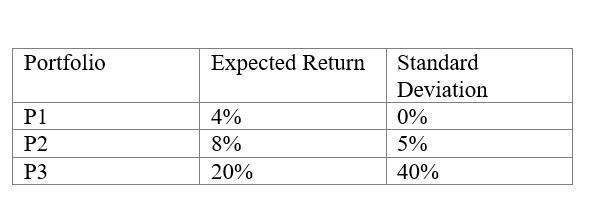

Investor A and investor B are mean-variance optimisers possessing quadratic utility. Consider the following three portfolios in

Fantastic news! We've Found the answer you've been seeking!

Question:

Investor A and investor B are mean-variance optimisers possessing quadratic utility. Consider the following three portfolios in the table below

Investor A has a risk aversion coefficient of 4. How risk averse Investor A is and how Investor B would rank portfolios, P1, P2 and P3.

How capital allocation lines can be used to select the best performing portfolio?

Expert Answer:

Question a Investor A has a risk aversion coefficient of 4 This means that she is very risk averse S... View the full answer

Related Book For

Microeconomics

ISBN: 9781464146978

1st Edition

Authors: Austan Goolsbee, Steven Levitt, Chad Syverson

Posted Date: