Question: Jones Manufacturing Inc. sponsored a defined benefit pension plan effective 1 January 20X7. The company uses the projected unit credit actuarial cost method for funding

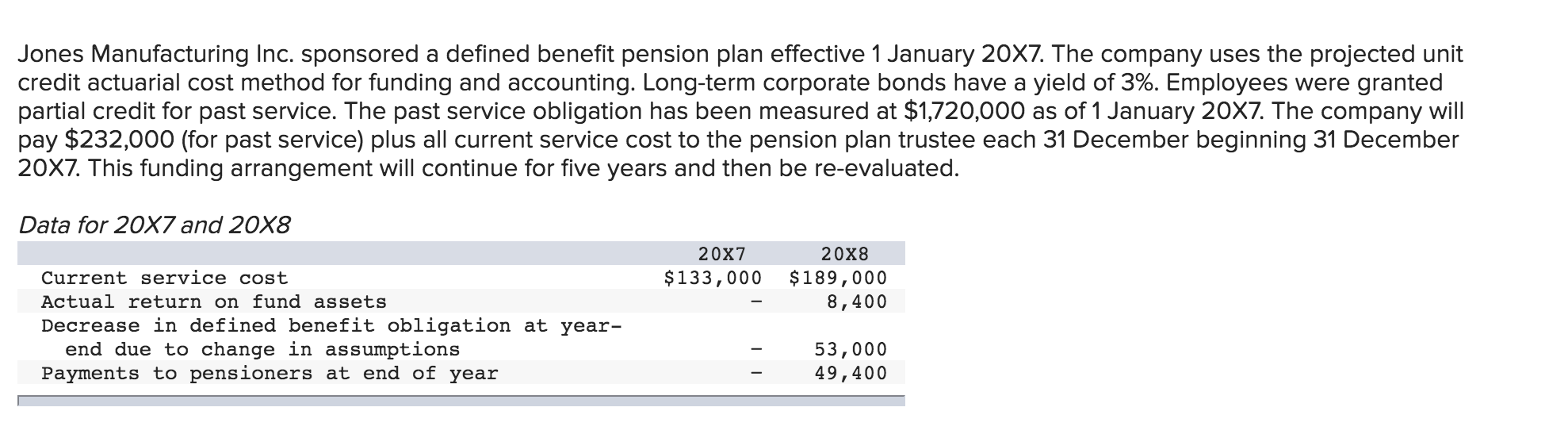

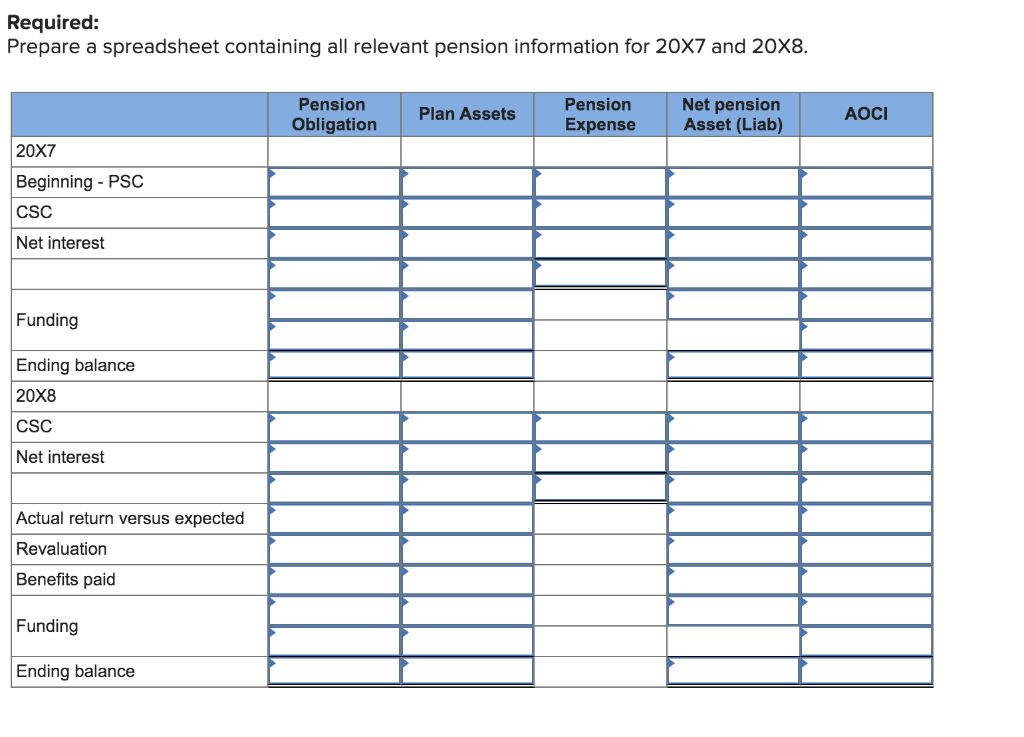

Jones Manufacturing Inc. sponsored a defined benefit pension plan effective 1 January 20X7. The company uses the projected unit credit actuarial cost method for funding and accounting. Long-term corporate bonds have a yield of 3%. Employees were granted partial credit for past service. The past service obligation has been measured at $1,720,000 as of 1 January 20X7. The company will pay $232,000 (for past service) plus all current service cost to the pension plan trustee each 31 December beginning 31 December 20X7. This funding arrangement will continue for five years and then be re-evaluated. Data for 20X7 and 20x8 20x7 $133,000 2008 $189,000 8,400 Current service cost Actual return on fund assets Decrease in defined benefit obligation at year- end due to change in assumptions Payments to pensioners at end of year 53,000 49,400 Required: Prepare a spreadsheet containing all relevant pension information for 20X7 and 20X8. Pension Obligation Plan Assets Pension Expense Net pension Asset (Liab) AOCI 20X7 Beginning - PSC CSC Net interest Funding i Ending balance 20X8 CSC Net interest Actual return versus expected Revaluation Benefits paid Funding Ending balance Jones Manufacturing Inc. sponsored a defined benefit pension plan effective 1 January 20X7. The company uses the projected unit credit actuarial cost method for funding and accounting. Long-term corporate bonds have a yield of 3%. Employees were granted partial credit for past service. The past service obligation has been measured at $1,720,000 as of 1 January 20X7. The company will pay $232,000 (for past service) plus all current service cost to the pension plan trustee each 31 December beginning 31 December 20X7. This funding arrangement will continue for five years and then be re-evaluated. Data for 20X7 and 20x8 20x7 $133,000 2008 $189,000 8,400 Current service cost Actual return on fund assets Decrease in defined benefit obligation at year- end due to change in assumptions Payments to pensioners at end of year 53,000 49,400 Required: Prepare a spreadsheet containing all relevant pension information for 20X7 and 20X8. Pension Obligation Plan Assets Pension Expense Net pension Asset (Liab) AOCI 20X7 Beginning - PSC CSC Net interest Funding i Ending balance 20X8 CSC Net interest Actual return versus expected Revaluation Benefits paid Funding Ending balance

Step by Step Solution

There are 3 Steps involved in it

I have prepared a spreadsheet with all relevant ... View full answer

Get step-by-step solutions from verified subject matter experts

Document Format (1 attachment)

20250321_104014.xlsx

300 KBs Excel File