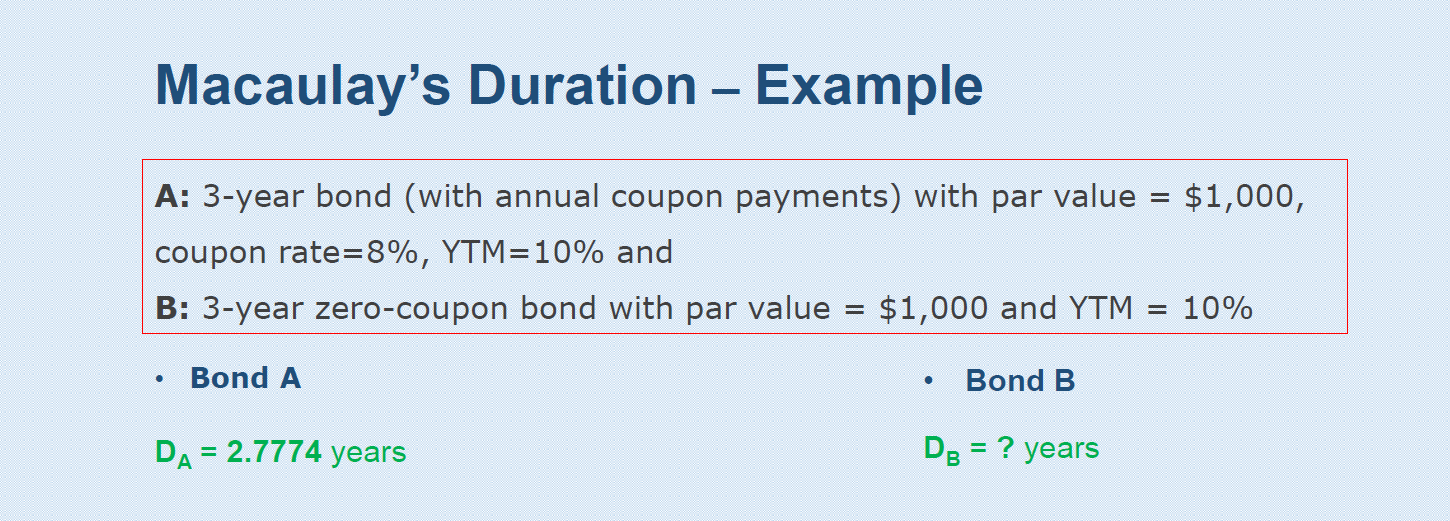

Question: Macaulay's Duration - Example A: 3-year bond (with annual coupon payments) with par value = $1,000, coupon rate=8%, YTM=10% and B: 3-year zero-coupon bond with

Macaulay's Duration - Example A: 3-year bond (with annual coupon payments) with par value = $1,000, coupon rate=8%, YTM=10% and B: 3-year zero-coupon bond with par value = $1,000 and YTM 10% . Bond A . Bond B DA = 2.7774 years De = ? years

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock