Question: Let Z be a Wiener process. Given a non-dividend paying stock with expected rate of return u and volatility o, assume that the stock price

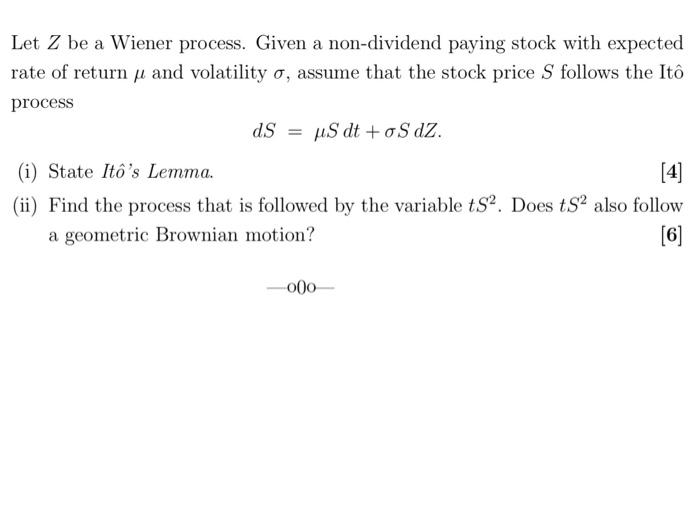

Let Z be a Wiener process. Given a non-dividend paying stock with expected rate of return u and volatility o, assume that the stock price S follows the It process dS = us dt +oS dz. (i) State Ito's Lemma. [4] (ii) Find the process that is followed by the variable ts. Does ts also follow a geometric Brownian motion? [6] -000 Let Z be a Wiener process. Given a non-dividend paying stock with expected rate of return u and volatility o, assume that the stock price S follows the It process dS = us dt +oS dz. (i) State Ito's Lemma. [4] (ii) Find the process that is followed by the variable ts. Does ts also follow a geometric Brownian motion? [6] -000

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock