Question: Let's work out a concrete example of two comparable bonds. The first bond is a zero-coupon bond with a time until maturity of four years.

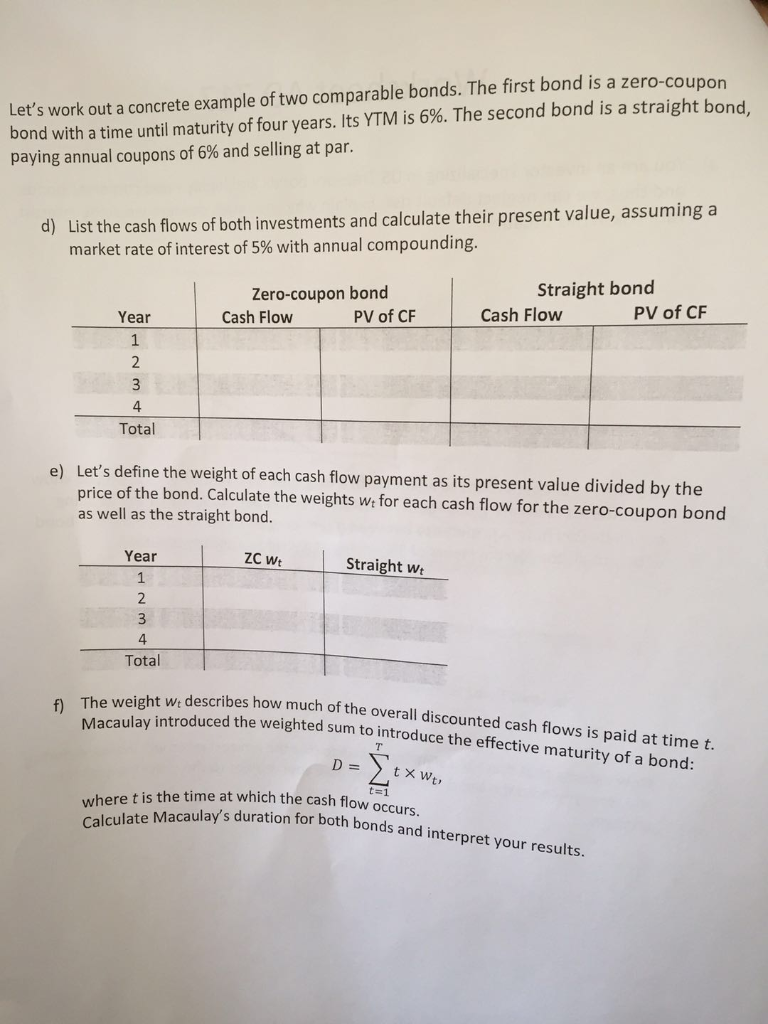

Let's work out a concrete example of two comparable bonds. The first bond is a zero-coupon bond with a time until maturity of four years. Its YTM is 6%. The second bond is a straight bond, paying annual coupons of 6% and selling at par. List the cash flows of both investments and calculate their present value, assuming a market rate of interest of 5% with annual compounding. d) Straight bond Zero-coupon bond Cash Flow Cash Flovw PV of CF Year 1 PV of CF 4 Total Let's define the weight of each cash flow payment as its present value divided by the price of the bond. Calculate the weights we for each cash flow for the zero-coupon bond as well as the straight bond. e) Year Straight w 4 Total eight w describes how much of the overall discounted cash flows is paid at time t. he weight Wt descr lay introduced the weighted sum to introduce the effective maturity of a bond: here t is the time at which the cash flow occurs calculate Macaulay's duration for both bond and interpret your results. Let's work out a concrete example of two comparable bonds. The first bond is a zero-coupon bond with a time until maturity of four years. Its YTM is 6%. The second bond is a straight bond, paying annual coupons of 6% and selling at par. List the cash flows of both investments and calculate their present value, assuming a market rate of interest of 5% with annual compounding. d) Straight bond Zero-coupon bond Cash Flow Cash Flovw PV of CF Year 1 PV of CF 4 Total Let's define the weight of each cash flow payment as its present value divided by the price of the bond. Calculate the weights we for each cash flow for the zero-coupon bond as well as the straight bond. e) Year Straight w 4 Total eight w describes how much of the overall discounted cash flows is paid at time t. he weight Wt descr lay introduced the weighted sum to introduce the effective maturity of a bond: here t is the time at which the cash flow occurs calculate Macaulay's duration for both bond and interpret your results

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts