Question: It a question about risk-free rate, expected return and the variance, the beta of risky asset, mean-variance efficient Consider an economy with two risky assets

It a question about risk-free rate, expected return and the variance, the beta of risky asset, mean-variance efficient

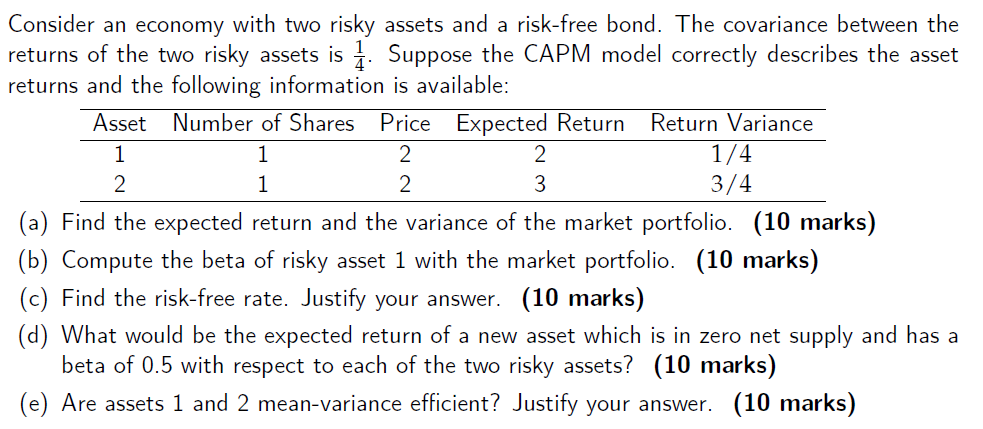

Consider an economy with two risky assets and a risk-free bond. The covariance between the returns of the two risky assets is %. Suppose the CAPM model correctly describes the asset returns and the following information is available: Asset Number of Shares Price Expected Return Return Variance l 1 2 2 1/4 2 1 2 3 3/4 a) Find the expected return and the variance of the market portfolio. (10 marks) ) l d) What would be the expected return of a new asset which is in zero net supply and has a beta of 0.5 with respect to each of the two risky assets? (10 marks) Compute the beta of risky asset 1 with the market portfolio. (10 marks) Find the risk-free rate. Justify your answer. (10 marks) (e) Are assets 1 and 2 meanvariance efficient? Justify your answer. (10 marks)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts