Question: . L04-11 PROBLEM 48-6 Step-Down Method versus Direct Method: Predetermined Overhead Rates L04-10 The Sendai Co., Ltd. of Japan has budgeted costs in its various

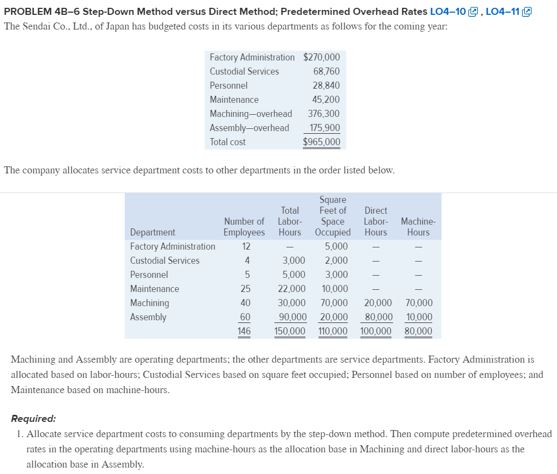

. L04-11 PROBLEM 48-6 Step-Down Method versus Direct Method: Predetermined Overhead Rates L04-10 The Sendai Co., Ltd. of Japan has budgeted costs in its various departments as follows for the coming year. Factory Administration $270,000 Custodial Services 68,760 Personnel 28.840 Maintenance 45,200 Machining-overhead 376,300 Assembly-overhead 175,900 Total cost $965,000 The company allocates service department costs to other departments in the order listed below. Number of Employees 12 Total Labor Hours Square Feet of Space Occupied Direct Labor- Houts Machine Houts 5.000 Department Factory Administration Custodial Services Personnel Maintenance Machining Assembly 25 3,000 5,000 22,000 30,000 90,000 150.000 2,000 3,000 10,000 70,000 20,000 110.000 40 20,000 80,000 100.000 70,000 10.000 80.000 Machining and Assembly are operating departments: the other departments are service departments. Factory Administration is allocated based on labor-hours: Custodial Services based on square feet occupied: Personnel based on number of employees, and Maintenance based on machine-hours. Required: 1. Allocate service department costs to consuming departments by the step-down method. Then compute predetermined overhead rates in the operating departments using machine hours as the allocation base in Machining and direct labor-hours as the allocation base in Assembly

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts