Question: Isabel exchanges a building with a fair market value (FMV) of $1,100,000 for $100,000 cash in addition to a building with fair market value (FMV)

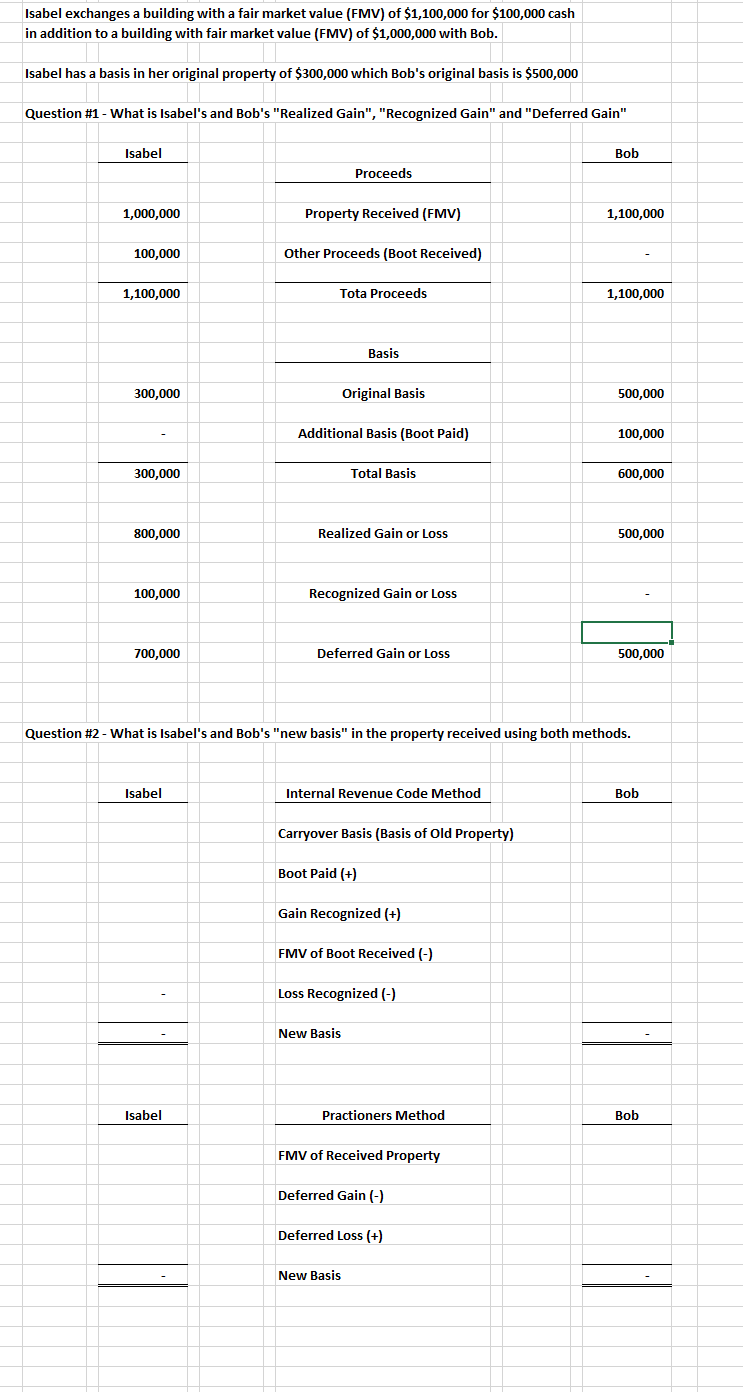

Isabel exchanges a building with a fair market value (FMV) of $1,100,000 for $100,000 cash in addition to a building with fair market value (FMV) of $1,000,000 with Bob. Isabel has a basis in her original property of $300,000 which Bob's original basis is $500,000 Question #1 - What is Isabel's and Bob's "Realized Gain", "Recognized Gain" and "Deferred Gain" Isabel Bob Proceeds 1,000,000 Property Received (FMV) 1,100,000 100,000 Other Proceeds (Boot Received) 1,100,000 Tota Proceeds 1,100,000 Basis 300,000 Original Basis 500,000 Additional Basis (Boot Paid) 100,000 300,000 Total Basis 600,000 800,000 Realized Gain or Loss 500,000 100,000 Recognized Gain or Loss 700,000 Deferred Gain or Loss 500,000 Question #2 - What is Isabel's and Bob's "new basis" in the property received using both methods. Isabel Internal Revenue Code Method Bob Carryover Basis (Basis of Old Property) Boot Paid (+) Gain Recognized (+) FMV of Boot Received (-) Loss Recognized (-) New Basis Isabel Practioners Method Bob FMV of Received Property Deferred Gain (-) Deferred Loss (+) New Basis

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts