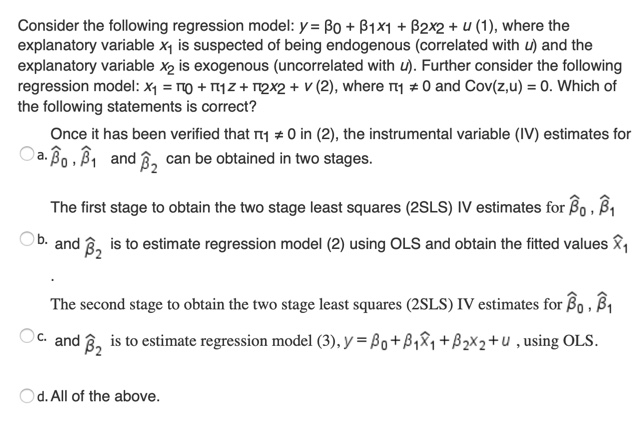

Question: ISonsider the following regression model: y: BC! + [31:1 + [3212 + u {1]. where the explanatory 1Irariable x1 is suspected of being endogenous [correlated

ISonsider the following regression model: y: BC! + [31:1 + [3212 + u {1]. where the explanatory 1Irariable x1 is suspected of being endogenous [correlated with u} and the explanatory variable :2 is exogenous {uncorrelated with u). Further consider the following regression modal: x1 = n0 + 111: + ngxg + H2], where n1 s i} and Danish] = 0. Which of the following statements is oorreot'? Ones it has been verified that n1 :2 b in {2]. the instrumental variable {W} estimates for a 'u. .61 and\" '32 oan be obtained' In two stages. The first stage to obtain the two stage least squares {EELS} IV estimates for ED , E1 ' '1 and '3': is to estimate regression model {2) using 0L3 and obtain the tted IIrsIIues E1 The second stage to obtain the two stage least squares (EELS) IV estimates for t: . E1 55- and g: is to estimate regression model (3), y =13\" +3121 +5213 + u , using 0L5. 'dll of the above

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts