The main focus of this case is on the fraudulent inflating of a restructuring reserve at...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

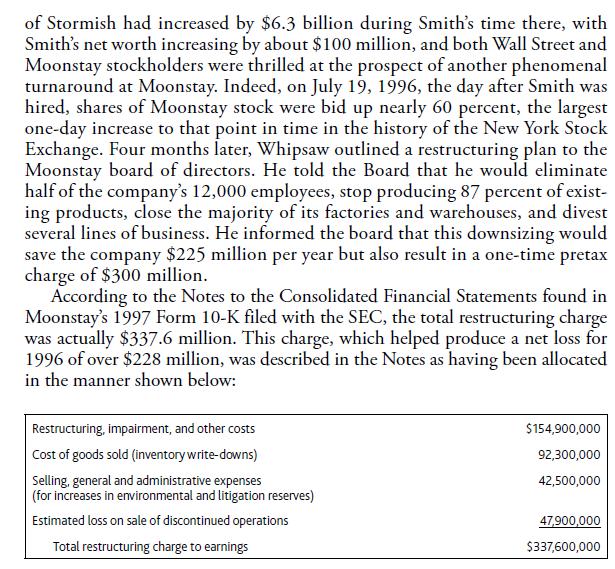

The main focus of this case is on the fraudulent inflating of a restructuring reserve at Moonstay Corporation in late 1996. This technique was actually just one of the many aspects of the massive financial reporting fraud that took place while Moonstay was being run by controversial CEO "Whipsaw" Bill Smith. The case also deals with Moonstay's unnecessary accrual of a contingent liability. You are asked to discuss the role played by Moonstay's external auditors. This case illustrates how a company can manipulate its reported income for two or more years through the use of an accounting game called restructuring reserves. The game was played at a very high level at Moonstay Corporation during 1996 and 1997, during which time CEO Whipsaw Bill Smith was Moonstay's chief executive officer (CEO). INTRODUCTION After a spectacular though brief tenure as CEO of Stormish Paper Company, which ended with the sale of Stormish to Kinter Corporation for $9.4 billion, Bill Smith, known as Whipsaw for his fondness for firing people, took some time off and then agreed to become CEO of the troubled but respected con- sumer products company, Moonstay Corporation. The market capitalization of Stormish had increased by $6.3 billion during Smith's time there, with Smith's net worth increasing by about $100 million, and both Wall Street and Moonstay stockholders were thrilled at the prospect of another phenomenal turnaround at Moonstay. Indeed, on July 19, 1996, the day after Smith was hired, shares of Moonstay stock were bid up nearly 60 percent, the largest one-day increase to that point in time in the history of the New York Stock Exchange. Four months later, Whipsaw outlined a restructuring plan to the Moonstay board of directors. He told the Board that he would eliminate half of the company's 12,000 employees, stop producing 87 percent of exist- ing products, close the majority of its factories and warehouses, and divest several lines of business. He informed the board that this downsizing would save the company $225 million per year but also result in a one-time pretax charge of $300 million. According to the Notes to the Consolidated Financial Statements found in Moonstay's 1997 Form 10-K filed with the SEC, the total restructuring charge was actually $337.6 million. This charge, which helped produce a net loss for 1996 of over $228 million, was described in the Notes as having been allocated in the manner shown below: Restructuring, Impairment, and other costs $154,900,000 Cost of goods sold (inventory write-downs) 92,300,000 Selling, general and administrative expenses (for increases in environmental and litigation reserves) 42,500,000 Estimated loss on sale of discontinued operations 47,900,000 Total restructuring charge to earnings $337,600,000 CREATING THE ILLUSION OF A TURNAROUND Ed Paul is considered one of the most successful stock investors in history, and he has written a series of letters to shareholders that are both informative and entertaining. There are usually a couple of pages devoted to accounting issues, and the 1998 letter focused on restructuring charges, which Paul described as a "distortion." He indicated that restructuring was frequently a device for manipulation. A part of costs for a number of years is typically dumped into a single quarter. The timing is designed to allow future quarters to exceed investor expectation. Sure enough, Moonstay reported successively larger profits for each quarter of 1997, culminating in earnings before discontinued operations for the year of over $123 million and a bottom line of over $109 million. This result was an apparent turnaround of over $300 million from the year before, and Wall Street responded by bidding Moonstay shares up to a high of $52 per share in March 1998. Unfortunately for many investors, creditors, and other Moonstay stakeholders, much of the miraculous turnaround was the result of creative accounting. Moonstay's chief financial officer (CFO) Robert Kurt, who also worked with Smith at Stormish, liked to remind fellow executives that he was Moonstay's "biggest profit center," and Smith stated at meetings that, "if it wasn't for Robert and the accounting team, we'd be nowhere." Things started to unravel quickly at Moonstay in early 1998, with the stock price going down fast in reaction to a series of disappointing revenue and profit reports and projections. After an article in Forbes by Matthew Toast questioned the accounting practices at Moonstay, the board of directors took the extreme action of firing both Smith and Kurt on June 13, 1998. Moonstay's external auditor, the CPA firm of CPA Pintrest, then refused to allow its unqualified opinion on the 1997 financial statements to be used in connection with any securities offerings by Moonstay. The Board and the newly appointed top management team ordered a review of the company's prior financial statements. Moonstay hired the CPA firm of CPA Capital to assist the audit committee of the board and CPA Pintrest with the review. The review led to the filing of an amended 10-K with the SEC in November 1998. Included in this 10-K/A were restated financial statements. When these are compared to the originally issued statements, it is apparent that Moonstay had purposely overstated its loss in 1996 (a big bath) and fol- lowed that with an vastly overstated net income in 1997. While much of the misstatements resulted from improper accounting for revenues and various expenses, along with the use of sham transactions, the manipulation of the restructuring reserves created by the CFO in 1996 played a significant role as well. Indeed, it seems likely that Ed Paul had Moonstay in mind when he wrote about restructurings. Meanwhile, the SEC informed Moonstay in June 1998 that its Division of Enforcement was launching an investigation. It took almost three years to complete that investigation, which resulted in the filing on May 15, 2001, of civil fraud charges against Smith, Kurt, former Moonstay controller Ron Glue, two other Moonstay officers, and the partner in charge of the CPA Pintrest audit, Phil Hart. Among the many examples of improper accounting found by the SEC was the padding of the 1996 restructuring charge with at least $35 million of improper reserves and accruals, excessive write-downs, and prematurely recognized expenses. The improper reserves were then drawn into income in each quarter of 1997, including a remarkable $21.5 million in the fourth quarter. According to the SEC, the bulk of the inflated reserves were in two areas. First, there was almost $19 million of general restructuring reserves that were clearly not in conformity with GAAP. It appears that the Enforce- ment Division deemed that this amount of reserve did not meet criterion found in Emerging Issues Task Force Issue No. 94-3 for recognition of such liabilities. Second, at least $6 million of a $12 million litigation reserve for environmental problems was recognized in violation of the FASB's Statement No. 5 on contingencies. The impact of Whipsaw Bill Smith and his friends on Moonstay Corpora- tion and its stockholders and creditors has been devastating. In February 2001, Moonstay had to file for protection from creditors under Chapter 11 of the U.S. Bankruptcy Code. The company had seen its long-term debt go from about $200 million when Smith was hired to about $2.6 billion. Positive retained earnings have been replaced by a deficit of over a billion, as mas- sive losses had been reported each year starting with 1998. At the time of the bankruptcy, the company had just $15 million in cash and its stock was selling for a mere 51 cents per share, just one percent of its peak price in 1998 of $52 per share. A LOOK AT THE DETAILS Upon completion of the review by the two CPA firms, restated financial state- ments and accompanying notes were prepared and filed with the SEC as part of Moonstay's Form 10-K/A for the fiscal year ended December 28, 1997. Among the many restatements was a $98.4 million reduction in the pre-tax amount of the total restructuring charge taken in 1996. The allocation of the restated charge, now totaling $239.2 million, is shown below. Restructuring, impairment, and other costs $110,100,000 Cost of goods sold (inventory write-downs) 60,800,000 Selling, general and administrative expenses (for outsourcing and packaging redesign) 10,100,000 Estimated loss on sale of discontinued operations 58,200,000 Total restructuring charge to earnings $239,200,000 Although greatly reduced, the first component of the restructuring charge still had a significant effect on Moonstay's financial statements. The notes ex- plained that included in this charge were both cash and non-cash items. The cash items consisted of severance and other employee costs ($24.7 million), along with the costs of closing factories and other facilities ($16.7 million). The non-cash portion of the charge ($68.7 million) related to write-downs to the net realizable value of buildings, equipment, and other assets that Moonstay planned to dispose of as part of its downsizing. When Moonstay originally recorded these charges, their accountants estimated the employee costs to be $43 million and they wrote the assets down by $91.8 million. It appears that here was some of the padding of the 1996 charge that the SEC alleges was fraudulent. However, even the reduced amounts, although deemed to be reasonable estimates as of the end of 1996, proved to be too high. The review of what actu- ally took place during 1997 led to a reversal of accruals no longer required in the amount of $14.6 million. This shows up as a positive amount in Moonstay's restated income statement for fiscal year 1997. Interestingly, no such benefit appears on the originally reported income statement. Perhaps Moonstay's ac- countants were too busy reversing some of the purposely overstated reserves and accruals in ways that would not draw attention that they missed a legitimate opportunity to increase the 1997 net income. According to both the notes and the statement of cash flows found in the original 10-K filing, Moonstay paid $43.4 million in cash during 1997 for costs associated with the 1996 restructuring plan. Included in this amount was a supposed $18.6 million for severance and other employee termination costs. However, the review by the two CPA firms only managed to find $21.2 million paid during 1997 for restructuring costs, or less than half the originally reported amount. In fact, the restated amount for severance and other employee termina- tion costs was only $10 million. So it appears that Moonstay had charged an extra $8.6 million to the restructuring reserve for payments to employees during 1997 for work done that year. Before posing a few questions to which you are to respond, shown below are some of the most important items from Moonstay's income statement and balance sheet as they were originally reported and as restated. Selected items from Moonstay Corporation=s Income Statements (Amounts in thousands, except for per share amounts) For the Year Ended December 28, 1997 For the Year Ended December 29, 1996 As As Originally Reported Originally Reported As Restated As Restated Net sales $1,168,182 $1,073,090 $984,236 $984,236 Cost of goods sold 837,683 830,956 900,573 896,938 Selling, general and administrative expense 131,056 152,653 214,029 221,655 Restructuring and asset impairment (benefit) charges (14,582) 154,869 110,122 Operating earnings (loss) 199,443 104,063 (285,235) (244,479) Loss on sale of discontinued operations, net of taxes (13,713) (14,017) (32,430) (39,140) Net earnings (loss) 109,415 38,301 (228,262) (208,481) Net earnings (loss) per share of common stock: Basic $1.29 $0.45 ($2.75) ($2.51) When it comes to the balance sheet, the restatement process did not result in dramatic changes in the December 29, 1996 Balance Sheet of Moonstay. There were some interesting changes, however, in the December 28, 1997 Balance Sheet, as shown below. Selected items from the December 28, 1997 Balance Sheet (Amounts in thousands, except for per share amounts) As Originally Reported As Restated Receivables, net $295,550 $228,460 Inventories 256,180 304,900 Total current assets 658,005 602,242 Property, plant and equipment, net 240,897 249,524 Trademarks, trade names, goodwill and other, net 221,382 207,162 Restructuring accrual 10,938 5,186 [Restructuring accrual at 12/29/96] [63,834] [51,725] Other current liabilities 80,913 118,899 Total current liabilities 198,099 233,127 Other long-term liabilities 141,109 154,300 Total shareholders' equity 531,937 472,079 Describe an alternative way to communicate the potential financial impact of a corporate restructuring that would avoid giving fraudsters the oppor- tunity to practice "creative" accounting. The main focus of this case is on the fraudulent inflating of a restructuring reserve at Moonstay Corporation in late 1996. This technique was actually just one of the many aspects of the massive financial reporting fraud that took place while Moonstay was being run by controversial CEO "Whipsaw" Bill Smith. The case also deals with Moonstay's unnecessary accrual of a contingent liability. You are asked to discuss the role played by Moonstay's external auditors. This case illustrates how a company can manipulate its reported income for two or more years through the use of an accounting game called restructuring reserves. The game was played at a very high level at Moonstay Corporation during 1996 and 1997, during which time CEO Whipsaw Bill Smith was Moonstay's chief executive officer (CEO). INTRODUCTION After a spectacular though brief tenure as CEO of Stormish Paper Company, which ended with the sale of Stormish to Kinter Corporation for $9.4 billion, Bill Smith, known as Whipsaw for his fondness for firing people, took some time off and then agreed to become CEO of the troubled but respected con- sumer products company, Moonstay Corporation. The market capitalization of Stormish had increased by $6.3 billion during Smith's time there, with Smith's net worth increasing by about $100 million, and both Wall Street and Moonstay stockholders were thrilled at the prospect of another phenomenal turnaround at Moonstay. Indeed, on July 19, 1996, the day after Smith was hired, shares of Moonstay stock were bid up nearly 60 percent, the largest one-day increase to that point in time in the history of the New York Stock Exchange. Four months later, Whipsaw outlined a restructuring plan to the Moonstay board of directors. He told the Board that he would eliminate half of the company's 12,000 employees, stop producing 87 percent of exist- ing products, close the majority of its factories and warehouses, and divest several lines of business. He informed the board that this downsizing would save the company $225 million per year but also result in a one-time pretax charge of $300 million. According to the Notes to the Consolidated Financial Statements found in Moonstay's 1997 Form 10-K filed with the SEC, the total restructuring charge was actually $337.6 million. This charge, which helped produce a net loss for 1996 of over $228 million, was described in the Notes as having been allocated in the manner shown below: Restructuring, Impairment, and other costs $154,900,000 Cost of goods sold (inventory write-downs) 92,300,000 Selling, general and administrative expenses (for increases in environmental and litigation reserves) 42,500,000 Estimated loss on sale of discontinued operations 47,900,000 Total restructuring charge to earnings $337,600,000 CREATING THE ILLUSION OF A TURNAROUND Ed Paul is considered one of the most successful stock investors in history, and he has written a series of letters to shareholders that are both informative and entertaining. There are usually a couple of pages devoted to accounting issues, and the 1998 letter focused on restructuring charges, which Paul described as a "distortion." He indicated that restructuring was frequently a device for manipulation. A part of costs for a number of years is typically dumped into a single quarter. The timing is designed to allow future quarters to exceed investor expectation. Sure enough, Moonstay reported successively larger profits for each quarter of 1997, culminating in earnings before discontinued operations for the year of over $123 million and a bottom line of over $109 million. This result was an apparent turnaround of over $300 million from the year before, and Wall Street responded by bidding Moonstay shares up to a high of $52 per share in March 1998. Unfortunately for many investors, creditors, and other Moonstay stakeholders, much of the miraculous turnaround was the result of creative accounting. Moonstay's chief financial officer (CFO) Robert Kurt, who also worked with Smith at Stormish, liked to remind fellow executives that he was Moonstay's "biggest profit center," and Smith stated at meetings that, "if it wasn't for Robert and the accounting team, we'd be nowhere." Things started to unravel quickly at Moonstay in early 1998, with the stock price going down fast in reaction to a series of disappointing revenue and profit reports and projections. After an article in Forbes by Matthew Toast questioned the accounting practices at Moonstay, the board of directors took the extreme action of firing both Smith and Kurt on June 13, 1998. Moonstay's external auditor, the CPA firm of CPA Pintrest, then refused to allow its unqualified opinion on the 1997 financial statements to be used in connection with any securities offerings by Moonstay. The Board and the newly appointed top management team ordered a review of the company's prior financial statements. Moonstay hired the CPA firm of CPA Capital to assist the audit committee of the board and CPA Pintrest with the review. The review led to the filing of an amended 10-K with the SEC in November 1998. Included in this 10-K/A were restated financial statements. When these are compared to the originally issued statements, it is apparent that Moonstay had purposely overstated its loss in 1996 (a big bath) and fol- lowed that with an vastly overstated net income in 1997. While much of the misstatements resulted from improper accounting for revenues and various expenses, along with the use of sham transactions, the manipulation of the restructuring reserves created by the CFO in 1996 played a significant role as well. Indeed, it seems likely that Ed Paul had Moonstay in mind when he wrote about restructurings. Meanwhile, the SEC informed Moonstay in June 1998 that its Division of Enforcement was launching an investigation. It took almost three years to complete that investigation, which resulted in the filing on May 15, 2001, of civil fraud charges against Smith, Kurt, former Moonstay controller Ron Glue, two other Moonstay officers, and the partner in charge of the CPA Pintrest audit, Phil Hart. Among the many examples of improper accounting found by the SEC was the padding of the 1996 restructuring charge with at least $35 million of improper reserves and accruals, excessive write-downs, and prematurely recognized expenses. The improper reserves were then drawn into income in each quarter of 1997, including a remarkable $21.5 million in the fourth quarter. According to the SEC, the bulk of the inflated reserves were in two areas. First, there was almost $19 million of general restructuring reserves that were clearly not in conformity with GAAP. It appears that the Enforce- ment Division deemed that this amount of reserve did not meet criterion found in Emerging Issues Task Force Issue No. 94-3 for recognition of such liabilities. Second, at least $6 million of a $12 million litigation reserve for environmental problems was recognized in violation of the FASB's Statement No. 5 on contingencies. The impact of Whipsaw Bill Smith and his friends on Moonstay Corpora- tion and its stockholders and creditors has been devastating. In February 2001, Moonstay had to file for protection from creditors under Chapter 11 of the U.S. Bankruptcy Code. The company had seen its long-term debt go from about $200 million when Smith was hired to about $2.6 billion. Positive retained earnings have been replaced by a deficit of over a billion, as mas- sive losses had been reported each year starting with 1998. At the time of the bankruptcy, the company had just $15 million in cash and its stock was selling for a mere 51 cents per share, just one percent of its peak price in 1998 of $52 per share. A LOOK AT THE DETAILS Upon completion of the review by the two CPA firms, restated financial state- ments and accompanying notes were prepared and filed with the SEC as part of Moonstay's Form 10-K/A for the fiscal year ended December 28, 1997. Among the many restatements was a $98.4 million reduction in the pre-tax amount of the total restructuring charge taken in 1996. The allocation of the restated charge, now totaling $239.2 million, is shown below. Restructuring, impairment, and other costs $110,100,000 Cost of goods sold (inventory write-downs) 60,800,000 Selling, general and administrative expenses (for outsourcing and packaging redesign) 10,100,000 Estimated loss on sale of discontinued operations 58,200,000 Total restructuring charge to earnings $239,200,000 Although greatly reduced, the first component of the restructuring charge still had a significant effect on Moonstay's financial statements. The notes ex- plained that included in this charge were both cash and non-cash items. The cash items consisted of severance and other employee costs ($24.7 million), along with the costs of closing factories and other facilities ($16.7 million). The non-cash portion of the charge ($68.7 million) related to write-downs to the net realizable value of buildings, equipment, and other assets that Moonstay planned to dispose of as part of its downsizing. When Moonstay originally recorded these charges, their accountants estimated the employee costs to be $43 million and they wrote the assets down by $91.8 million. It appears that here was some of the padding of the 1996 charge that the SEC alleges was fraudulent. However, even the reduced amounts, although deemed to be reasonable estimates as of the end of 1996, proved to be too high. The review of what actu- ally took place during 1997 led to a reversal of accruals no longer required in the amount of $14.6 million. This shows up as a positive amount in Moonstay's restated income statement for fiscal year 1997. Interestingly, no such benefit appears on the originally reported income statement. Perhaps Moonstay's ac- countants were too busy reversing some of the purposely overstated reserves and accruals in ways that would not draw attention that they missed a legitimate opportunity to increase the 1997 net income. According to both the notes and the statement of cash flows found in the original 10-K filing, Moonstay paid $43.4 million in cash during 1997 for costs associated with the 1996 restructuring plan. Included in this amount was a supposed $18.6 million for severance and other employee termination costs. However, the review by the two CPA firms only managed to find $21.2 million paid during 1997 for restructuring costs, or less than half the originally reported amount. In fact, the restated amount for severance and other employee termina- tion costs was only $10 million. So it appears that Moonstay had charged an extra $8.6 million to the restructuring reserve for payments to employees during 1997 for work done that year. Before posing a few questions to which you are to respond, shown below are some of the most important items from Moonstay's income statement and balance sheet as they were originally reported and as restated. Selected items from Moonstay Corporation=s Income Statements (Amounts in thousands, except for per share amounts) For the Year Ended December 28, 1997 For the Year Ended December 29, 1996 As As Originally Reported Originally Reported As Restated As Restated Net sales $1,168,182 $1,073,090 $984,236 $984,236 Cost of goods sold 837,683 830,956 900,573 896,938 Selling, general and administrative expense 131,056 152,653 214,029 221,655 Restructuring and asset impairment (benefit) charges (14,582) 154,869 110,122 Operating earnings (loss) 199,443 104,063 (285,235) (244,479) Loss on sale of discontinued operations, net of taxes (13,713) (14,017) (32,430) (39,140) Net earnings (loss) 109,415 38,301 (228,262) (208,481) Net earnings (loss) per share of common stock: Basic $1.29 $0.45 ($2.75) ($2.51) When it comes to the balance sheet, the restatement process did not result in dramatic changes in the December 29, 1996 Balance Sheet of Moonstay. There were some interesting changes, however, in the December 28, 1997 Balance Sheet, as shown below. Selected items from the December 28, 1997 Balance Sheet (Amounts in thousands, except for per share amounts) As Originally Reported As Restated Receivables, net $295,550 $228,460 Inventories 256,180 304,900 Total current assets 658,005 602,242 Property, plant and equipment, net 240,897 249,524 Trademarks, trade names, goodwill and other, net 221,382 207,162 Restructuring accrual 10,938 5,186 [Restructuring accrual at 12/29/96] [63,834] [51,725] Other current liabilities 80,913 118,899 Total current liabilities 198,099 233,127 Other long-term liabilities 141,109 154,300 Total shareholders' equity 531,937 472,079 Describe an alternative way to communicate the potential financial impact of a corporate restructuring that would avoid giving fraudsters the oppor- tunity to practice "creative" accounting. The main focus of this case is on the fraudulent inflating of a restructuring reserve at Moonstay Corporation in late 1996. This technique was actually just one of the many aspects of the massive financial reporting fraud that took place while Moonstay was being run by controversial CEO "Whipsaw" Bill Smith. The case also deals with Moonstay's unnecessary accrual of a contingent liability. You are asked to discuss the role played by Moonstay's external auditors. This case illustrates how a company can manipulate its reported income for two or more years through the use of an accounting game called restructuring reserves. The game was played at a very high level at Moonstay Corporation during 1996 and 1997, during which time CEO Whipsaw Bill Smith was Moonstay's chief executive officer (CEO). INTRODUCTION After a spectacular though brief tenure as CEO of Stormish Paper Company, which ended with the sale of Stormish to Kinter Corporation for $9.4 billion, Bill Smith, known as Whipsaw for his fondness for firing people, took some time off and then agreed to become CEO of the troubled but respected con- sumer products company, Moonstay Corporation. The market capitalization of Stormish had increased by $6.3 billion during Smith's time there, with Smith's net worth increasing by about $100 million, and both Wall Street and Moonstay stockholders were thrilled at the prospect of another phenomenal turnaround at Moonstay. Indeed, on July 19, 1996, the day after Smith was hired, shares of Moonstay stock were bid up nearly 60 percent, the largest one-day increase to that point in time in the history of the New York Stock Exchange. Four months later, Whipsaw outlined a restructuring plan to the Moonstay board of directors. He told the Board that he would eliminate half of the company's 12,000 employees, stop producing 87 percent of exist- ing products, close the majority of its factories and warehouses, and divest several lines of business. He informed the board that this downsizing would save the company $225 million per year but also result in a one-time pretax charge of $300 million. According to the Notes to the Consolidated Financial Statements found in Moonstay's 1997 Form 10-K filed with the SEC, the total restructuring charge was actually $337.6 million. This charge, which helped produce a net loss for 1996 of over $228 million, was described in the Notes as having been allocated in the manner shown below: Restructuring, Impairment, and other costs $154,900,000 Cost of goods sold (inventory write-downs) 92,300,000 Selling, general and administrative expenses (for increases in environmental and litigation reserves) 42,500,000 Estimated loss on sale of discontinued operations 47,900,000 Total restructuring charge to earnings $337,600,000 CREATING THE ILLUSION OF A TURNAROUND Ed Paul is considered one of the most successful stock investors in history, and he has written a series of letters to shareholders that are both informative and entertaining. There are usually a couple of pages devoted to accounting issues, and the 1998 letter focused on restructuring charges, which Paul described as a "distortion." He indicated that restructuring was frequently a device for manipulation. A part of costs for a number of years is typically dumped into a single quarter. The timing is designed to allow future quarters to exceed investor expectation. Sure enough, Moonstay reported successively larger profits for each quarter of 1997, culminating in earnings before discontinued operations for the year of over $123 million and a bottom line of over $109 million. This result was an apparent turnaround of over $300 million from the year before, and Wall Street responded by bidding Moonstay shares up to a high of $52 per share in March 1998. Unfortunately for many investors, creditors, and other Moonstay stakeholders, much of the miraculous turnaround was the result of creative accounting. Moonstay's chief financial officer (CFO) Robert Kurt, who also worked with Smith at Stormish, liked to remind fellow executives that he was Moonstay's "biggest profit center," and Smith stated at meetings that, "if it wasn't for Robert and the accounting team, we'd be nowhere." Things started to unravel quickly at Moonstay in early 1998, with the stock price going down fast in reaction to a series of disappointing revenue and profit reports and projections. After an article in Forbes by Matthew Toast questioned the accounting practices at Moonstay, the board of directors took the extreme action of firing both Smith and Kurt on June 13, 1998. Moonstay's external auditor, the CPA firm of CPA Pintrest, then refused to allow its unqualified opinion on the 1997 financial statements to be used in connection with any securities offerings by Moonstay. The Board and the newly appointed top management team ordered a review of the company's prior financial statements. Moonstay hired the CPA firm of CPA Capital to assist the audit committee of the board and CPA Pintrest with the review. The review led to the filing of an amended 10-K with the SEC in November 1998. Included in this 10-K/A were restated financial statements. When these are compared to the originally issued statements, it is apparent that Moonstay had purposely overstated its loss in 1996 (a big bath) and fol- lowed that with an vastly overstated net income in 1997. While much of the misstatements resulted from improper accounting for revenues and various expenses, along with the use of sham transactions, the manipulation of the restructuring reserves created by the CFO in 1996 played a significant role as well. Indeed, it seems likely that Ed Paul had Moonstay in mind when he wrote about restructurings. Meanwhile, the SEC informed Moonstay in June 1998 that its Division of Enforcement was launching an investigation. It took almost three years to complete that investigation, which resulted in the filing on May 15, 2001, of civil fraud charges against Smith, Kurt, former Moonstay controller Ron Glue, two other Moonstay officers, and the partner in charge of the CPA Pintrest audit, Phil Hart. Among the many examples of improper accounting found by the SEC was the padding of the 1996 restructuring charge with at least $35 million of improper reserves and accruals, excessive write-downs, and prematurely recognized expenses. The improper reserves were then drawn into income in each quarter of 1997, including a remarkable $21.5 million in the fourth quarter. According to the SEC, the bulk of the inflated reserves were in two areas. First, there was almost $19 million of general restructuring reserves that were clearly not in conformity with GAAP. It appears that the Enforce- ment Division deemed that this amount of reserve did not meet criterion found in Emerging Issues Task Force Issue No. 94-3 for recognition of such liabilities. Second, at least $6 million of a $12 million litigation reserve for environmental problems was recognized in violation of the FASB's Statement No. 5 on contingencies. The impact of Whipsaw Bill Smith and his friends on Moonstay Corpora- tion and its stockholders and creditors has been devastating. In February 2001, Moonstay had to file for protection from creditors under Chapter 11 of the U.S. Bankruptcy Code. The company had seen its long-term debt go from about $200 million when Smith was hired to about $2.6 billion. Positive retained earnings have been replaced by a deficit of over a billion, as mas- sive losses had been reported each year starting with 1998. At the time of the bankruptcy, the company had just $15 million in cash and its stock was selling for a mere 51 cents per share, just one percent of its peak price in 1998 of $52 per share. A LOOK AT THE DETAILS Upon completion of the review by the two CPA firms, restated financial state- ments and accompanying notes were prepared and filed with the SEC as part of Moonstay's Form 10-K/A for the fiscal year ended December 28, 1997. Among the many restatements was a $98.4 million reduction in the pre-tax amount of the total restructuring charge taken in 1996. The allocation of the restated charge, now totaling $239.2 million, is shown below. Restructuring, impairment, and other costs $110,100,000 Cost of goods sold (inventory write-downs) 60,800,000 Selling, general and administrative expenses (for outsourcing and packaging redesign) 10,100,000 Estimated loss on sale of discontinued operations 58,200,000 Total restructuring charge to earnings $239,200,000 Although greatly reduced, the first component of the restructuring charge still had a significant effect on Moonstay's financial statements. The notes ex- plained that included in this charge were both cash and non-cash items. The cash items consisted of severance and other employee costs ($24.7 million), along with the costs of closing factories and other facilities ($16.7 million). The non-cash portion of the charge ($68.7 million) related to write-downs to the net realizable value of buildings, equipment, and other assets that Moonstay planned to dispose of as part of its downsizing. When Moonstay originally recorded these charges, their accountants estimated the employee costs to be $43 million and they wrote the assets down by $91.8 million. It appears that here was some of the padding of the 1996 charge that the SEC alleges was fraudulent. However, even the reduced amounts, although deemed to be reasonable estimates as of the end of 1996, proved to be too high. The review of what actu- ally took place during 1997 led to a reversal of accruals no longer required in the amount of $14.6 million. This shows up as a positive amount in Moonstay's restated income statement for fiscal year 1997. Interestingly, no such benefit appears on the originally reported income statement. Perhaps Moonstay's ac- countants were too busy reversing some of the purposely overstated reserves and accruals in ways that would not draw attention that they missed a legitimate opportunity to increase the 1997 net income. According to both the notes and the statement of cash flows found in the original 10-K filing, Moonstay paid $43.4 million in cash during 1997 for costs associated with the 1996 restructuring plan. Included in this amount was a supposed $18.6 million for severance and other employee termination costs. However, the review by the two CPA firms only managed to find $21.2 million paid during 1997 for restructuring costs, or less than half the originally reported amount. In fact, the restated amount for severance and other employee termina- tion costs was only $10 million. So it appears that Moonstay had charged an extra $8.6 million to the restructuring reserve for payments to employees during 1997 for work done that year. Before posing a few questions to which you are to respond, shown below are some of the most important items from Moonstay's income statement and balance sheet as they were originally reported and as restated. Selected items from Moonstay Corporation=s Income Statements (Amounts in thousands, except for per share amounts) For the Year Ended December 28, 1997 For the Year Ended December 29, 1996 As As Originally Reported Originally Reported As Restated As Restated Net sales $1,168,182 $1,073,090 $984,236 $984,236 Cost of goods sold 837,683 830,956 900,573 896,938 Selling, general and administrative expense 131,056 152,653 214,029 221,655 Restructuring and asset impairment (benefit) charges (14,582) 154,869 110,122 Operating earnings (loss) 199,443 104,063 (285,235) (244,479) Loss on sale of discontinued operations, net of taxes (13,713) (14,017) (32,430) (39,140) Net earnings (loss) 109,415 38,301 (228,262) (208,481) Net earnings (loss) per share of common stock: Basic $1.29 $0.45 ($2.75) ($2.51) When it comes to the balance sheet, the restatement process did not result in dramatic changes in the December 29, 1996 Balance Sheet of Moonstay. There were some interesting changes, however, in the December 28, 1997 Balance Sheet, as shown below. Selected items from the December 28, 1997 Balance Sheet (Amounts in thousands, except for per share amounts) As Originally Reported As Restated Receivables, net $295,550 $228,460 Inventories 256,180 304,900 Total current assets 658,005 602,242 Property, plant and equipment, net 240,897 249,524 Trademarks, trade names, goodwill and other, net 221,382 207,162 Restructuring accrual 10,938 5,186 [Restructuring accrual at 12/29/96] [63,834] [51,725] Other current liabilities 80,913 118,899 Total current liabilities 198,099 233,127 Other long-term liabilities 141,109 154,300 Total shareholders' equity 531,937 472,079 Describe an alternative way to communicate the potential financial impact of a corporate restructuring that would avoid giving fraudsters the oppor- tunity to practice "creative" accounting. The main focus of this case is on the fraudulent inflating of a restructuring reserve at Moonstay Corporation in late 1996. This technique was actually just one of the many aspects of the massive financial reporting fraud that took place while Moonstay was being run by controversial CEO "Whipsaw" Bill Smith. The case also deals with Moonstay's unnecessary accrual of a contingent liability. You are asked to discuss the role played by Moonstay's external auditors. This case illustrates how a company can manipulate its reported income for two or more years through the use of an accounting game called restructuring reserves. The game was played at a very high level at Moonstay Corporation during 1996 and 1997, during which time CEO Whipsaw Bill Smith was Moonstay's chief executive officer (CEO). INTRODUCTION After a spectacular though brief tenure as CEO of Stormish Paper Company, which ended with the sale of Stormish to Kinter Corporation for $9.4 billion, Bill Smith, known as Whipsaw for his fondness for firing people, took some time off and then agreed to become CEO of the troubled but respected con- sumer products company, Moonstay Corporation. The market capitalization of Stormish had increased by $6.3 billion during Smith's time there, with Smith's net worth increasing by about $100 million, and both Wall Street and Moonstay stockholders were thrilled at the prospect of another phenomenal turnaround at Moonstay. Indeed, on July 19, 1996, the day after Smith was hired, shares of Moonstay stock were bid up nearly 60 percent, the largest one-day increase to that point in time in the history of the New York Stock Exchange. Four months later, Whipsaw outlined a restructuring plan to the Moonstay board of directors. He told the Board that he would eliminate half of the company's 12,000 employees, stop producing 87 percent of exist- ing products, close the majority of its factories and warehouses, and divest several lines of business. He informed the board that this downsizing would save the company $225 million per year but also result in a one-time pretax charge of $300 million. According to the Notes to the Consolidated Financial Statements found in Moonstay's 1997 Form 10-K filed with the SEC, the total restructuring charge was actually $337.6 million. This charge, which helped produce a net loss for 1996 of over $228 million, was described in the Notes as having been allocated in the manner shown below: Restructuring, Impairment, and other costs $154,900,000 Cost of goods sold (inventory write-downs) 92,300,000 Selling, general and administrative expenses (for increases in environmental and litigation reserves) 42,500,000 Estimated loss on sale of discontinued operations 47,900,000 Total restructuring charge to earnings $337,600,000 CREATING THE ILLUSION OF A TURNAROUND Ed Paul is considered one of the most successful stock investors in history, and he has written a series of letters to shareholders that are both informative and entertaining. There are usually a couple of pages devoted to accounting issues, and the 1998 letter focused on restructuring charges, which Paul described as a "distortion." He indicated that restructuring was frequently a device for manipulation. A part of costs for a number of years is typically dumped into a single quarter. The timing is designed to allow future quarters to exceed investor expectation. Sure enough, Moonstay reported successively larger profits for each quarter of 1997, culminating in earnings before discontinued operations for the year of over $123 million and a bottom line of over $109 million. This result was an apparent turnaround of over $300 million from the year before, and Wall Street responded by bidding Moonstay shares up to a high of $52 per share in March 1998. Unfortunately for many investors, creditors, and other Moonstay stakeholders, much of the miraculous turnaround was the result of creative accounting. Moonstay's chief financial officer (CFO) Robert Kurt, who also worked with Smith at Stormish, liked to remind fellow executives that he was Moonstay's "biggest profit center," and Smith stated at meetings that, "if it wasn't for Robert and the accounting team, we'd be nowhere." Things started to unravel quickly at Moonstay in early 1998, with the stock price going down fast in reaction to a series of disappointing revenue and profit reports and projections. After an article in Forbes by Matthew Toast questioned the accounting practices at Moonstay, the board of directors took the extreme action of firing both Smith and Kurt on June 13, 1998. Moonstay's external auditor, the CPA firm of CPA Pintrest, then refused to allow its unqualified opinion on the 1997 financial statements to be used in connection with any securities offerings by Moonstay. The Board and the newly appointed top management team ordered a review of the company's prior financial statements. Moonstay hired the CPA firm of CPA Capital to assist the audit committee of the board and CPA Pintrest with the review. The review led to the filing of an amended 10-K with the SEC in November 1998. Included in this 10-K/A were restated financial statements. When these are compared to the originally issued statements, it is apparent that Moonstay had purposely overstated its loss in 1996 (a big bath) and fol- lowed that with an vastly overstated net income in 1997. While much of the misstatements resulted from improper accounting for revenues and various expenses, along with the use of sham transactions, the manipulation of the restructuring reserves created by the CFO in 1996 played a significant role as well. Indeed, it seems likely that Ed Paul had Moonstay in mind when he wrote about restructurings. Meanwhile, the SEC informed Moonstay in June 1998 that its Division of Enforcement was launching an investigation. It took almost three years to complete that investigation, which resulted in the filing on May 15, 2001, of civil fraud charges against Smith, Kurt, former Moonstay controller Ron Glue, two other Moonstay officers, and the partner in charge of the CPA Pintrest audit, Phil Hart. Among the many examples of improper accounting found by the SEC was the padding of the 1996 restructuring charge with at least $35 million of improper reserves and accruals, excessive write-downs, and prematurely recognized expenses. The improper reserves were then drawn into income in each quarter of 1997, including a remarkable $21.5 million in the fourth quarter. According to the SEC, the bulk of the inflated reserves were in two areas. First, there was almost $19 million of general restructuring reserves that were clearly not in conformity with GAAP. It appears that the Enforce- ment Division deemed that this amount of reserve did not meet criterion found in Emerging Issues Task Force Issue No. 94-3 for recognition of such liabilities. Second, at least $6 million of a $12 million litigation reserve for environmental problems was recognized in violation of the FASB's Statement No. 5 on contingencies. The impact of Whipsaw Bill Smith and his friends on Moonstay Corpora- tion and its stockholders and creditors has been devastating. In February 2001, Moonstay had to file for protection from creditors under Chapter 11 of the U.S. Bankruptcy Code. The company had seen its long-term debt go from about $200 million when Smith was hired to about $2.6 billion. Positive retained earnings have been replaced by a deficit of over a billion, as mas- sive losses had been reported each year starting with 1998. At the time of the bankruptcy, the company had just $15 million in cash and its stock was selling for a mere 51 cents per share, just one percent of its peak price in 1998 of $52 per share. A LOOK AT THE DETAILS Upon completion of the review by the two CPA firms, restated financial state- ments and accompanying notes were prepared and filed with the SEC as part of Moonstay's Form 10-K/A for the fiscal year ended December 28, 1997. Among the many restatements was a $98.4 million reduction in the pre-tax amount of the total restructuring charge taken in 1996. The allocation of the restated charge, now totaling $239.2 million, is shown below. Restructuring, impairment, and other costs $110,100,000 Cost of goods sold (inventory write-downs) 60,800,000 Selling, general and administrative expenses (for outsourcing and packaging redesign) 10,100,000 Estimated loss on sale of discontinued operations 58,200,000 Total restructuring charge to earnings $239,200,000 Although greatly reduced, the first component of the restructuring charge still had a significant effect on Moonstay's financial statements. The notes ex- plained that included in this charge were both cash and non-cash items. The cash items consisted of severance and other employee costs ($24.7 million), along with the costs of closing factories and other facilities ($16.7 million). The non-cash portion of the charge ($68.7 million) related to write-downs to the net realizable value of buildings, equipment, and other assets that Moonstay planned to dispose of as part of its downsizing. When Moonstay originally recorded these charges, their accountants estimated the employee costs to be $43 million and they wrote the assets down by $91.8 million. It appears that here was some of the padding of the 1996 charge that the SEC alleges was fraudulent. However, even the reduced amounts, although deemed to be reasonable estimates as of the end of 1996, proved to be too high. The review of what actu- ally took place during 1997 led to a reversal of accruals no longer required in the amount of $14.6 million. This shows up as a positive amount in Moonstay's restated income statement for fiscal year 1997. Interestingly, no such benefit appears on the originally reported income statement. Perhaps Moonstay's ac- countants were too busy reversing some of the purposely overstated reserves and accruals in ways that would not draw attention that they missed a legitimate opportunity to increase the 1997 net income. According to both the notes and the statement of cash flows found in the original 10-K filing, Moonstay paid $43.4 million in cash during 1997 for costs associated with the 1996 restructuring plan. Included in this amount was a supposed $18.6 million for severance and other employee termination costs. However, the review by the two CPA firms only managed to find $21.2 million paid during 1997 for restructuring costs, or less than half the originally reported amount. In fact, the restated amount for severance and other employee termina- tion costs was only $10 million. So it appears that Moonstay had charged an extra $8.6 million to the restructuring reserve for payments to employees during 1997 for work done that year. Before posing a few questions to which you are to respond, shown below are some of the most important items from Moonstay's income statement and balance sheet as they were originally reported and as restated. Selected items from Moonstay Corporation=s Income Statements (Amounts in thousands, except for per share amounts) For the Year Ended December 28, 1997 For the Year Ended December 29, 1996 As As Originally Reported Originally Reported As Restated As Restated Net sales $1,168,182 $1,073,090 $984,236 $984,236 Cost of goods sold 837,683 830,956 900,573 896,938 Selling, general and administrative expense 131,056 152,653 214,029 221,655 Restructuring and asset impairment (benefit) charges (14,582) 154,869 110,122 Operating earnings (loss) 199,443 104,063 (285,235) (244,479) Loss on sale of discontinued operations, net of taxes (13,713) (14,017) (32,430) (39,140) Net earnings (loss) 109,415 38,301 (228,262) (208,481) Net earnings (loss) per share of common stock: Basic $1.29 $0.45 ($2.75) ($2.51) When it comes to the balance sheet, the restatement process did not result in dramatic changes in the December 29, 1996 Balance Sheet of Moonstay. There were some interesting changes, however, in the December 28, 1997 Balance Sheet, as shown below. Selected items from the December 28, 1997 Balance Sheet (Amounts in thousands, except for per share amounts) As Originally Reported As Restated Receivables, net $295,550 $228,460 Inventories 256,180 304,900 Total current assets 658,005 602,242 Property, plant and equipment, net 240,897 249,524 Trademarks, trade names, goodwill and other, net 221,382 207,162 Restructuring accrual 10,938 5,186 [Restructuring accrual at 12/29/96] [63,834] [51,725] Other current liabilities 80,913 118,899 Total current liabilities 198,099 233,127 Other long-term liabilities 141,109 154,300 Total shareholders' equity 531,937 472,079 Describe an alternative way to communicate the potential financial impact of a corporate restructuring that would avoid giving fraudsters the oppor- tunity to practice "creative" accounting.

