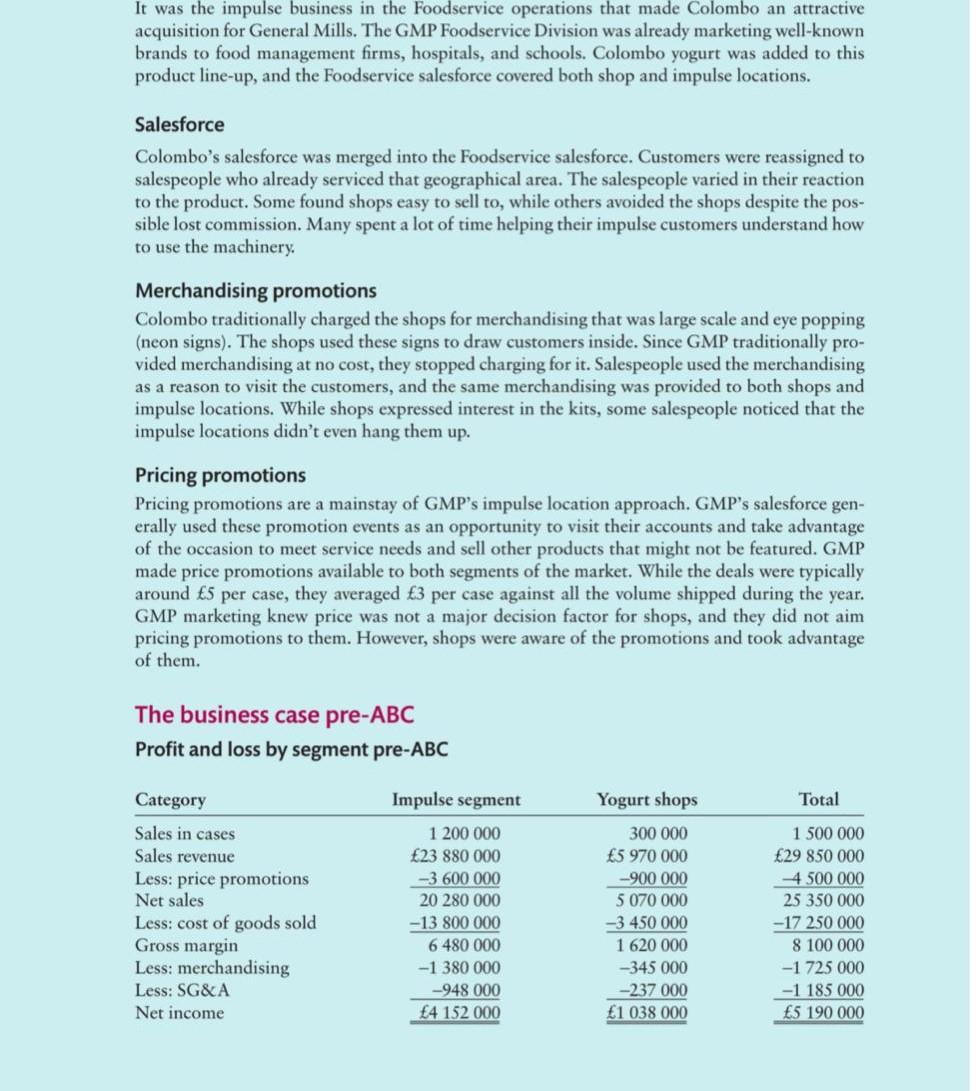

It was the impulse business in the Foodservice operations that made Colombo an attractive acquisition for...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

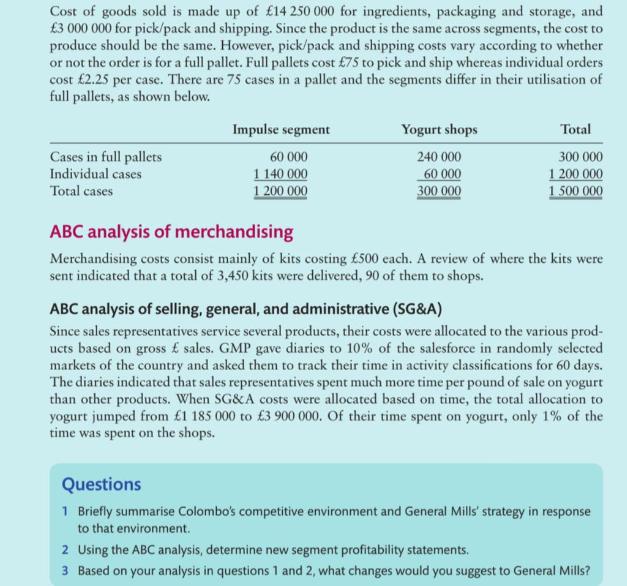

It was the impulse business in the Foodservice operations that made Colombo an attractive acquisition for General Mills. The GMP Foodservice Division was already marketing well-known brands to food management firms, hospitals, and schools. Colombo yogurt was added to this product line-up, and the Foodservice salesforce covered both shop and impulse locations. Salesforce Colombo's salesforce was merged into the Foodservice salesforce. Customers were reassigned to salespeople who already serviced that geographical area. The salespeople varied in their reaction to the product. Some found shops easy to sell to, while others avoided the shops despite the pos- sible lost commission. Many spent a lot of time helping their impulse customers understand how to use the machinery. Merchandising promotions Colombo traditionally charged the shops for merchandising that was large scale and eye popping (neon signs). The shops used these signs to draw customers inside. Since GMP traditionally pro- vided merchandising at no cost, they stopped charging for it. Salespeople used the merchandising as a reason to visit the customers, and the same merchandising was provided to both shops and impulse locations. While shops expressed interest in the kits, some salespeople noticed that the impulse locations didn't even hang them up. Pricing promotions Pricing promotions are a mainstay of GMP's impulse location approach. GMP's salesforce gen- erally used these promotion events as an opportunity to visit their accounts and take advantage of the occasion to meet service needs and sell other products that might not be featured. GMP made price promotions available to both segments of the market. While the deals were typically around 5 per case, they averaged 3 per case against all the volume shipped during the year. GMP marketing knew price was not a major decision factor for shops, and they did not aim pricing promotions to them. However, shops were aware of the promotions and took advantage of them. The business case pre-ABC Profit and loss by segment pre-ABC Category Impulse segment Yogurt shops Total Sales in cases Sales revenue Less: price promotions 1 200 000 23 880 000 -3 600 000 Net sales 20 280 000 5 070 000 Less: cost of goods sold -13 800 000 -3 450 000 Gross margin Less: merchandising Less: SG&A Net income 6 480 000 -1 380 000 -948 000 4 152 000 1 620 000 300 000 5 970 000 -900 000 -345 000 1 500 000 29 850 000 -4 500 000 25 350 000 -17 250 000 8 100 000 -1 725 000 -237 000 -1 185 000 1 038 000 5 190 000 Cost of goods sold is made up of 14 250 000 for ingredients, packaging and storage, and 3 000 000 for pick/pack and shipping. Since the product is the same across segments, the cost to produce should be the same. However, pick/pack and shipping costs vary according to whether or not the order is for a full pallet. Full pallets cost 75 to pick and ship whereas individual orders cost 2.25 per case. There are 75 cases in a pallet and the segments differ in their utilisation of full pallets, as shown below. Cases in full pallets Individual cases Total cases Impulse segment 60 000 1140 000 Yogurt shops 240 000 60 000 1 200 000 300 000 Total 300 000 1 200 000 1.500 000 ABC analysis of merchandising Merchandising costs consist mainly of kits costing 500 each. A review of where the kits were sent indicated that a total of 3,450 kits were delivered, 90 of them to shops. ABC analysis of selling, general, and administrative (SG&A) Since sales representatives service several products, their costs were allocated to the various prod- ucts based on gross sales. GMP gave diaries to 10% of the salesforce in randomly selected markets of the country and asked them to track their time in activity classifications for 60 days. The diaries indicated that sales representatives spent much more time per pound of sale on yogurt than other products. When SG&A costs were allocated based on time, the total allocation to yogurt jumped from 1 185 000 to 3 900 000. Of their time spent on yogurt, only 1% of the time was spent on the shops. Questions 1 Briefly summarise Colombo's competitive environment and General Mills' strategy in response to that environment. 2 Using the ABC analysis, determine new segment profitability statements. 3 Based on your analysis in questions 1 and 2, what changes would you suggest to General Mills? It was the impulse business in the Foodservice operations that made Colombo an attractive acquisition for General Mills. The GMP Foodservice Division was already marketing well-known brands to food management firms, hospitals, and schools. Colombo yogurt was added to this product line-up, and the Foodservice salesforce covered both shop and impulse locations. Salesforce Colombo's salesforce was merged into the Foodservice salesforce. Customers were reassigned to salespeople who already serviced that geographical area. The salespeople varied in their reaction to the product. Some found shops easy to sell to, while others avoided the shops despite the pos- sible lost commission. Many spent a lot of time helping their impulse customers understand how to use the machinery. Merchandising promotions Colombo traditionally charged the shops for merchandising that was large scale and eye popping (neon signs). The shops used these signs to draw customers inside. Since GMP traditionally pro- vided merchandising at no cost, they stopped charging for it. Salespeople used the merchandising as a reason to visit the customers, and the same merchandising was provided to both shops and impulse locations. While shops expressed interest in the kits, some salespeople noticed that the impulse locations didn't even hang them up. Pricing promotions Pricing promotions are a mainstay of GMP's impulse location approach. GMP's salesforce gen- erally used these promotion events as an opportunity to visit their accounts and take advantage of the occasion to meet service needs and sell other products that might not be featured. GMP made price promotions available to both segments of the market. While the deals were typically around 5 per case, they averaged 3 per case against all the volume shipped during the year. GMP marketing knew price was not a major decision factor for shops, and they did not aim pricing promotions to them. However, shops were aware of the promotions and took advantage of them. The business case pre-ABC Profit and loss by segment pre-ABC Category Impulse segment Yogurt shops Total Sales in cases Sales revenue Less: price promotions 1 200 000 23 880 000 -3 600 000 Net sales 20 280 000 5 070 000 Less: cost of goods sold -13 800 000 -3 450 000 Gross margin Less: merchandising Less: SG&A Net income 6 480 000 -1 380 000 -948 000 4 152 000 1 620 000 300 000 5 970 000 -900 000 -345 000 1 500 000 29 850 000 -4 500 000 25 350 000 -17 250 000 8 100 000 -1 725 000 -237 000 -1 185 000 1 038 000 5 190 000 Cost of goods sold is made up of 14 250 000 for ingredients, packaging and storage, and 3 000 000 for pick/pack and shipping. Since the product is the same across segments, the cost to produce should be the same. However, pick/pack and shipping costs vary according to whether or not the order is for a full pallet. Full pallets cost 75 to pick and ship whereas individual orders cost 2.25 per case. There are 75 cases in a pallet and the segments differ in their utilisation of full pallets, as shown below. Cases in full pallets Individual cases Total cases Impulse segment 60 000 1140 000 Yogurt shops 240 000 60 000 1 200 000 300 000 Total 300 000 1 200 000 1.500 000 ABC analysis of merchandising Merchandising costs consist mainly of kits costing 500 each. A review of where the kits were sent indicated that a total of 3,450 kits were delivered, 90 of them to shops. ABC analysis of selling, general, and administrative (SG&A) Since sales representatives service several products, their costs were allocated to the various prod- ucts based on gross sales. GMP gave diaries to 10% of the salesforce in randomly selected markets of the country and asked them to track their time in activity classifications for 60 days. The diaries indicated that sales representatives spent much more time per pound of sale on yogurt than other products. When SG&A costs were allocated based on time, the total allocation to yogurt jumped from 1 185 000 to 3 900 000. Of their time spent on yogurt, only 1% of the time was spent on the shops. Questions 1 Briefly summarise Colombo's competitive environment and General Mills' strategy in response to that environment. 2 Using the ABC analysis, determine new segment profitability statements. 3 Based on your analysis in questions 1 and 2, what changes would you suggest to General Mills?

