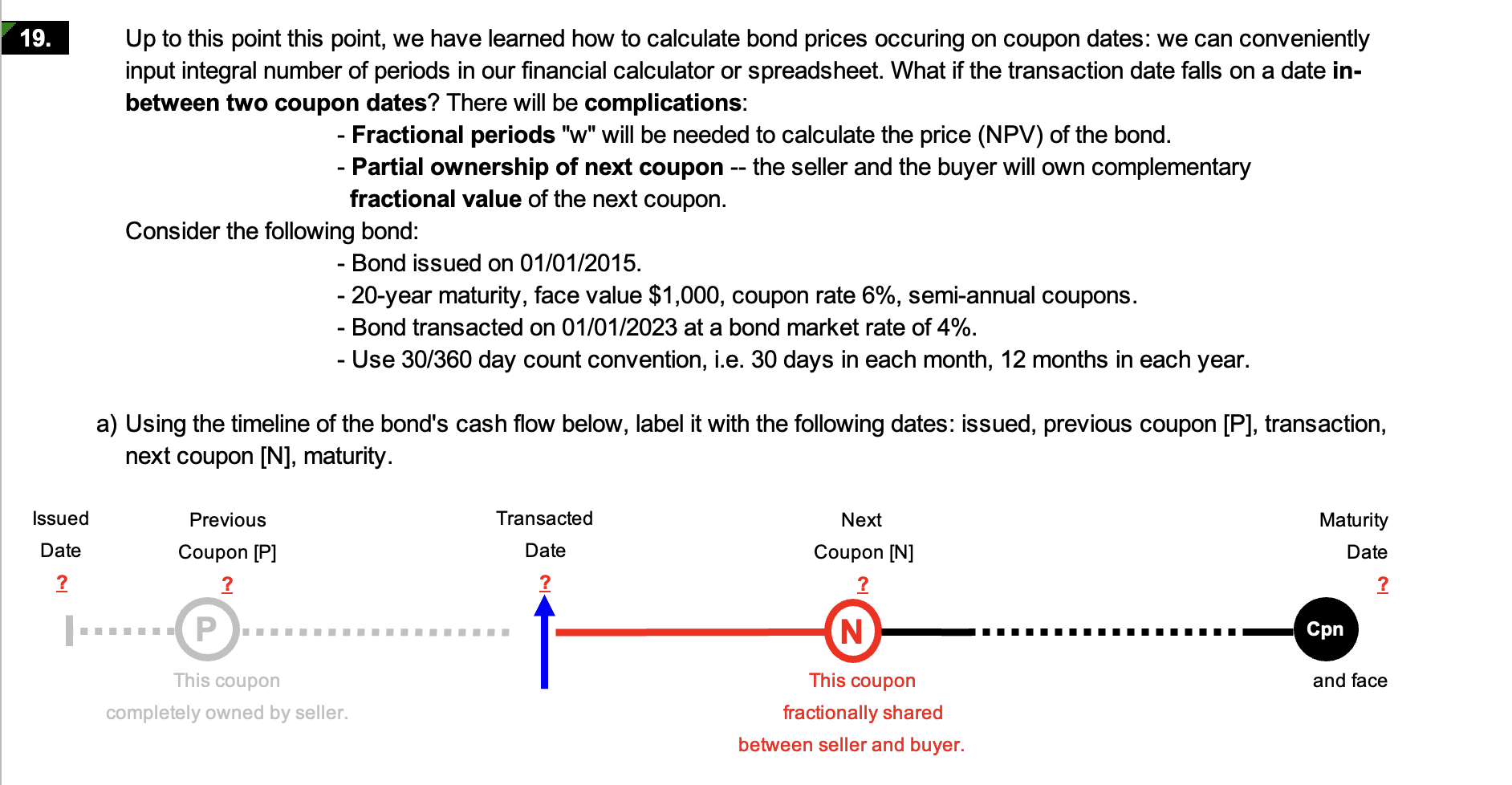

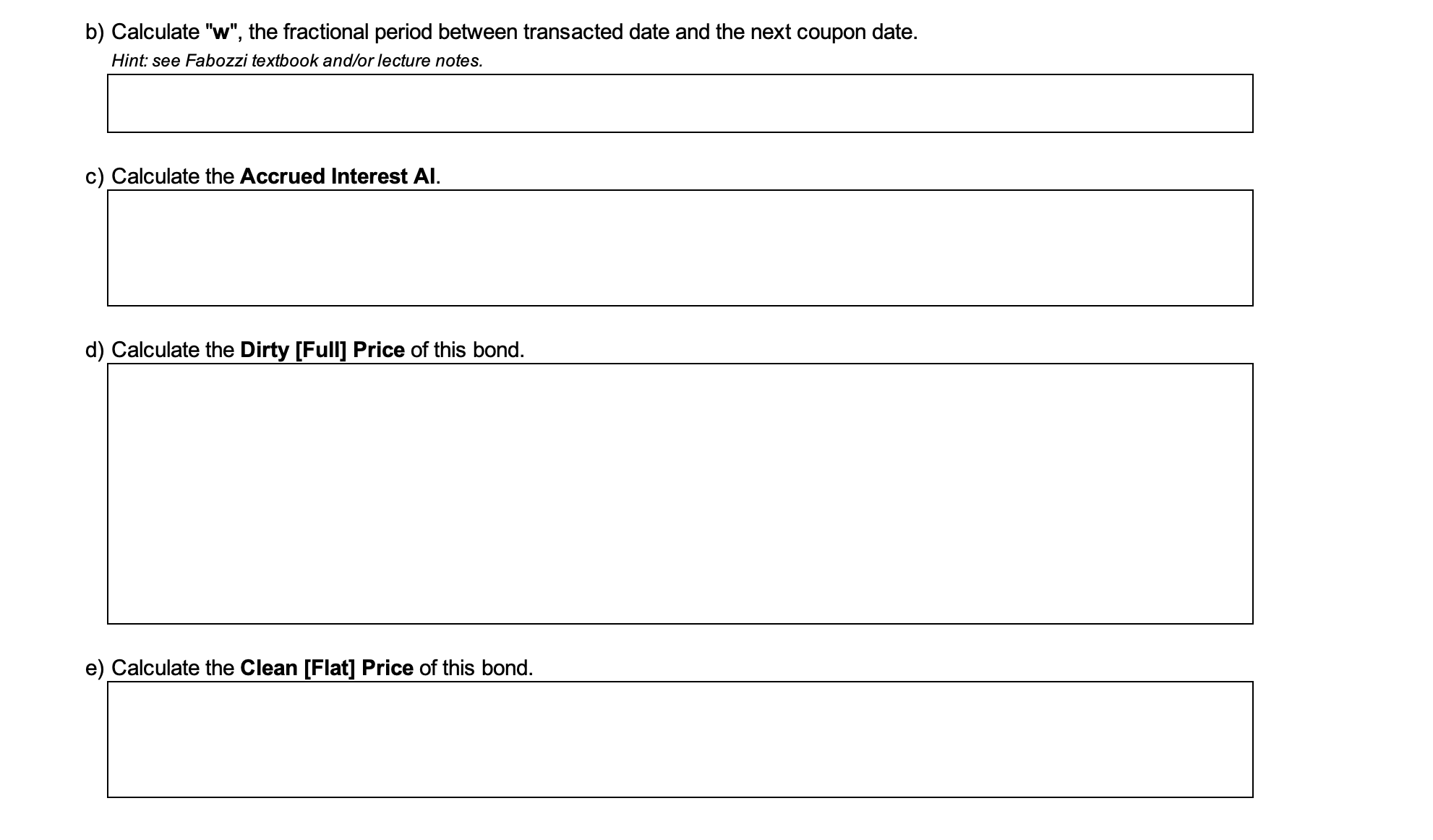

Question: m Up to this point this point. we have learned how to calculate bond prices occuring on coupon dates: we can conveniently input integral number

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts