It is April 1, 2022, and a manager of Interstate Truckers, Inc. anticipates buying 1,000,000gal of diesel

Question:

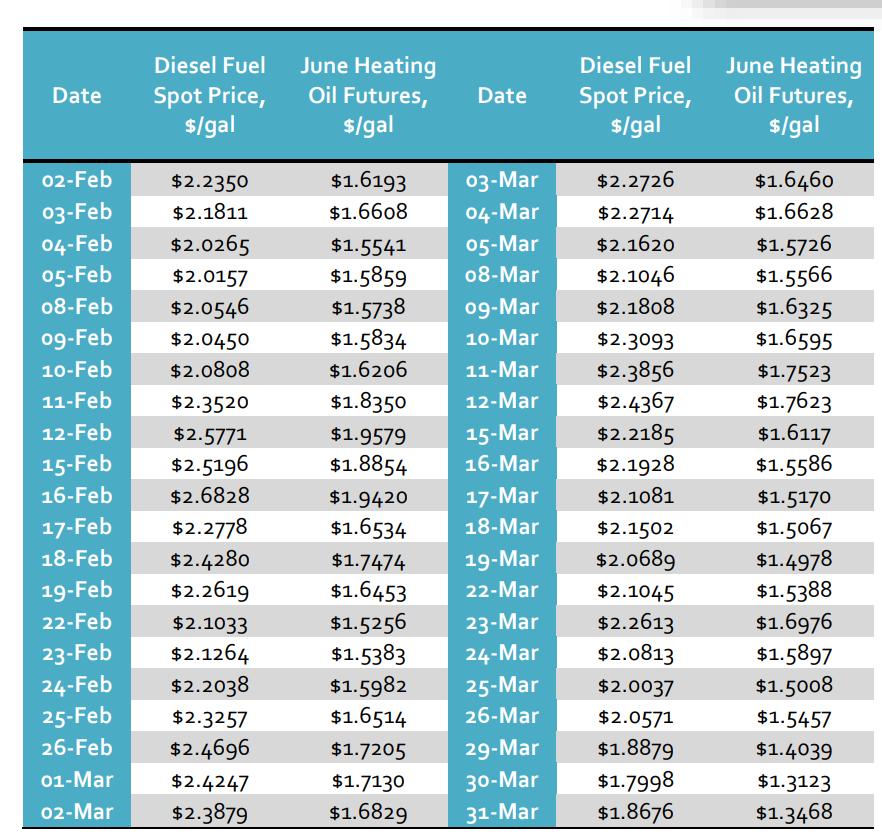

It is April 1, 2022, and a manager of Interstate Truckers, Inc. anticipates buying 1,000,000gal of diesel fuel on May 30, 2022. Diesel fuel currently sells on the spot market at $2.1742/gal. The manager is concerned about variability of the spot prices between April 1 and May 30 and wants to hedge this risk exposure. There is no futures market for diesel fuel, but the spot prices of diesel fuel tend to correlate with the prices of heating oil futures. The following table summarizes data on the spot prices of diesel fuel and futures prices of June heating oil contracts for the preceding two months Â

Â

a. Use the data above to find the standard deviations of spot and futures prices and the coefficient of correlation between the two. You might want to copy the table into Excel and perform calculations there.Â

b. Using the results from part a., find the variance-minimizing hedge ratio for hedging the volatility of diesel fuel spot price with the heating oil futures on April 1, 2022. Round your results to four decimal places.Â

c. Using the results from part b., find the optimal number of contracts that the manager has to buy on April 1, 2022, in order to hedge the purchase of 1,000,000gal of diesel fuel. The size of one heating oil futures contract is 42,000gal. Keep in mind that the exchange does not sell fractions of a contract.Â

d. Determine the actual hedge ratio that the manager will use if she ends up buying the number of contracts found in part c.

Expert Answer:

a To find the standard deviations of spot and futures prices and the coefficient of correlation betw... View the full answer

Intermediate Accounting IFRS

ISBN: 9781119607519

4th Edition

Authors: Donald E. Kieso, Jerry J. Weygandt, Terry D. Warfield