Expert Answer:

Related Book For

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Posted Date:

Students also viewed these accounting questions

-

13 10 points eBook Print You are managing a portfolio of $1 million. Your target duration is 10 years, and you can invest in two bonds, a zero-coupon bond with maturity of five years and a...

-

What type of business is S. G. Cowen? How is this firm different from the other financial firms? How systems and operations of financial firms are different from other types of businesses - say...

-

Big Tech behaving badly: Why you can't trust Facebook and Google Facebook and Google have become the largest advertising agencies in the world and they've apparently done it by hoodwinking...

-

The costs of achieving emission reductions in the future will depend greatly on the types of policies used to reduce emissions today. Explain.

-

The Pampa Oil Company op-erates oil and gas exploration throughout the panhandle of Texas. The firm was recently approached by a wildcatter named William Wild Bill Donavan with the prospect to...

-

The following are independent items. 1. The excess amount of a charge to the accounting records (allowance method) over a charge to the tax return (direct writeoff method) for uncollectible...

-

The detailed dataflow diagram in Figure 14-16 decomposes the DFD for the expenditure cycle in Figure 14-15. Further decompose the process numbered 1.4.4, Receive Invoice, in detail.

-

Set up T accounts for Case Advising based on the work sheet in Exercise 6-1A and the chart of accounts provided below. Enter the existing balance for each account. Prepare closing entries in general...

-

X Domain: Range: (0,0) [0,0] (0,0) Q 80- Graph the exponential function g(x)=3x-2 To do this, plot two points on the graph of the function, and also draw the asymptote. Then click on the...

-

Using the following information: a. The bank statement balance is $3,800. b. The cash account balance is $3,949. c. Outstanding checks amount to $687. d. Deposits in transit are $703. e. The bank...

-

Sandhill Co. at the end of 2020, its first year of operations, prepared a reconciliation between pretax financial income and taxable income as follows: Pretax financial income $1080000 Estimated...

-

A company's 5-year bonds are yielding 6% per year. Treasury bonds with the same maturity are yielding 5.3% per year, and the real risk-free rate (r*) is 2.55%. The average inflation premium is 2.35%,...

-

Sheffield Co. is building a new hockey arena at a cost of $2,600,000. It received a downpayment of $460,000 from local businesses to support the project, and now needs to borrow $2,140,000 to...

-

Journalize basic transactions and adjusting entries. Instructions 7/31 Supplies Expense 900 Supplies 7/1 Bal. 1,100 7/31 900 7/10 650 Accounts Receivable 7/31 500 Salaries and Wages Expense 7/15 7/31...

-

Common Stockholders' Profitability Analysis A company reports the following: Net income Preferred dividends Average stockholders' equity $210,000 8,400 1,981,132 983,415 Average common stockholders'...

-

2. Let f(x) = x3 + 6x - 36x + 1 a) List all critical points, c, from the first derivative such that f'(c)=0 b) For each of the values in part a, calculate f"(c) c) According to the second derivative...

-

The National Collegiate Athletic Association (NCAA) and the National Federation of State High School Associations (NFHS) set a new standard for non-wood baseball bats. Their goal was to ensure that...

-

Financial accounting theory has accumulated a vast literature. A cynic might be inclined to say that the vastness of the literature is in sharp contrast to its impact on practice. (a) Describe the...

-

What is the basic difference between the purposes of financial and managerial accounting?

-

Is it possible for costs such as salaries or depreciation to end up as assets on the balance sheet? Explain.

Study smarter with the SolutionInn App