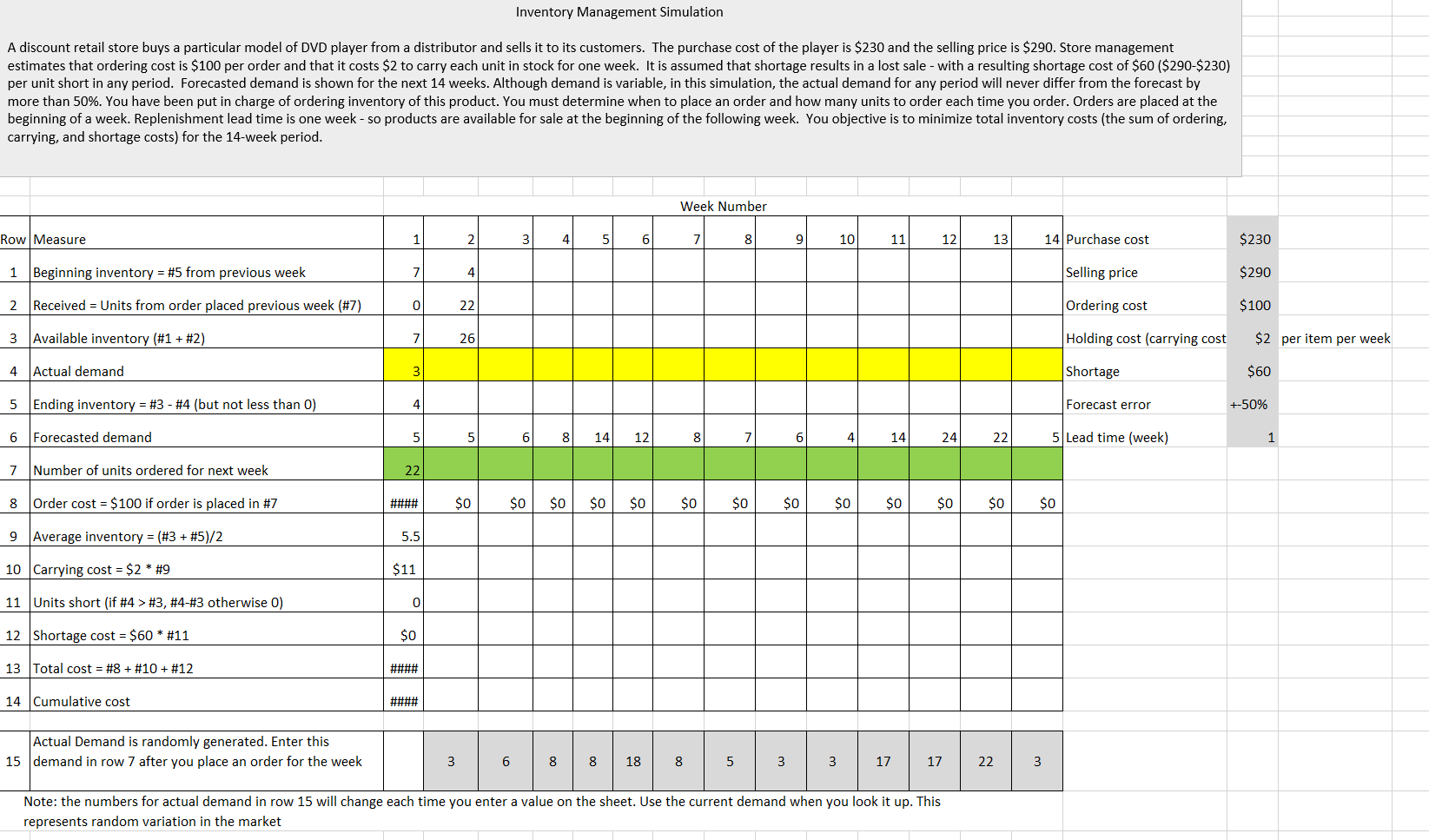

Question: Inventory Management Simulation A discount retail store buys a particular model of DVD player from a distributor and sells it to its customers. The purchase

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock