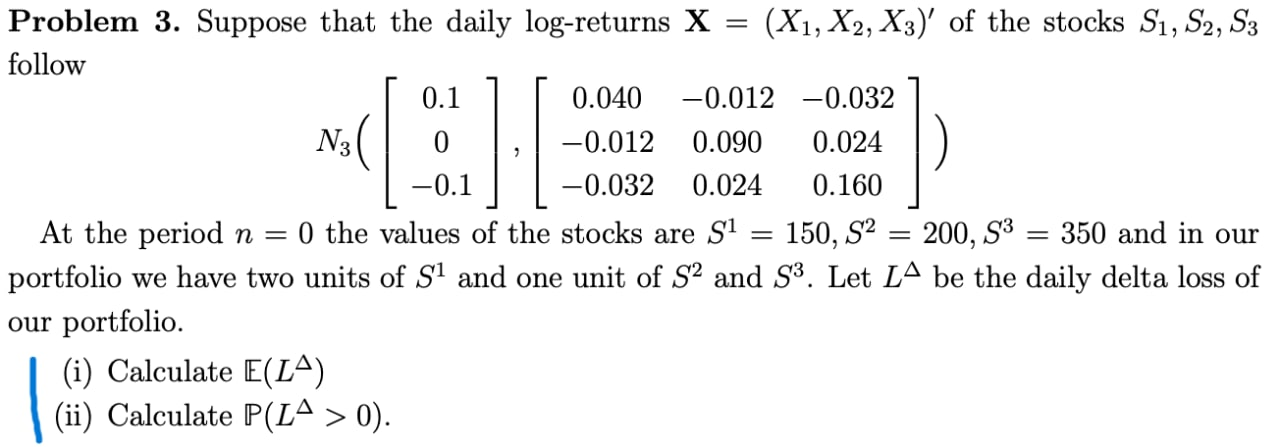

Question: = m () Problem 3. Suppose that the daily log-returns X (X1, X2, X3)' of the stocks S1, S2, S3 follow 0.1 0.040 -0.012 -0.032

= m () Problem 3. Suppose that the daily log-returns X (X1, X2, X3)' of the stocks S1, S2, S3 follow 0.1 0.040 -0.012 -0.032 0 -0.012 0.090 0.024 -0.1 -0.032 0.024 0.160 At the period n = O the values of the stocks are Si , S3 350 and in our portfolio we have two units of S1 and one unit of S2 and 53. Let L4 be the daily delta loss of our portfolio (i) Calculate E(LA) (ii) Calculate P(L4 > 0). 150, S2 = 200, = m () Problem 3. Suppose that the daily log-returns X (X1, X2, X3)' of the stocks S1, S2, S3 follow 0.1 0.040 -0.012 -0.032 0 -0.012 0.090 0.024 -0.1 -0.032 0.024 0.160 At the period n = O the values of the stocks are Si , S3 350 and in our portfolio we have two units of S1 and one unit of S2 and 53. Let L4 be the daily delta loss of our portfolio (i) Calculate E(LA) (ii) Calculate P(L4 > 0). 150, S2 = 200

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts