Question: Isabel exchanges a building with a fair market value (FMV) of $1,100,000 for $100,000 cash in addition to a building with fair market value (FMV)

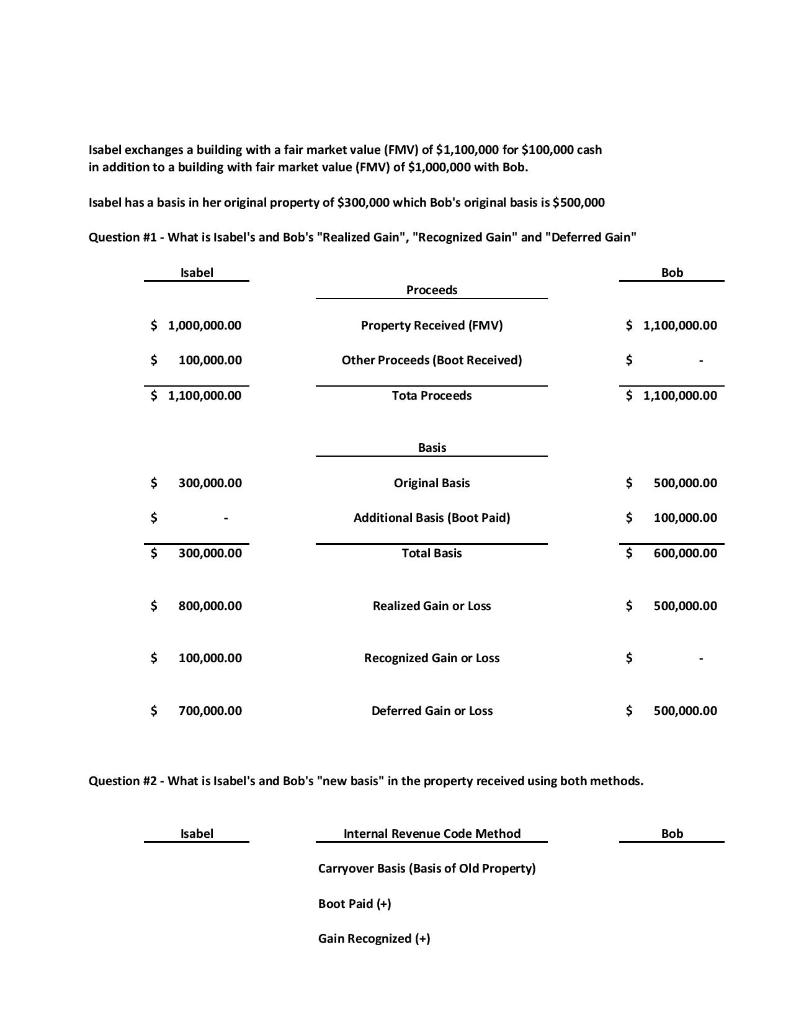

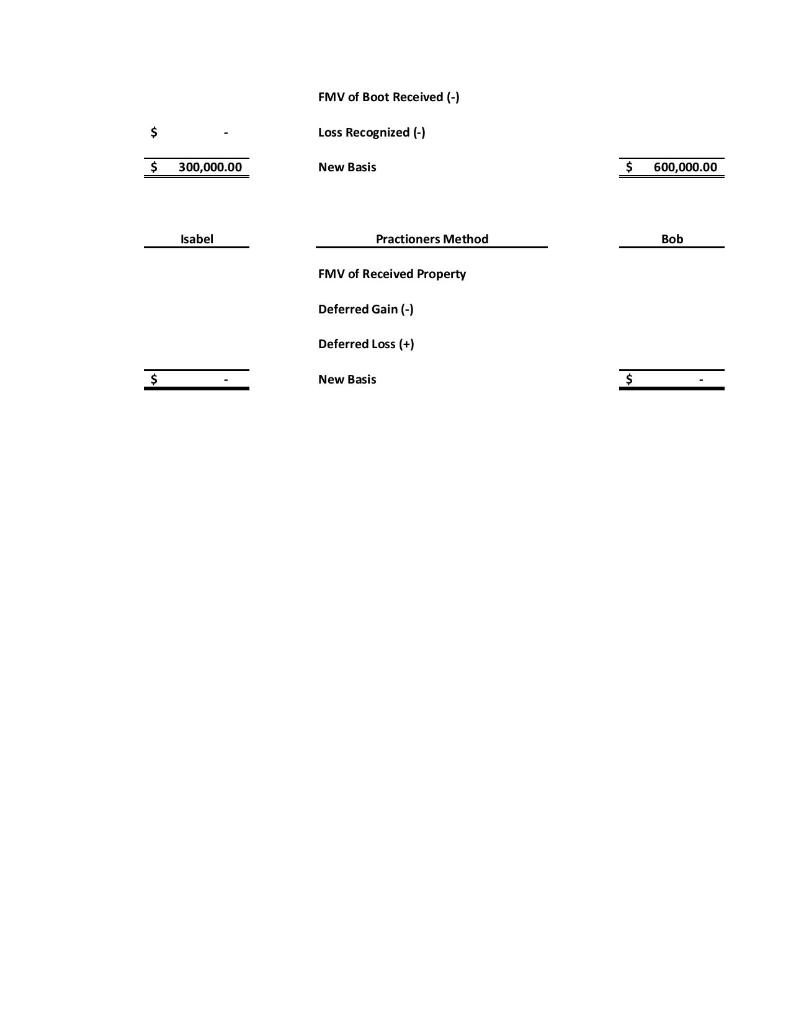

Isabel exchanges a building with a fair market value (FMV) of $1,100,000 for $100,000 cash in addition to a building with fair market value (FMV) of $1,000,000 with Bob. Isabel has a basis in her original property of $300,000 which Bob's original basis is $500,000 Question #1 - What is Isabel's and Bob's "Realized Gain", "Recognized Gain" and "Deferred Gain" Isabel Bob Proceeds $ 1,000,000.00 Property Received (FMV) $ 1,100,000.00 $ 100,000.00 Other Proceeds (Boot Received) $ $ $ 1,100,000.00 Tota Proceeds $ 1,100,000.00 Basis $ 300,000.00 Original Basis $ 500,000.00 $ Additional Basis (Boot Paid) $ 100,000.00 $ 300,000.00 Total Basis $ 600,000.00 $ 800,000.00 Realized Gain or Loss $ 500,000.00 $ 100,000.00 Recognized Gain or Loss $ $ 700,000.00 Deferred Gain or Loss $ 500,000.00 Question #2 - What is Isabel's and Bob's "new basis" in the property received using both methods. Isabel Internal Revenue Code Method Bob Carryover Basis (Basis of Old Property) Boot Paid (+) Gain Recognized (+) FMV of Boot Received (-) $ Loss Recognized (-) 300,000.00 New Basis 600,000.00 Isabel Practioners Method Bob FMV of Received Property Deferred Gain (-) Deferred Loss (+) New Basis

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts