Manufacturing and selling recreational cannabis products are still illegal according to the federal government. A neighborhood cannabis

Question:

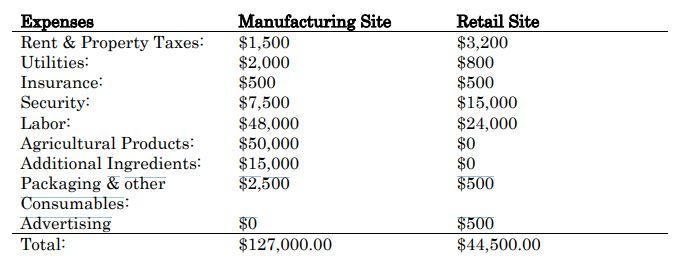

Manufacturing and selling recreational cannabis products are still illegal according to the federal government. A neighborhood cannabis company is our customer, CC. CC is legitimately in business. Cannabis is not grown by CC. However, it does refine the unprocessed agricultural product into sweets like chocolate and other recreational marijuana products. Customers may purchase the cannabis chocolates that CC makes at its store in Indica City. Since CC runs both locations under the same roof, the retail location does not pay the production location to produce the items. This enables CC to control expenses and compete favorably with other, comparable companies. Celia would appreciate our opinion on whether or not certain things are income and whether certain items are deductible. For now, ignore the state tax law consequences. Using the memorandum template and only referring to the attached materials, please advise Celia on the inclusion or deductibility of the following: • CC earns $250,000 per month from its retail sales of cannabis products • CC has the following expenses each month:

• Because CC is owned and operated as a sole proprietorship all items of income and deduction appear on Form 1040, Schedule C. Tax due is paid on Celia's personal income tax return.

Explain what you believe Celia’s (and CC’s) options are with respect to these items, given the current state of the law. Advise our client on what is the best answer and why. The memorandum should be no longer than 8 pages long and use tax code laws.

Expert Answer:

MEMORANDUM To Celia From CPA Date Re Inclusion and Deductibility of Cannabis Products This memorandum provides an analysis of the inclusion or deductibility of the various items related to the recreat... View the full answer

Financial Management for Public Health and Not for Profit Organizations

ISBN: 978-0132805667

4th edition

Authors: Steven A. Finkler, Thad Calabrese