Question: INTEGRATED CASE APPLICATION- PINNACLE MANUFACTURING: PARTV 12-37 (oajECTIVES 12-1, 12.2) In Parts I and II of this case, you performed preliminary analytical procedures and assessed

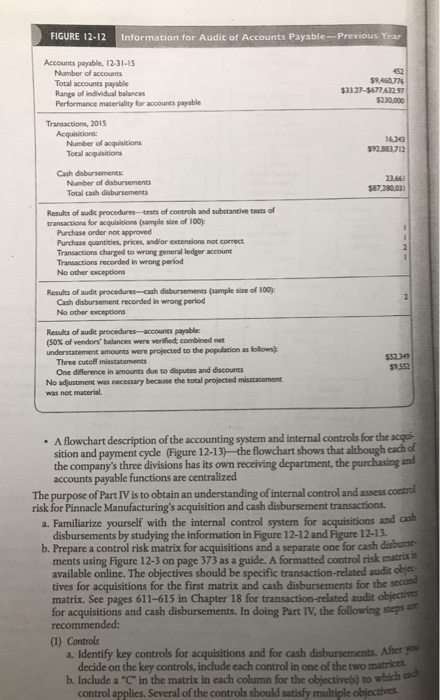

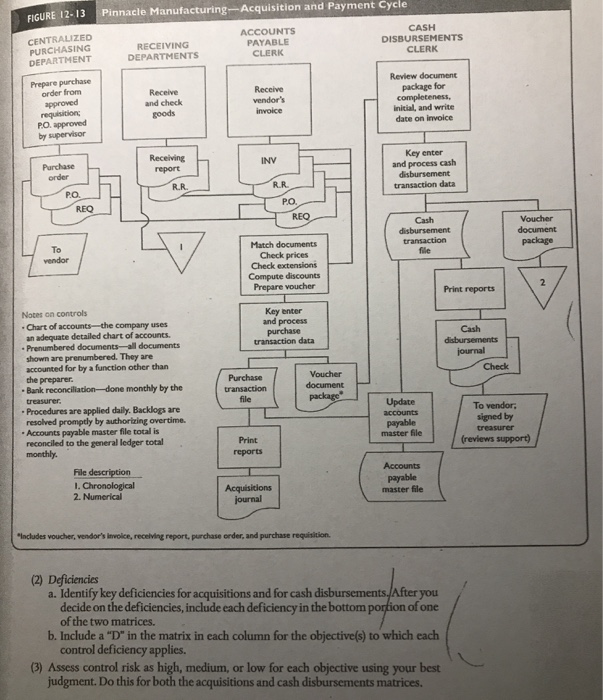

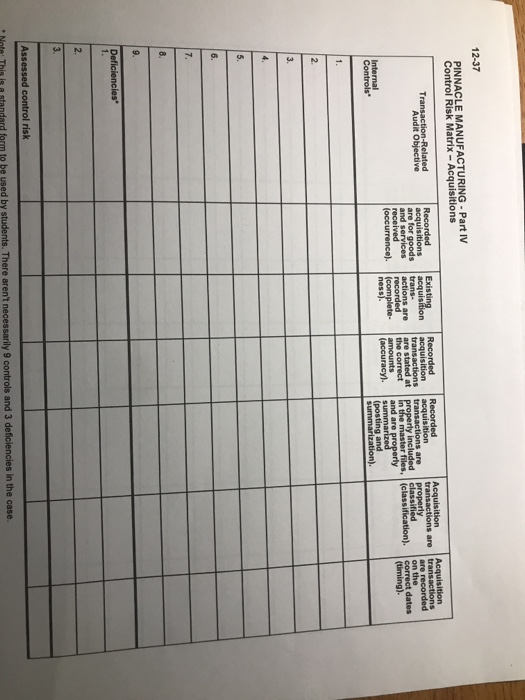

INTEGRATED CASE APPLICATION- PINNACLE MANUFACTURING: PARTV 12-37 (oajECTIVES 12-1, 12.2) In Parts I and II of this case, you performed preliminary analytical procedures and assessed acceptable audit risk and inherent risk for Pinnacle In Part III you considered fraud risks. Your team has been assigned the responsibility of auditing the acquisition and payment cycle and one related balance sheet account, accounts payable. The general approach to be taken will be to reduce assessed control risk to a low level, if possible, for the two main types of transactions affecting accounts payable: acquisitions and cash disbursements. The following are furnished as on: A summary of key information from the audit of the acquisition and payment cycle and accounts payable in the prior year, which was extracted from the previous audit firm's audit files (Figure 12-12, p.406) INTEGRATED CASE APPLICATION- PINNACLE MANUFACTURING: PARTV 12-37 (oajECTIVES 12-1, 12.2) In Parts I and II of this case, you performed preliminary analytical procedures and assessed acceptable audit risk and inherent risk for Pinnacle In Part III you considered fraud risks. Your team has been assigned the responsibility of auditing the acquisition and payment cycle and one related balance sheet account, accounts payable. The general approach to be taken will be to reduce assessed control risk to a low level, if possible, for the two main types of transactions affecting accounts payable: acquisitions and cash disbursements. The following are furnished as on: A summary of key information from the audit of the acquisition and payment cycle and accounts payable in the prior year, which was extracted from the previous audit firm's audit files (Figure 12-12, p.406)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts