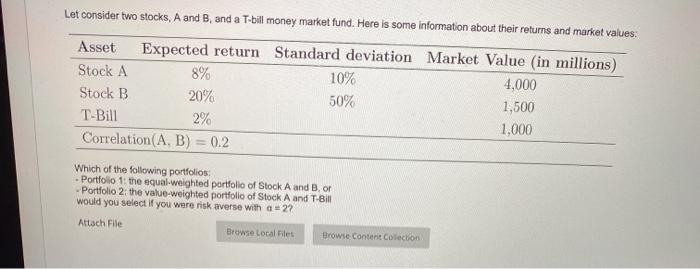

Question: Let consider two stocks, A and B and a T-bill money market fund. Here is some information about their returns and market values: 8% Asset

Let consider two stocks, A and B and a T-bill money market fund. Here is some information about their returns and market values: 8% Asset Expected return Standard deviation Market Value (in millions) Stock A 10% 4,000 Stock B 20% 50% 1,500 T-Bill 2% 1.000 Correlation(A. B) = 0.2 Which of the following portfolios: Portfolio 1: the equal weighted portfolio of Stock A and B. o Portfolio 2: the value-weighted portfolio of Stock A and T-Bill would you select if you were risk averse with a = 22 Attach File Browse Local Files Browse Content Collection

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock