Question: ...l Telenor 8:12 AM 18% assignment 6.docx U Examples 1. An individual has $35,000 invested in a stock with a beta of 0.8 and another

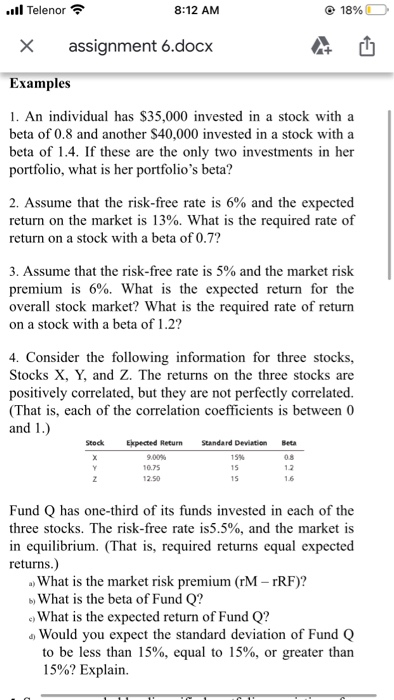

...l Telenor 8:12 AM 18% assignment 6.docx U Examples 1. An individual has $35,000 invested in a stock with a beta of 0.8 and another $40,000 invested in a stock with a beta of 1.4. If these are the only two investments in her portfolio, what is her portfolio's beta? 2. Assume that the risk-free rate is 6% and the expected return on the market is 13%. What is the required rate of return on a stock with a beta of 0.7? 3. Assume that the risk-free rate is 5% and the market risk premium is 6%. What is the expected return for the overall stock market? What is the required rate of return on a stock with a beta of 1.2? 4. Consider the following information for three stocks, Stocks X, Y, and Z. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) Stock X Y z Expected Return 9.00 10.75 12.50 Standard Deviation 15% 15 15 Beta 08 12 16 Fund Q has one-third of its funds invested in each of the three stocks. The risk-free rate is5.5%, and the market is in equilibrium. (That is, required returns equal expected returns.) . What is the market risk premium (rM TRF)? What is the beta of Fund Q? What is the expected return of Fund Q? Would you expect the standard deviation of Fund Q to be less than 15%, equal to 15%, or greater than 15%? Explain ...Telenor 8:12 AM 18% assignment 6.docx U 5. Suppose you held a diversified portfolio consisting of a $7,500 investment in each of 20 different common stocks. The portfolio's beta is 1.12. Now suppose you decided to sell one of the stocks in your portfolio with a beta of 1.0 for $7,500 and use the proceeds to buy another stock with a beta of 1.75. What would your portfolio's new beta be? 6. Stock X has a 10% expected return, a beta coefficient of 0.9, and a 35% standard deviation of expected returns. Stock Y has a 12.5% expected return, a beta coefficient of 1.2, and a 25% standard deviation. The risk-free rate is 6%, and the market risk premium is 5%. Calculate each stock's coefficient of variation. Which stock is riskier for a diversified investor? Calculate each stock's required rate of return. On the basis of the two stocks' expected and required returns, which stock would be more attractive to a diversified investor? Calculate the required return of a portfolio that has $7,500 invested in Stock X and $2,500 invested in Stock Y. If the market risk premium increased to 6%, which of the two stocks would have the larger increase in its required return? Problems for Assignment d) 1. An investor has a two-stock portfolio with $25,000 invested in Stock X and$50,000 invested in Stock Y. X's beta is 1.50, and Y's beta is 0.60. What is thebeta of the investor's portfolio? 2. A stock has a beta of 1.2. Assume that the risk-free rate is 4.5% and the market risk premium is 5%. What is the stock's required rate of return? stock's required rate of return! 3. A stock has a required return of 11%, the risk-free rate is 7%, and the market risk premium is 4%. What is the stock's beta? b) If the market risk premium increased to 6%, what would happen to the stocks required rate of return? Assume that the risk-free rate and the beta remain unchanged. 4. Suppose you are the money manager of a $4 millioninvestment fund. The fund consists of four stocks with the following investments and betas: Stock A B Investment $ 400,000 600,000 1.000.000 2,000,000 Beta 1.50 10.SO 125 0.75 If the market's required rate of return is 14% and the risk-free rate is 6%, what is the fundsrequired rate of return? 5. Bradford Manufacturing Company has a beta of 1.45, while Farley Industries has a beta of 0.85. The required return on an index fund that holds the entire stock market is 12.0%. The risk-free rate of interest is 5%. By how much does Bradford's required return exceed Farley's required return? 6. Calculate the required rate of return for Manning Enterprises assuming that investors expect a 3.5% rate of inflation in the future. The real risk-free rate is 2.5%, and the market risk premium is 6.5%. Manning has a beta of 1.7, and its realized rate of return has averaged 13.5% over the past 5 years. 7. You have been managing a $5 million portfolio that has a beta of 1.25 and a required rate of return of 12%. The current risk-free rate is 5.25%. Assume that you receive another $500,000. If you invest the money in a stock with a beta of 0.75, what will be the required return on your $5.5 million portfolio? 8. A mutual fund manager has a $20 million portfolio with a beta of 1.5. The risk-free rate is 4.5%, and the market risk premium is 5.5%. The manager expects to receive an additional $5 million, which she plans to invest in a number of stocks. After investing the additional funds, she wants the fund's required return to be 13%. What should be the average beta of the new stocks added to the portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts