Question: Introduction I n the practice set you will have the opportunity t o maintain a set o f accounting records for a typical local town

Introduction

the practice set you will have the opportunity maintain a set accounting records for a typical local town government encompassing the first two months its fiscal year. the end the second month will make the adjusting and closing entries were the end the fiscal year. will also prepare the appropriate financial statements.

The town maintains its accounting records the modified accrual basis accounting. This means that all material items revenues earned expenditures incurred are'accrued order prepare the financial statements. The accounting system used the town prescribed the State Comptroller and consists the following records:

General Journal

Cash Disbursements Journal

Cash Receipts Journal

General Ledger

Subsidiary Expenditure Ledger

Subsidiary Revenue Ledger.

Also included the practice set a chart accounts and a schedule exhibits assist recording the appropriate transactions. Balances from the previous year have been brought forward the General Ledger.

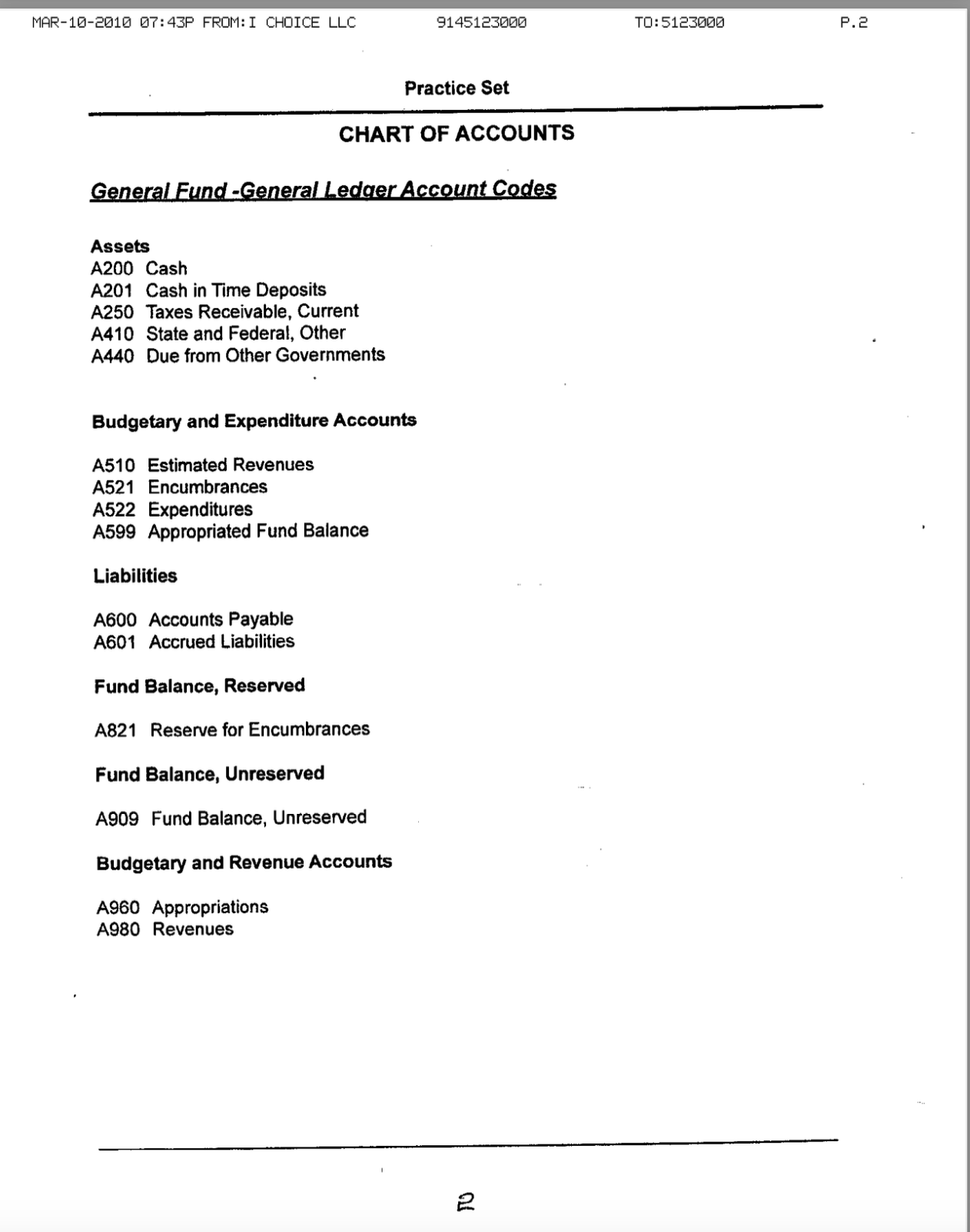

CHART ACCOUNTS

General FundGeneral Ledger Account Codes

Assets

Cash

Cash Time Deposits

Taxes Receivable, Current

State and Federal, Other

Due from Other Governments

Budgetary and Expenditure Accounts

Estimated Revenues

Encumbrances

Expenditures

Appropriated Fund Balance

Liabilities

Accounts Payable

Accrued Liabilities

Fund Balance, Reserved

Reserve for Encumbrances

Fund Balance, Unreserved

Fund Balance, Unreserved

Budgetary and Revenue Accounts

Appropriations

Revenues

General Fund Individual Revenue and Expenditure Account Codes

Revenue Account Codes

Real Property Taxes

Interest Taxes

NonProperty Tax Distribution County Tax

Clerk Fees

Youth Programs

Expenditure Account Codes

Contingent Account

PolicePersonal Services

Police Equipment and Other Capital Outlay

Police Contractual Expenditure

Parks Personal Services

Parks Equipment and Other Capital Outlay

Parks Contractual Expenditure

Practice Set Assumptions and Exhibits

The following assumptions and exhibits will used preparing the practice set.

The Town's opening balances are:

Ledgers are already posted

ExhibitA

The following budget was approved for year:

Estimated Revenues $

Real Property Taxes $

Sales Tax

State Aid

Appropriated Fund Balance $

Appropriation Subsidiaries

Exhibit.

The following payrolls were prepared and recorded during the first two months. The town

pays all employees weekly basis.

Payroll # Accounting Entries

January The budget included Exhibit journalized and posted the

appropriate ledgers.

January Real Property Tax bills are prepared and mailed amounting $

January Sales Tax Revenues $ for the quarter last year received.

January A State aid youth claim prepared and submitted for $ Moneys

are anticipated received during the town's fiscal year.

January Payroll # Exhibit paid.

January Received prior year State aid claim accrued minus $ disallowance.

January Payroll # Exhibit paid.

January Abstract # Exhibit paid.

January Tax Collector remits tax moneys the amount $

February The Police Department issues purchase order # for equipment

the amount $

February Receives State aid for youth program the amount $$

adjustment for mathematical mistake

February Tax Collector submits balance taxes $ addition $

interest.

February Payroll # Exhibit paid.

February The Police Department issues purchase order # for equipment the

amount $: there insufficient appropriations, transfer

from

February Paid Abstract # Exhibit Practice Set

February Record Payroll # Exhibit Payroll should charge percent month

February, percent should attributed March.

Adjusting Entries

Park equipment the amount $ was received but never recorded.

A State aid claim has just been submitted $ program

Prepare Closing Entries

Prepare YearEnd Financial Statements Statements Packet

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock