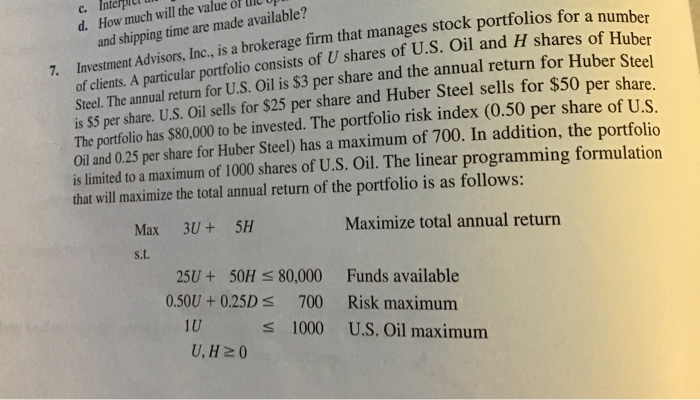

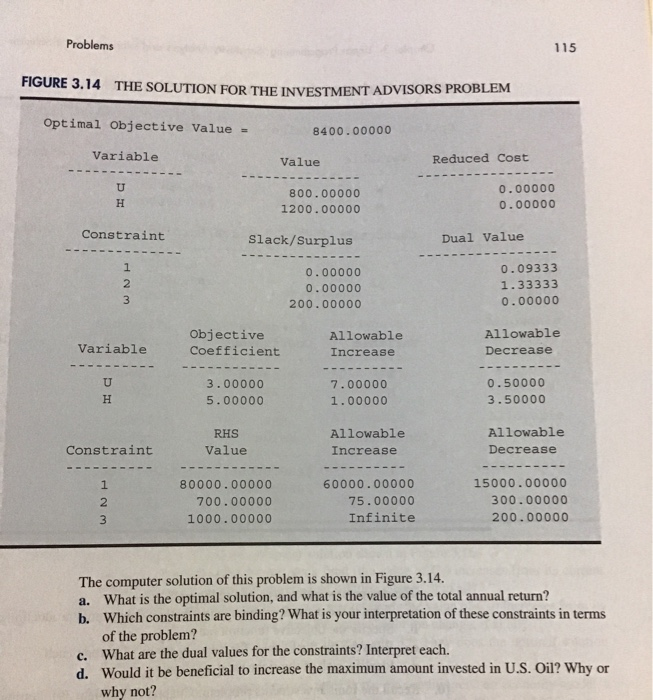

Question: k portfolios for a number c. Interpie d. How much will the value of life and shipping time are made available? Investment Advisors, Inc., is

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock