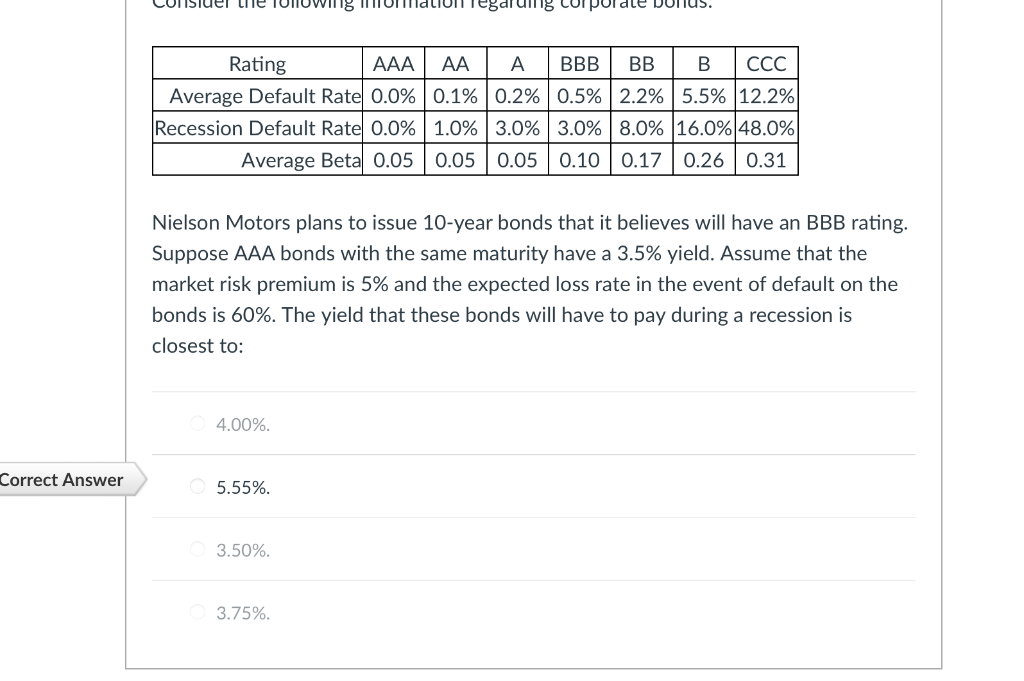

Question: LITE 18 corporate Duius. Rating AAA AA A BBB BB B CCC Average Default Rate 0.0% 0.1% 0.2% 0.5% 2.2% 5.5% 12.2% Recession Default Rate

LITE 18 corporate Duius. Rating AAA AA A BBB BB B CCC Average Default Rate 0.0% 0.1% 0.2% 0.5% 2.2% 5.5% 12.2% Recession Default Rate 0.0% 1.0% 3.0% 3.0% 8.0% 16.0% 48.0% Average Beta 0.05 0.05 0.05 0.10 0.17 0.26 0.31 Nielson Motors plans to issue 10-year bonds that it believes will have an BBB rating. Suppose AAA bonds with the same maturity have a 3.5% yield. Assume that the market risk premium is 5% and the expected loss rate in the event of default on the bonds is 60%. The yield that these bonds will have to pay during a recession is closest to: 4.00% Correct Answer 5.55% 3.50% 3.75%

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock