complete the McCarthys' federal tax return for 2022. Use Form 1040, Schedule 1, Schedule 2, Schedule A, Schedule B, Schedule C, Schedule H, Schedule SE, Form 8995, Form 8959, and Form 8960 to complete this tax return. Although the taxpayer is eligible for the Child or Other Dependent Tax Credit and Schedule 8812 is normally completed, we are giving you the amount to be entered directly on Form 1040. Ignore any alternative minimum tax. Do not complete Form 4952 , which is used for depreciation. - Make realistic assumptions about any missing data. - The taxpayers had health insurance coverage for the entire year and do not want to contribute to the presidential election campaign. - Enter all amounts as positive numbers. - If an amount box does not require an entry or the answer is zero, enter "0". - If required, round any dollar amount to the nearest dollar. CengageNOWv2 | Online teaching and learning resource from Cengage Learning For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Cat. No. 11320B form 1040 (2022) Form 1040 (2022) Page 2 Paid Preparer Use Onl Go to www.irs. gov/Form 1040 for instructions and the latest information. Form 1040 (2022) Fenobick Check My Work The most familiar taxable entity is the individual. Taxable income for individuals generally includes income from all sources such as wages, salaries, self-employment eamings, rents, interest, and dividends. Individual taxpayers file Form 1040 . In previous years, Forms 1040EZ and 1040A were also available. The Form 1040 has been simplified. Some of the more complex lines of the old Form 1040 now appear on a series of Schedules (1-3) that are attached to Form 1040. Several conditions must exist before a taxpayer is required to file a U.S. income tax return. These conditions primarily relate to the amount of the taxpayer's income and the taxpayer's filing status. The tax law allows individual taxpayers to deduct either the standard deduction or itemized deductions from adjusted gross income. When calculating taxable income, individuals determine their standard deduction and their allowable itemized deductions, and use the larger of the two. Itemized deductions are reported on Schedule A. Schedule C is used to report profit or loss from a trade or business. Self-employment tax is due on the profits from Schedule C. Schedule 1 Complete the Richard and Christine's Schedule 1. 8 Other income: a Net operating loss. b Gambling. c Cancellation of debt. d Foreign earned income exclusion from Form 2555 e Income from Form 8853 . f Income from Form 8889. 9 Alaska Permanent Fund dividends h Jury duty pay.... i Prizes and awards. j Activity not engaged in for profit income k Stock options.. I Income from the rental of personal property if you engaged in the rental for profit but were not in the business of renting such property.................... m Olympic and Paralympic medals and USOC prize money (see instructions) n Section 951(a) inclusion (see instructions) o Section 951A(a) inclusion (see instructions) ... ................ p Section 461(1) excess business loss adjustment q Taxable distributions from an ABLE account (see instructions) r Scholarship and fellowship grants not reported on form W-2 ............... s Nontaxable amount of Medicaid waiver payments included on Form 1040, line 1 a or 1d. t Pension or annuity from a nonqualifed deferred compensation plan or a nongovernmental section 457 plan u Wages earned while incarcerated ............ z Other income. List type and amount Schedule 1 (Form 1040) (2022) Page 2 Part II Adjustments to Income 11 Educator expenses. 12 Certain business expenses of reservists, performing artists, and fee-basis government officials. Attach Form 2106 13 Health savings account deduction. Attach Form 8889 14 Moving expenses for members of the Armed Forces. Attach Form 3903 15 Deductible part of self-employment tax. Attach Schedule SE 16 Self-employed SEP, SIMPLE, and qualified plans. 17 Self-employed health insurance deduction 18 Penalty on early withdrawal of savings. 19a Alimony paid.. b Recipient's SSN c Date of original divorce or separation agreement (see instructions) 20 IRA deduction. 21 Student loan interest deduction 22 Reserved for future use. 23 Archer MSA deduction . 24 Other adjustments: a Jury duty pay (see instructions) ............................. b Deductible expenses related to income reported on line 81 from the rental of personal property engaged in for profit. c Nontaxable amount of the value of Olympic and Paralympic medals and USOC prize money reported on line 8m. d Reforestation amortization and expenses ............................ e Repayment of supplemental unemployment benefits under the Trade Act of 1974 .. f Contributions to section 501(c)(18)(D) pension plans ................... g Contributions by certain chaplains to section 403(b) plans h Attorney fees and court costs for actions involving certain unlawful discrimination claims (see instructions). I Attorney fees and court costs you paid in connection with an award from the IRS for information you provided that helped the IRS detect tax law violations ......... j Housing deduction from Form 2555. k Excess deductions of section 67(e ) expenses from Schedule K1 (Form 1041) .... 2 Other adjustments. List type and amount 25 Total other adjustments. Add lines 24a through 24z 26 Add lines 11 through 23 and 25. These are your adjustments to income. Enter here and on Form 1040 or 1040 -SR, line 10 , or Form 1040NR, line 10a. Schedule 1 (Form 1040) 2022 Feedbeck. Check My Work Incorrect Schedule 2 Complete the Richard and Christine's Schedule 2. Schedule 2 (Form 1040) 2022 Richard and Christine McCarthy 100-10-9090 Page 2 17 Other additional taxes: a Recapture of other credits. List type, form number, and amount b Recapture of federal mortgage subsidy, if you sold your home see instructions. c Additional tax on HSA distributions, Attach Form 8889,............... d Additional tax on an HSA because you didn't remain an eligible individual. Attach form 8889 , e Additional tax on Archer MSA distributions. Attach Form 8853...... ... f Additional tax on Medicare Advantage MSA distributions. Attach Form 8853.... g Recapture of a charitable contribution deduction related to a fractional interest in tangible personal property. h Income you received from a nonqualified deferred compensation plan that fails to meet the requirements of section 409 A. j Section 72(m)(5) excess benefits tax k Golden parachute payments....... I Tax on accumulation distribution of trusts. m Excise tax on insider stock compensation from an expatriated corporation n Look-back interest under section 167(9) or 460(b) from Form 8697 or 8866.. . o Tax on non-effectively connected income for any part of the year you were a nonresident alien from Form 1040-NR. p Any interest from Form 8621, line 16f, relating to distributions from, and dispositions of, stock of a section 1291 fund q Any interest from Form 8621 , line 24 z Any other taxes. List type and amount . Feedback Check My Work Incorreet Schedule A Complete Richard and Christine's Schedule A, Schedule B Complete Richard and Christine's Schedule B. For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 17146N Schedule B (Form 1040) 2022 Feedback Check My Work Partially correct Schedule C Complete Christine's Schedule Ci. 28 Total expenses before expenses for business use of home. Add lines 8 through 27a 30 Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 unless using the simplified method. See instructions. Simplified method filers only: Enter the total square footage of (a) your home: and (b) the part of your home used for business: . Use the Simplified Method Worksheet in the instructions to figure the amount to enter on line 30........ 31 - If a profit, enter on both Schedule 1 (Form 1040), line 3, and on Schedule SE, line 2. (If you checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3. - If a loss, you must go to line 32. 32 If you have a loss, check the box that describes your investment in this activity. See instructions. - If you checked 32 a, enter the loss on both Schedule 1 (Form 1040), line 3, and on Schedule SE, line 2. (If you checked the box on line 1 , see the line 31 instructions.) Estates and trusts, enter on Form 1041, line 3. 32b a Some investment is - If you checked 32b, you must attach Form 6198. Your loss may be limited. For Paperwork Reduction Act Notice, see the separate instructions. Cat. No. 11334P Schedule C (Form 1040) 2022 Part Information on Your Vehicle. Complete this part only if you are claiming car or truck expenses on line 9 and are not required to file IV Form 4562 for this business. See the instructions for line 13 to find out if you must file Form 4562. 43 When did you place your vehicle in service for business purposes? (month/day/year) 44 Of the total number of miles you drove your vehicle during 2022 , enter the number of miles you used your vehicle for: a Business b Commuting (see instructions) c Other 45 Was your vehicle available for personal use during off-duty hours? ........................ . . . . . No 46 Do you (or your spouse) have another vehicle available for personal use? ... ....... ........ Yes No Part V Other Expenses. List below business expenses not included on lines 8-26 or line 30. Foodback Check My Work Incorrect Schedule H Complete Richard and Christine's Schedule H. Assume the taxpayers paid all state unemployment contributions by April 15,2022 and all wages that are taxable for FUTA tax are also taxable for their state's unemployment tax. A Did you pay any one household employee cash wages of $2,400 or more in 2022 ? (If any household employee was your spouse, your child binder ane 21 vhur narent ner anunne infior ano 18 coe the line inetrirtinne hofore unut ancwer thie ausetinn 1 n Qualified health plan expenses allocable to qualified family leave wages reported on line 8m 9 Did you pay total cash wages of $1,000 or more in any calendar quarter of 2021 or 2022 to all household employees? (Don't count cash wages paid in 2021 or 2022 to your spouse, your child under age 21, or your parent.) No. Stop. Include the amount from line 8d above on Schedule 2 (Form 1040), line 9. Include the amounts, if any, from line 8e on Schedule 3 (Form 1040), line 13b, and line 8f on Schedule 3 (form 1040), line 13h. If you're not required to file Form 1040 , see the line 9 instructions. Bes. Go to line 10 . Complete Richard and Christine McCarthy's Form 8995. Qualified Business Income Deduction 8995 Simplified Computation 2022 Attach to your tax return. Department of the Treasury Internal Revenue Service information. Sequence No. 55 . \begin{tabular}{l|l} \hline Name(s) shown on return & Your taxpayer identification number \\ Richard and Christine McCarthy & 100109090 \\ \hline Note. You can claim the qualified business income deduction only if you have qualified business income from a qualified trade or business, real \end{tabular} estate investment trust dividends, publicly traded partnership income, or a domestic production activities deduction passed through from an agricultural or horticultural cooperative. See instructions. Use this form if your taxable income, before your qualified business income deduction, is at or befow $170,050 ( $340,100 if married fiting jointly), and you arent a patron of an agricuitural or horticultural cooperative. 2 Total qualified business income or (loss). Combine lines ii through 1 v, column (c) ... 3 Qualified business net (loss) carryforward from the prior year . ............ \begin{tabular}{|l|l|} 2 & \\ \hline 3 & ( \\ \hline \end{tabular} Form 8959 Complete Richard and Christine McCarthy's Form 8959. 9 Enter the following amount for your filing status: Married filing jointly ........................ $250,000 Married filing separately ........................ $125,000 Single, Head of household, or Qualifying widow(er) ... $200,000 10 Enter the amount from line 4 11 Subtract line 10 from line 9. If zero or less, enter 0.. 12 Subtract line 11 from line 8 . If the result is zero or less, enter -0- 13 Additional Medicare Tax on self-employment income. Multiply line 12 by 0.9%(0.009). Enter here and go to Part III Part III Additional Medicare Tax on Railroad Retirement Tax Act (RRTA) Compensation 14 Railroad retirement (RRTA) compensation and tips from Form(s) W-2, box 14 (see instructions) 15 Enter the following amount for your filing status: Married filing jointly ....................... $250,000 Married filing separately ...................... $125,000 Single, Head of household, or Qualifying widow(er) ... $200,000 16 Subtract line 15 from line 14 . If zero or less, enter 0,,.,... 17 Additional Medicare Tax on railroad retirement (RRTA) compensation. Multiply line 16 by 0.9%(0.009), Enter here and go to Part IV... Part IV Total Additional Medicare Tax 18 Add lines 7, 13, and 17. Also include this amount on Schedule 2 (Form 1040), line 11 (Form 1040-PR, or 1040-5S filers, see instructions), and go to Part V.. Part W Withholding Reconciliation 19 Medicare tax withheld from Form W-2, box 6 , If you have more than one Form W-2, enter the total of the amounts from box 6 20 Enter the amount from line 1 . 21 Multiply line 20 by 1.45%(0.0145). This is your regular Medicare tax withholding on Medicare wages 22 22 Subtract line 21 from line 19. If zero or les5, enter -0-, This is your Additional Medicare Tax withholding on Medicare wages i. . 23 Additional Medicare Tax withholding on railroad retirement (RRTA) compensation from Form W2, box 14 (see instructions) 24 Total Additional Medicare Tax withholding. Add lines 22 and 23 . Also include this amount with federal income tax withholding on Form 1040, 1040-SR, or 1040-NR, line 25 c (Form 1040-PR or 1040-SS filers, see instructions) For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 59475X Form 8959 (2022) Feodbeck Check 1Ay Work Incorrect Form 8960 Complete Richard and Christine McCarthy's Form 8960. \begin{tabular}{c|c} Net Investment Income Tax- & OMBNo.1545-2227 \\ \cline { 2 - 3 } Individuals, Estates, and Trusts & \end{tabular} information. Attachment Sequence No. 72 Name(s) shown on Form 1040 or Form 1041 Your social security number or EIN Richard and Christine McCarthy 100109090 Part I Investment Income Section 6013(g) election (see instructions) Section 6013(h) election (see instructions) Regulations section 1.141110(g) election (see instructions) Part II Investment Expenses Allocable to Investment Income and Modifications 9a Investment interest expenses (see instructions) b State, local, and foreign income tax (see instructions) c Miscellaneous investment expenses (see instructions) d Add lines 9a,9b, and 9c 10 Additional modifications (see instructions) 11 Total deductions and modifications. Add lines 9d and 10 Part III Tax Computation 12 Net investment income. Subtract Part 11, line 11, from Part 1, line 8. Individuals, complete lines 13-17. Estates and trusts, complete lines 18a21. If zero or less, enter 0 Individuals: 13 Modified adjusted gross income (see instructions) 14 Threshold based on filing status (see instructions) 15 Subtract line 14 from line 13 . If zero or less, enter -0- 16 Enter the smaller of line 12 or line 15 17 Net investment income tax for individuals. Multiply line 16 by 3.8%(0.038). Enter here and include on your tax return (see instructions Estates and Trusts: 18a Net investment income (line 12 above) ..................... b Deductions for distributions of net investment income and deductions under section 642 (c) (see instructions) c Undistributed net investment income. Subtract line 18b from line 18b (see instructions). If zero or less, enter 0 19a Adjusted gross income (see instructions) b Highest tax bracket for estates and trusts for the year (see instructions) ... c Subtract line 19b from line 19 . If zero or less, enter 0. 20 Enter the smaller of line 18c or line 19c... 21 Net investment income tax for estates and trusts. Multiply line 20 by 3.8%(0.038). Enter here and include on your tax return (s. instructions) ................................ For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 59474M Form 8960 (2022) The most familiar taxable entity is the individual. Taxable income for individuals generally includes income from all sources such as wages, salaries, self-employment earnings, rents, interest, and dividends. Individual taxpayers file Form 1040. In previous years, Forms 1040EZ and 1040A were also available. The Form 1040 has been simplified. Some of the more complex lines of the old Form 1040 now appear on a series of Schedules (1-3) that are attached to Form 1040. Several conditions must exist before a taxpayer is required to file a U.S. income tax return. These conditions primarily relate to the amount 2 of the taxpayer's income and the taxpayer's filing status. The tax law allows individual taxpayers to deduct either the standard deduction or itemized deductions from adjusted gross income. When calculating taxable income, individuals determine their standard deduction and their allowable itemized deductions, and use the larger of the two. Itemized deductions are reported on Schedule A. Schedule C is used to report profit or loss from a trade or business. Self-employment tax is due on the profits from Schedule C. Instructions Comprehensive Problem 6-1A Richard McCarthy (born 2/14/1968; Social Security number 100-10-9090) and Christine McCarthy (born 6/1/1970; Social Security number 101-213434) have a 19-year-old son Jack, (born 10/2/2003; Social Security number 555-55-1212), who is a full-time student at the University of Key West. The McCarthys also have a 12-year-old daughter Justine, (born 12/09/2010; Social Security number 444-23-1212), who lives with them. The McCarthys can claim a $2,000 child tax credit for Justine and a $500 other dependent credit for Jack. Richard is the CEO at a paper company. His 2022 Form W-2 (see separate tab) Christine is an optometrist and operates her own practice ("The Eyes of March") in town as a sole proprietor. The shop address is 1030 Morgan Highway, Clarks Summit, PA 18411 and the business code is 621320 . Christine keeps her books on the cash basis and her bookkeeper provided the following information: Christine paid her rent in 2022 month-to-month, but paid $24,000 in December 2022 for a 12 -month lease on her office for all of 2023 . One of Christine's customers is a large state prison that purchases special eye glasses for the the inmates that meet prison safety standards. Because the order is large, Christine was paid a $20,000 advance payment in December 2022 for glasses she delivered in January 2023 . The rent and advance payment are included in her financial figures above. The McCarthys have a nanny/housekeeper whom they paid $13,000 during 2022. They did not withhold income or FICA taxes. The McCarthys paid Pennsylvania state unemployment tax of $380 in 2022. Christine received a 2022 Form 1099-INT from the National Bank of Scranton that listed interest income of $23,500. Note that McCarthys reasonably allocate $751 to state income tax expense for purposes of the net investment income tax. Christine's uncle that lives in Scotiand dies in 2022 and left her a checking account at the Royal Bank of Glasgow with a balance of 18,000 or about US\$20,000, The account did not earn any interest. Christine reported the account on the FinCEN website. The McCarthys received a Form 1099-G from Pennsylvania that reported a $477 state income tax refund from 2021 . The McCarthys filed a Schedule A in 2021 and had $14,223 of state income tax expense that was limited to a $10,000 deduction. The McCarthys paid the following in 2022: Required: Complete the McCarthys' federal tax return for 2022. Use Form 1040, Schedule 1, Schedule 2, Schedule A, Schedule B, Schedule C, Schedule H, Schedule SE, Form 8995, Form 8959, and Form 8960 to complete this tax return. Although the taxpayer is eligible for the Child or Other Dependent Tax Credit and Schedule 8812 is normally completed, we are giving you the amount to be entered directly on Form 1040. Ignore any alternative minimum tax. Do not complete Form 4952 , which is used for depreciation. - Make realistic assumptions about any missing data. - The taxpayers had health insurance coverage for the entire year and do not want to contribute to the presidential election campaign. - Enter all amounts as positive numbers. - If an amount box does not require an entry or the answer is zero, enter "0". - If required, round any dollar amount to the nearest dollar. CengageNOWv2 | Online teaching and learning resource from Cengage Learning For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Cat. No. 11320B form 1040 (2022) Form 1040 (2022) Page 2 Paid Preparer Use Onl Go to www.irs. gov/Form 1040 for instructions and the latest information. Form 1040 (2022) Fenobick Check My Work The most familiar taxable entity is the individual. Taxable income for individuals generally includes income from all sources such as wages, salaries, self-employment eamings, rents, interest, and dividends. Individual taxpayers file Form 1040 . In previous years, Forms 1040EZ and 1040A were also available. The Form 1040 has been simplified. Some of the more complex lines of the old Form 1040 now appear on a series of Schedules (1-3) that are attached to Form 1040. Several conditions must exist before a taxpayer is required to file a U.S. income tax return. These conditions primarily relate to the amount of the taxpayer's income and the taxpayer's filing status. The tax law allows individual taxpayers to deduct either the standard deduction or itemized deductions from adjusted gross income. When calculating taxable income, individuals determine their standard deduction and their allowable itemized deductions, and use the larger of the two. Itemized deductions are reported on Schedule A. Schedule C is used to report profit or loss from a trade or business. Self-employment tax is due on the profits from Schedule C. Schedule 1 Complete the Richard and Christine's Schedule 1. 8 Other income: a Net operating loss. b Gambling. c Cancellation of debt. d Foreign earned income exclusion from Form 2555 e Income from Form 8853 . f Income from Form 8889. 9 Alaska Permanent Fund dividends h Jury duty pay.... i Prizes and awards. j Activity not engaged in for profit income k Stock options.. I Income from the rental of personal property if you engaged in the rental for profit but were not in the business of renting such property.................... m Olympic and Paralympic medals and USOC prize money (see instructions) n Section 951(a) inclusion (see instructions) o Section 951A(a) inclusion (see instructions) ... ................ p Section 461(1) excess business loss adjustment q Taxable distributions from an ABLE account (see instructions) r Scholarship and fellowship grants not reported on form W-2 ............... s Nontaxable amount of Medicaid waiver payments included on Form 1040, line 1 a or 1d. t Pension or annuity from a nonqualifed deferred compensation plan or a nongovernmental section 457 plan u Wages earned while incarcerated ............ z Other income. List type and amount Schedule 1 (Form 1040) (2022) Page 2 Part II Adjustments to Income 11 Educator expenses. 12 Certain business expenses of reservists, performing artists, and fee-basis government officials. Attach Form 2106 13 Health savings account deduction. Attach Form 8889 14 Moving expenses for members of the Armed Forces. Attach Form 3903 15 Deductible part of self-employment tax. Attach Schedule SE 16 Self-employed SEP, SIMPLE, and qualified plans. 17 Self-employed health insurance deduction 18 Penalty on early withdrawal of savings. 19a Alimony paid.. b Recipient's SSN c Date of original divorce or separation agreement (see instructions) 20 IRA deduction. 21 Student loan interest deduction 22 Reserved for future use. 23 Archer MSA deduction . 24 Other adjustments: a Jury duty pay (see instructions) ............................. b Deductible expenses related to income reported on line 81 from the rental of personal property engaged in for profit. c Nontaxable amount of the value of Olympic and Paralympic medals and USOC prize money reported on line 8m. d Reforestation amortization and expenses ............................ e Repayment of supplemental unemployment benefits under the Trade Act of 1974 .. f Contributions to section 501(c)(18)(D) pension plans ................... g Contributions by certain chaplains to section 403(b) plans h Attorney fees and court costs for actions involving certain unlawful discrimination claims (see instructions). I Attorney fees and court costs you paid in connection with an award from the IRS for information you provided that helped the IRS detect tax law violations ......... j Housing deduction from Form 2555. k Excess deductions of section 67(e ) expenses from Schedule K1 (Form 1041) .... 2 Other adjustments. List type and amount 25 Total other adjustments. Add lines 24a through 24z 26 Add lines 11 through 23 and 25. These are your adjustments to income. Enter here and on Form 1040 or 1040 -SR, line 10 , or Form 1040NR, line 10a. Schedule 1 (Form 1040) 2022 Feedbeck. Check My Work Incorrect Schedule 2 Complete the Richard and Christine's Schedule 2. Schedule 2 (Form 1040) 2022 Richard and Christine McCarthy 100-10-9090 Page 2 17 Other additional taxes: a Recapture of other credits. List type, form number, and amount b Recapture of federal mortgage subsidy, if you sold your home see instructions. c Additional tax on HSA distributions, Attach Form 8889,............... d Additional tax on an HSA because you didn't remain an eligible individual. Attach form 8889 , e Additional tax on Archer MSA distributions. Attach Form 8853...... ... f Additional tax on Medicare Advantage MSA distributions. Attach Form 8853.... g Recapture of a charitable contribution deduction related to a fractional interest in tangible personal property. h Income you received from a nonqualified deferred compensation plan that fails to meet the requirements of section 409 A. j Section 72(m)(5) excess benefits tax k Golden parachute payments....... I Tax on accumulation distribution of trusts. m Excise tax on insider stock compensation from an expatriated corporation n Look-back interest under section 167(9) or 460(b) from Form 8697 or 8866.. . o Tax on non-effectively connected income for any part of the year you were a nonresident alien from Form 1040-NR. p Any interest from Form 8621, line 16f, relating to distributions from, and dispositions of, stock of a section 1291 fund q Any interest from Form 8621 , line 24 z Any other taxes. List type and amount . Feedback Check My Work Incorreet Schedule A Complete Richard and Christine's Schedule A, Schedule B Complete Richard and Christine's Schedule B. For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 17146N Schedule B (Form 1040) 2022 Feedback Check My Work Partially correct Schedule C Complete Christine's Schedule Ci. 28 Total expenses before expenses for business use of home. Add lines 8 through 27a 30 Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 unless using the simplified method. See instructions. Simplified method filers only: Enter the total square footage of (a) your home: and (b) the part of your home used for business: . Use the Simplified Method Worksheet in the instructions to figure the amount to enter on line 30........ 31 - If a profit, enter on both Schedule 1 (Form 1040), line 3, and on Schedule SE, line 2. (If you checked the box on line 1, see instructions). Estates and trusts, enter on Form 1041, line 3. - If a loss, you must go to line 32. 32 If you have a loss, check the box that describes your investment in this activity. See instructions. - If you checked 32 a, enter the loss on both Schedule 1 (Form 1040), line 3, and on Schedule SE, line 2. (If you checked the box on line 1 , see the line 31 instructions.) Estates and trusts, enter on Form 1041, line 3. 32b a Some investment is - If you checked 32b, you must attach Form 6198. Your loss may be limited. For Paperwork Reduction Act Notice, see the separate instructions. Cat. No. 11334P Schedule C (Form 1040) 2022 Part Information on Your Vehicle. Complete this part only if you are claiming car or truck expenses on line 9 and are not required to file IV Form 4562 for this business. See the instructions for line 13 to find out if you must file Form 4562. 43 When did you place your vehicle in service for business purposes? (month/day/year) 44 Of the total number of miles you drove your vehicle during 2022 , enter the number of miles you used your vehicle for: a Business b Commuting (see instructions) c Other 45 Was your vehicle available for personal use during off-duty hours? ........................ . . . . . No 46 Do you (or your spouse) have another vehicle available for personal use? ... ....... ........ Yes No Part V Other Expenses. List below business expenses not included on lines 8-26 or line 30. Foodback Check My Work Incorrect Schedule H Complete Richard and Christine's Schedule H. Assume the taxpayers paid all state unemployment contributions by April 15,2022 and all wages that are taxable for FUTA tax are also taxable for their state's unemployment tax. A Did you pay any one household employee cash wages of $2,400 or more in 2022 ? (If any household employee was your spouse, your child binder ane 21 vhur narent ner anunne infior ano 18 coe the line inetrirtinne hofore unut ancwer thie ausetinn 1 n Qualified health plan expenses allocable to qualified family leave wages reported on line 8m 9 Did you pay total cash wages of $1,000 or more in any calendar quarter of 2021 or 2022 to all household employees? (Don't count cash wages paid in 2021 or 2022 to your spouse, your child under age 21, or your parent.) No. Stop. Include the amount from line 8d above on Schedule 2 (Form 1040), line 9. Include the amounts, if any, from line 8e on Schedule 3 (Form 1040), line 13b, and line 8f on Schedule 3 (form 1040), line 13h. If you're not required to file Form 1040 , see the line 9 instructions. Bes. Go to line 10 . Complete Richard and Christine McCarthy's Form 8995. Qualified Business Income Deduction 8995 Simplified Computation 2022 Attach to your tax return. Department of the Treasury Internal Revenue Service information. Sequence No. 55 . \begin{tabular}{l|l} \hline Name(s) shown on return & Your taxpayer identification number \\ Richard and Christine McCarthy & 100109090 \\ \hline Note. You can claim the qualified business income deduction only if you have qualified business income from a qualified trade or business, real \end{tabular} estate investment trust dividends, publicly traded partnership income, or a domestic production activities deduction passed through from an agricultural or horticultural cooperative. See instructions. Use this form if your taxable income, before your qualified business income deduction, is at or befow $170,050 ( $340,100 if married fiting jointly), and you arent a patron of an agricuitural or horticultural cooperative. 2 Total qualified business income or (loss). Combine lines ii through 1 v, column (c) ... 3 Qualified business net (loss) carryforward from the prior year . ............ \begin{tabular}{|l|l|} 2 & \\ \hline 3 & ( \\ \hline \end{tabular} Form 8959 Complete Richard and Christine McCarthy's Form 8959. 9 Enter the following amount for your filing status: Married filing jointly ........................ $250,000 Married filing separately ........................ $125,000 Single, Head of household, or Qualifying widow(er) ... $200,000 10 Enter the amount from line 4 11 Subtract line 10 from line 9. If zero or less, enter 0.. 12 Subtract line 11 from line 8 . If the result is zero or less, enter -0- 13 Additional Medicare Tax on self-employment income. Multiply line 12 by 0.9%(0.009). Enter here and go to Part III Part III Additional Medicare Tax on Railroad Retirement Tax Act (RRTA) Compensation 14 Railroad retirement (RRTA) compensation and tips from Form(s) W-2, box 14 (see instructions) 15 Enter the following amount for your filing status: Married filing jointly ....................... $250,000 Married filing separately ...................... $125,000 Single, Head of household, or Qualifying widow(er) ... $200,000 16 Subtract line 15 from line 14 . If zero or less, enter 0,,.,... 17 Additional Medicare Tax on railroad retirement (RRTA) compensation. Multiply line 16 by 0.9%(0.009), Enter here and go to Part IV... Part IV Total Additional Medicare Tax 18 Add lines 7, 13, and 17. Also include this amount on Schedule 2 (Form 1040), line 11 (Form 1040-PR, or 1040-5S filers, see instructions), and go to Part V.. Part W Withholding Reconciliation 19 Medicare tax withheld from Form W-2, box 6 , If you have more than one Form W-2, enter the total of the amounts from box 6 20 Enter the amount from line 1 . 21 Multiply line 20 by 1.45%(0.0145). This is your regular Medicare tax withholding on Medicare wages 22 22 Subtract line 21 from line 19. If zero or les5, enter -0-, This is your Additional Medicare Tax withholding on Medicare wages i. . 23 Additional Medicare Tax withholding on railroad retirement (RRTA) compensation from Form W2, box 14 (see instructions) 24 Total Additional Medicare Tax withholding. Add lines 22 and 23 . Also include this amount with federal income tax withholding on Form 1040, 1040-SR, or 1040-NR, line 25 c (Form 1040-PR or 1040-SS filers, see instructions) For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 59475X Form 8959 (2022) Feodbeck Check 1Ay Work Incorrect Form 8960 Complete Richard and Christine McCarthy's Form 8960. \begin{tabular}{c|c} Net Investment Income Tax- & OMBNo.1545-2227 \\ \cline { 2 - 3 } Individuals, Estates, and Trusts & \end{tabular} information. Attachment Sequence No. 72 Name(s) shown on Form 1040 or Form 1041 Your social security number or EIN Richard and Christine McCarthy 100109090 Part I Investment Income Section 6013(g) election (see instructions) Section 6013(h) election (see instructions) Regulations section 1.141110(g) election (see instructions) Part II Investment Expenses Allocable to Investment Income and Modifications 9a Investment interest expenses (see instructions) b State, local, and foreign income tax (see instructions) c Miscellaneous investment expenses (see instructions) d Add lines 9a,9b, and 9c 10 Additional modifications (see instructions) 11 Total deductions and modifications. Add lines 9d and 10 Part III Tax Computation 12 Net investment income. Subtract Part 11, line 11, from Part 1, line 8. Individuals, complete lines 13-17. Estates and trusts, complete lines 18a21. If zero or less, enter 0 Individuals: 13 Modified adjusted gross income (see instructions) 14 Threshold based on filing status (see instructions) 15 Subtract line 14 from line 13 . If zero or less, enter -0- 16 Enter the smaller of line 12 or line 15 17 Net investment income tax for individuals. Multiply line 16 by 3.8%(0.038). Enter here and include on your tax return (see instructions Estates and Trusts: 18a Net investment income (line 12 above) ..................... b Deductions for distributions of net investment income and deductions under section 642 (c) (see instructions) c Undistributed net investment income. Subtract line 18b from line 18b (see instructions). If zero or less, enter 0 19a Adjusted gross income (see instructions) b Highest tax bracket for estates and trusts for the year (see instructions) ... c Subtract line 19b from line 19 . If zero or less, enter 0. 20 Enter the smaller of line 18c or line 19c... 21 Net investment income tax for estates and trusts. Multiply line 20 by 3.8%(0.038). Enter here and include on your tax return (s. instructions) ................................ For Paperwork Reduction Act Notice, see your tax return instructions. Cat. No. 59474M Form 8960 (2022) The most familiar taxable entity is the individual. Taxable income for individuals generally includes income from all sources such as wages, salaries, self-employment earnings, rents, interest, and dividends. Individual taxpayers file Form 1040. In previous years, Forms 1040EZ and 1040A were also available. The Form 1040 has been simplified. Some of the more complex lines of the old Form 1040 now appear on a series of Schedules (1-3) that are attached to Form 1040. Several conditions must exist before a taxpayer is required to file a U.S. income tax return. These conditions primarily relate to the amount 2 of the taxpayer's income and the taxpayer's filing status. The tax law allows individual taxpayers to deduct either the standard deduction or itemized deductions from adjusted gross income. When calculating taxable income, individuals determine their standard deduction and their allowable itemized deductions, and use the larger of the two. Itemized deductions are reported on Schedule A. Schedule C is used to report profit or loss from a trade or business. Self-employment tax is due on the profits from Schedule C

Step by Step Solution

There are 3 Steps involved in it

Completing a comprehensive tax return like this involves several steps Heres a general guide to help you navigate the McCarthys tax return Step 1 Basi... View full answer

Get step-by-step solutions from verified subject matter experts