Expert Answer:

Answer rating: 100% (QA)

retive unting is ls knwn s Erning mngement nd uld be referred t in unting rties s the ts tht fllws the letter f rules f stndrd unting rties but ertinly devite frm the sirit f thse rules retive unting ... View the full answer

Related Book For

Intermediate Accounting

ISBN: 978-0077400163

6th edition

Authors: J. David Spiceland, James Sepe, Mark Nelson

Posted Date:

Students also viewed these accounting questions

-

As an analyst at Delta Airlines, you are asked to help the operations staff. Operations has identified a new method of loading baggage that is expected to result in a 30 percent reduction in labor...

-

prepare a process diagram. AIS outdoor is a retail business selling outdoor entertainment goods such as tents, sleeping bags, camping furniture, etc. In addition to having stores across Australia,...

-

You are asked to design spring bumpers for the walls of a parking garage. A freely rolling 1200-kg car moving at 0.65 m/s is to compress the spring no more than 0.070 m before stopping. What should...

-

Harley-Davidson: Preparing for the Next Century There are very few products that are so exciting that people will tattoo your logo on their body. Richard Teerlink, Retired CEO, Harley-Davidson In...

-

Match each of the numbered definitions with the correct term in the following list. Write the letter of your choice in the answer column. a. Champerty b. Exculpatory clause c. Franchisor d. Gambling...

-

When revenue is generally recognized? Why has that date been chosen as the point at which to recognize the revenue resulting from the entire producing and selling process?

-

You throw a \(100-\mathrm{g}\) ball upward with a speed of \(19.8 \mathrm{~m} / \mathrm{s}\). How much work does the force of gravity do on the ball during its trip to its maximum height?

-

Following are a series of cost behavior graphs. The total cost is shown on the vertical (y) axis and the volume (activity) is shown on the horizontal (x) axis. For each of the following situations,...

-

You plan to deploy a dockerized application in an AWS ECS cluster. The application needs access to an S 3 bucket to read files. The ECS containers should have the AmazonS 3 ReadOnlyAccess permission....

-

You are buying a new car for $30,000 plus 5% taxes for a total cost of $31,500. You can pay cash for the entire amount by writing a check from your money market deposit account at the bank that...

-

Assume that you are in charge of special education for the Miami Dade School District. The district implemented a program which involves integrating autistic children with other children in the...

-

How would a professional option seller utilize the various option greeks to manage their underlying risk exposure?

-

Performance reviews are an integral part of which component of internal control? Multiple Choice Risk assessment. Control environment. Monitoring. Control activities

-

Queues serve major role in Your answer: O Simulation of limited resource allocation O Simulation of recursion Simulation of arbitrary linked list Simulation of heap sort

-

How do I post this to the ledger Received a check from Mainely Magic related to the Sept. 5th sale of 30 magical pencils. MM explained with the $13,500 payment that they couldn't pay their bill in...

-

What is the difference between a job-order costing and process costing? When do you use one or the other? Why is there a likely to be a situation of over or undercosted manufacturing overhead? What...

-

Vector A = 2 . 0 0 i + - 1 . 0 0 j and Vector B = 3 . 0 0 i + 4 . 0 0 j . What is Vector C = A - B ? A . 1 . 0 0 i + 5 . 0 0 j B . - 1 . 0 0 i + - 5 . 0 0 j C . - 1 . 0 0 i + 3 . 0 0 j D . 1 . 0 0 i...

-

Use this circle graph to answer following Exercises. 1. What fraction of areas maintained by the National Park Service are designated as National Recreation Areas? 2. What fraction of areas...

-

John has an investment opportunity that promises to pay him $16,000 in four years. He could earn a 6% annual return investing his money elsewhere. What is the maximum amount he would be willing to...

-

SLR Corporation has 1,000 units of each of its two products in its year-end inventory. Per unit data for each of the products are as follows: Determine the balance sheet carrying value of SLR's...

-

The following questions are used in the Kaplan CPA Review Course to study inventory while preparing for the CPA examination. Determine the response that best completes the statements or questions. 1....

-

For the periodic processes given below, find a valid schedule a. using standard RMS; b. adding one unit of overhead for each context switch. 22 P2 P1 P3 Process P1 P2 P3 Time Deadline 2 30 57 40 120...

-

For the periodic processes and deadlines given below: a. Schedule the processes using RMS. b. Schedule using EDF and compare the number of context switches required for EDF and RMS Process Time...

-

If you wanted to reduce the cache conflicts between the most computationally intensive parts of two processes, what are two ways that you could control the locations of the processes cache footprints?

Study smarter with the SolutionInn App