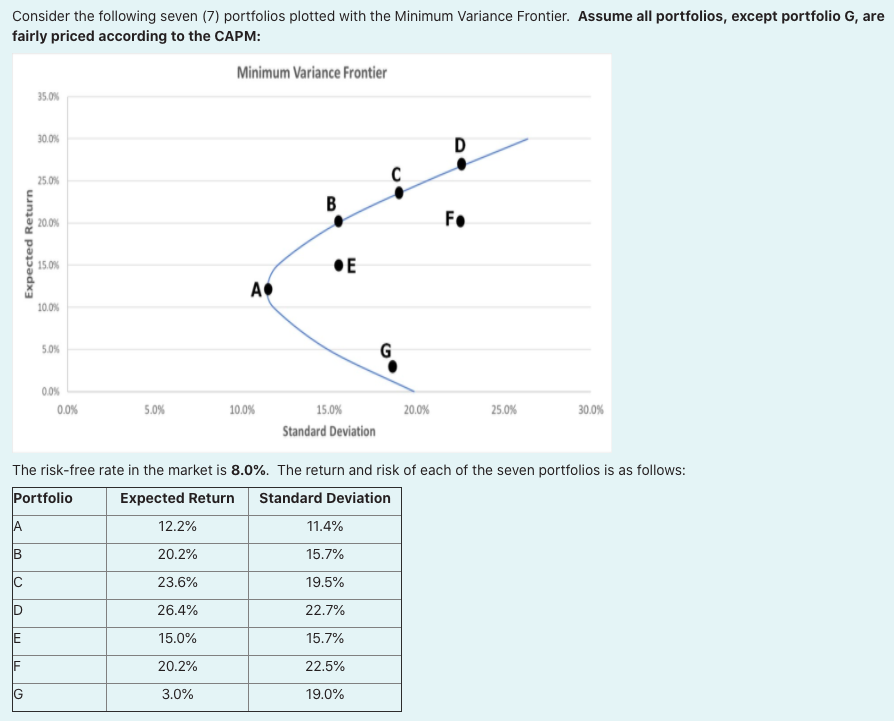

j) Assume that one of these portfolio's is the Market Portfolio and all portfolios, except Portfolio...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Absolutely Heres the solution for Treynor Measure of fairly priced assets Treynor Measure for Fairly Priced Assets When all portfolios except Portfolio G are fairly priced according to the CAPM it imp... View the full answer

Related Book For

Posted Date: