Question: Just need the answer for c) d) 3. Fix 7 > 0, and let (2. F. F. P) be filtered probability space and {Wiloster a

Just need the answer for c) d)

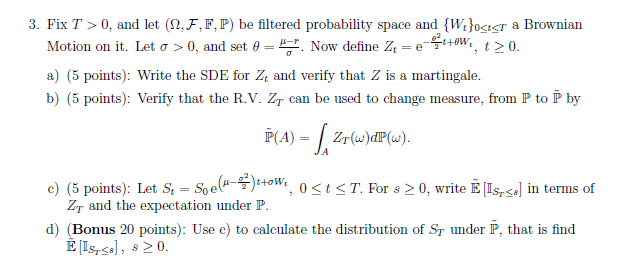

3. Fix 7 > 0, and let (2. F. F. P) be filtered probability space and {Wiloster a Brownian Motion on it. Let o > 0, and set 0 = 4. Now define Zz = e- 7tteWr, { > 0. a) (5 points): Write the SDE for Zt and verify that Z is a martingale. b) (5 points): Verify that the R.V. Zy can be used to change measure, from P to P by IP(A) = Zr(w) dIP (w). c) (5 points): Let St = Soe(#-7)tow, 0 0, write E[Is

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock