Question: Just explain the part I added red notice for it Refrence Deegan. (2016). Financial Accounting . McGraw-Hill Education, Australia Refrence Deegan. (2016). Financial Accounting .

Just explain the part I added red notice for it

Refrence

Deegan. (2016). Financial Accounting . McGraw-Hill Education, Australia

Refrence

Deegan. (2016). Financial Accounting . McGraw-Hill Education, Australia

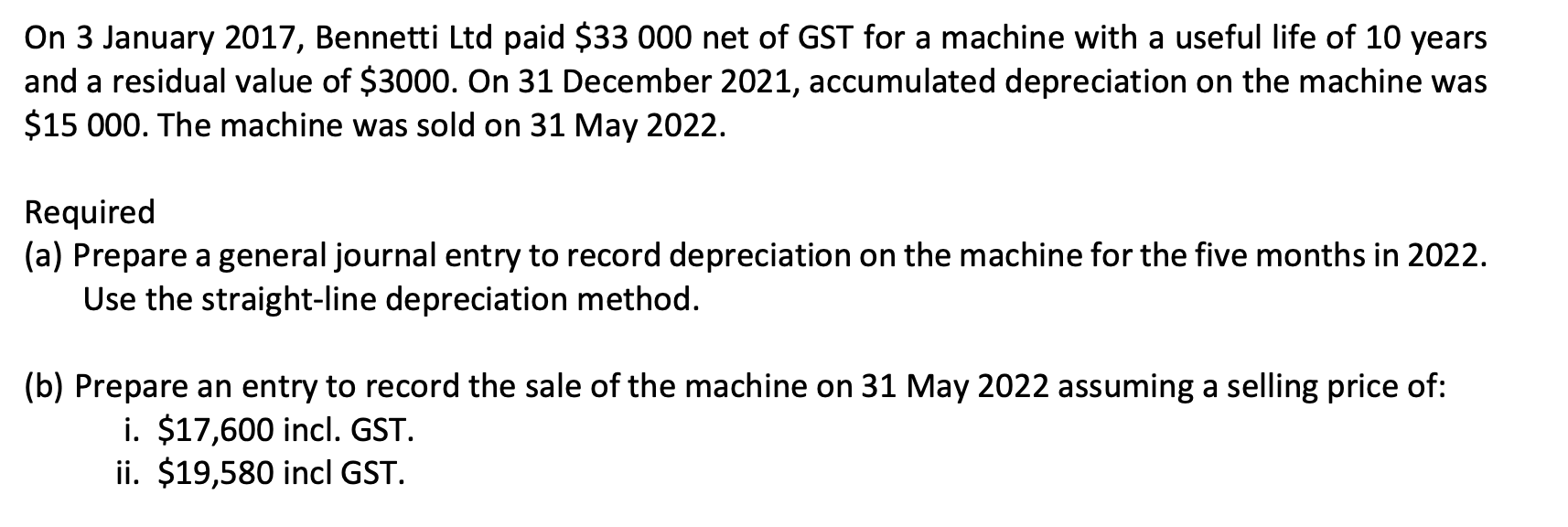

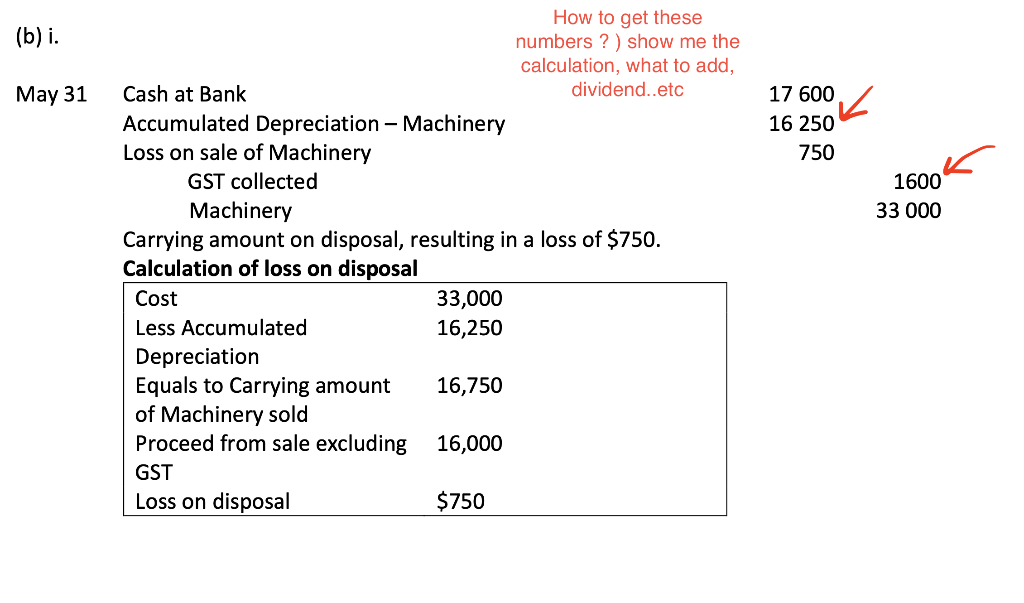

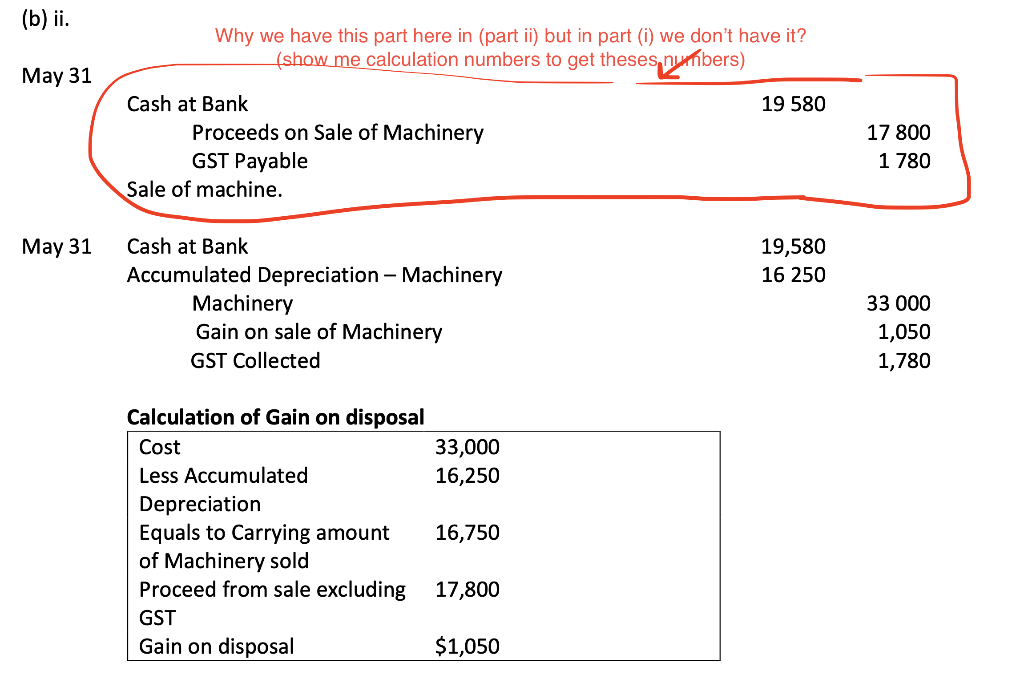

On 3 January 2017, Bennetti Ltd paid $33 000 net of GST for a machine with a useful life of 10 years and a residual value of $3000. On 31 December 2021, accumulated depreciation on the machine was $15 000. The machine was sold on 31 May 2022. Required (a) Prepare a general journal entry to record depreciation on the machine for the five months in 2022. Use the straight-line depreciation method. (b) Prepare an entry to record the sale of the machine on 31 May 2022 assuming a selling price of: i. $17,600 incl. GST. ii. $19,580 incl GST. (b) i. May 31 17 600 // 16 250 750 1600 33 000 How to get these numbers ?) show me the calculation, what to add, Cash at Bank dividend..etc Accumulated Depreciation - Machinery Loss on sale of Machinery GST collected Machinery Carrying amount on disposal, resulting in a loss of $750. Calculation of loss on disposal Cost 33,000 Less Accumulated 16,250 Depreciation Equals to carrying amount 16,750 of Machinery sold Proceed from sale excluding 16,000 GST Loss on disposal $750 (b) ii. Why we have this part here in (part ii) but in part (i) we don't have it? (show me calculation numbers to get theses, numbers) May 31 19 580 Cash at Bank Proceeds on Sale of Machinery GST Payable Sale of machine. 17 800 1 780 May 31 19,580 16 250 Cash at Bank Accumulated Depreciation - Machinery Machinery Gain on sale of Machinery GST Collected 33 000 1,050 1,780 Calculation of Gain on disposal Cost 33,000 Less Accumulated 16,250 Depreciation Equals to Carrying amount 16,750 of Machinery sold Proceed from sale excluding 17,800 GST Gain on disposal $1,050

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts